Delivering effective, efficient, and impartial home valuations across America

Empowering lenders to better serve their customers through a spectrum of options that foster a more efficient, understandable, and impartial valuation system, saving time and money in the origination process.

New! Click here to access the current property data collection: fulfillment providers list.

Value acceptance + property data has arrived

This new option reduces cycle times and may reduce borrower costs, promotes safety and soundness by obtaining a current observation of the subject property, and provides operational simplicity and certainty at time of loan application.

Fact Sheet Lender Checklist Service Provider Checklist

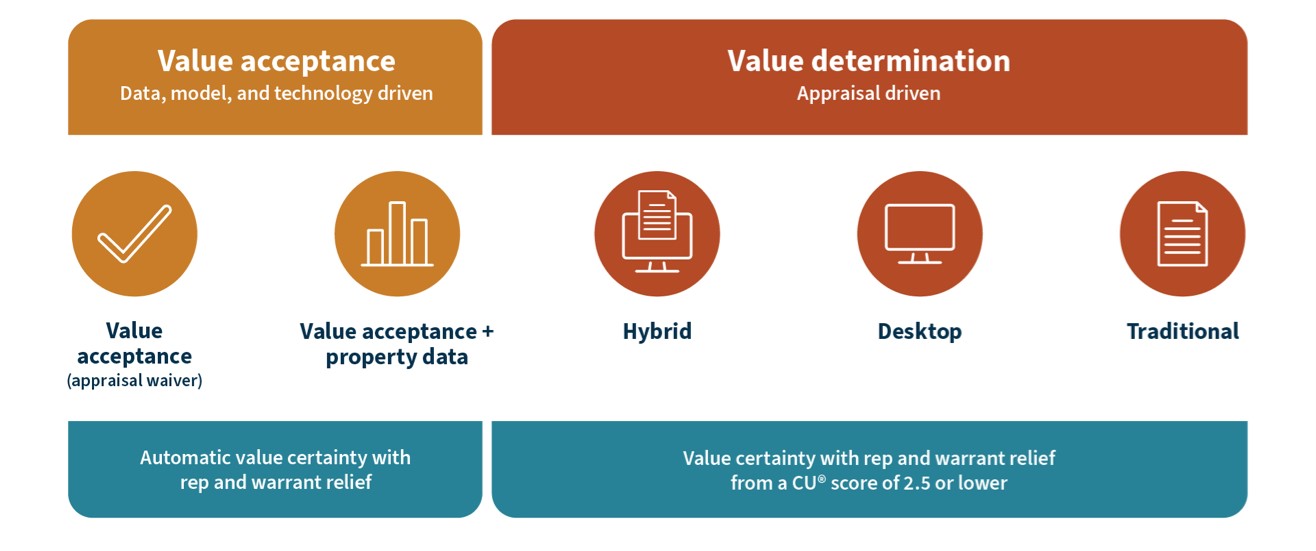

The modern valuation spectrum

Fannie Mae is on a journey of continuous improvement to make the home valuation process more efficient and accurate. We're transitioning to a spectrum of options to establish a property’s market value, with the option matching the risk of the collateral and the loan transaction. The spectrum balances traditional appraisals with appraisal alternatives.

Resources

Property Data Application Programming Interface (API)

Fannie Mae has established a property data standard and API to collect data and images consistently. The process encourages the use of emerging technologies to capture property information, imagery, and floor plans.

Lenders: Contact your Fannie Mae account team to request access.

Technology Service Providers (TSPs): In order to integrate with the Property Data API, complete the TSP Intake Form here.

Property Data API Review Tool (PDART)

Lenders, Mortgage Insurers (MI), and service providers may use our PDC web viewer known as Property Data API Review Tool (PDART) to aid with their required review process. Users can easily view the submitted property data, photos, and floor plan, as well as messages to help identify any potential PDC issues.

Lenders and MI companies: PDART is an available application in Technology Manager.

Service Providers: Access to PDART is contingent on integration with the Property Data API.

See the PDART Access Job Aid to learn more.