Utah Community Credit Union

With HomeReady, Utah Community Credit Union (UCCU) has been able to expand its business and serve its borrowers better.

The Situation

UCCU came from humble beginnings, it didn't have money for an office space, so it took its first deposits on a stair landing in a school building; it didn't have a vault, so it held its assets in a cast-iron tub. While the business has grown, that dedication to doing what it takes to better serve its customers remained.

So when Fannie Mae launched HomeReady®, a low down payment mortgage for low-income homebuyers in 2015, UCCU saw it as a natural fit. The credit union began to roll it out almost immediately after its release and it helped UCCU affordably expand homeownership to a larger population.

Right out of the gate, we thought HomeReady was a great product that aligned with our core values. We really strive to find products that will put our members in a better financial situation, so we were delighted to offer HomeReady based on our financial values and corporate mission statement.

help

The Result

UCCU trained its staff to use the resources available at HomeReady Mortgage and invited mortgage insurance (MI) companies to promote HomeReady’s benefits. The credit union also developed an affordable product matrix to help loan officers better understand the pros and cons of all of their affordable mortgage products.

"Before HomeReady was available we were using FHA and some other affordable products, but HomeReady has pretty much taken over most of that business," Short stated. "The benefits quickly made it clear to our staff and membership that HomeReady was a better product."

UCCU has found value in a number of HomeReady's flexibilities beyond the product's ability to offer down payments as low as three percent, such as its lower MI and flexibilities around the amount of income a borrower needs to qualify for HomeReady.

HomeReady can also be combined with a Community Seconds® product to assist borrowers with a down payment and/or closing costs, which has been a key to its success. UCCU's creative Community Second offering assists borrowers that meet income and credit score requirements who have not owned a home in at least three years.

HomeReady complements our assistance program, Short notes. By putting those two programs together, it allows us to offer a zero percent down financing option to borrowers that are earning less than 80 percent of the area median income.

Although HomeReady has helped UCCU drive volume and gain a competitive edge over other lenders in the area, the real value Short sees in HomeReady is the way it helps UCCU serve borrowers better.

"We have an obligation to help our community find the best product that's going to save them the most money," Short said. "The HomeReady product has more to offer than a standard conventional loan does."

HomeReady + Community Seconds = Affordable Homeownership

David,* a restaurant manager, was looking for a home for himself and his wife. He had a good credit score and minimal debt, but with an income of only $35,000 a year, he was having trouble saving for a down payment — even though he qualified for a mortgage loan.

Working with UCCU, David was able to qualify for the credit union's Community Seconds program, which was combined with a HomeReady loan. He was ultimately able to buy a home and he also saved on his monthly payments in interest and mortgage insurance.

* Borrower names have been changed to protect privacy.

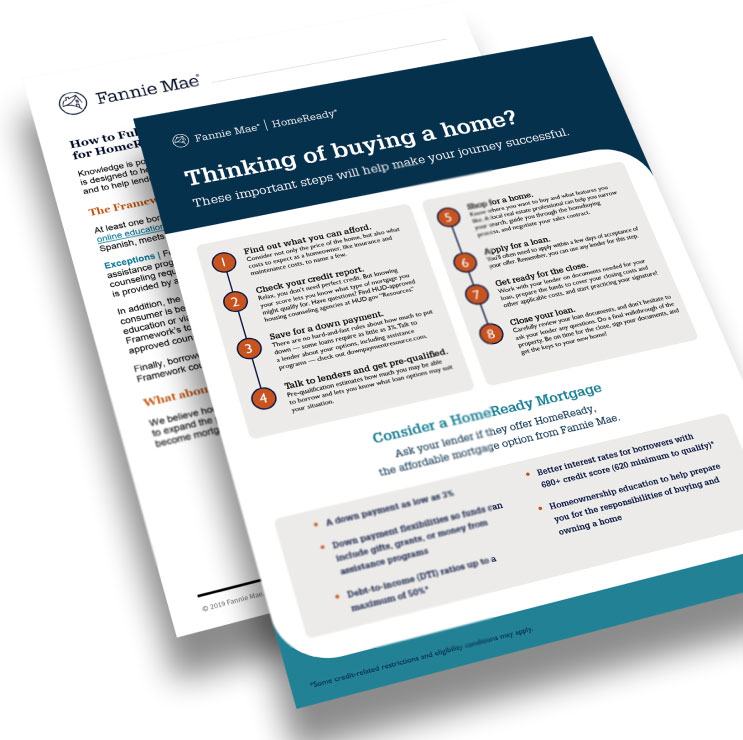

Quick Start Guide

To learn more about HomeReady, click below or talk to your account representative.

Learn more