My web

Navigating Loan Application Fields

![]()

This document explains where to locate certain loan application fields in the Desktop Underwriter® (DU®) user interface.

You may scroll through this document or click a link to be taken to the information for the specified field. If the field you are looking for isn't listed, you should be able to find it in the Uniform Residential Loan Application (URLA) Field Name Comparison spreadsheet, which compares the data fields of the current Uniform Residential Loan Application, Form 1003/Form 65 to the data fields in the redesigned Form 1003/Form 65.

Loan Type (Conventional, FHA, VA)

Property Types (Attached, Detached, Condominium, Cooperative, PUD)

Properties Excluded From the Multiple Financed Properties Policy

Derogatory Credit Policy Feature Codes

New Subordinate Financing Source

Condo Project Manager ID / Project Name

Income Calculator Reference Number

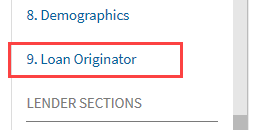

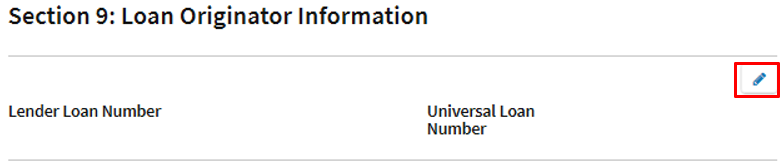

Lender Loan Number

Click 9. Loan Originator in the navigation bar.

Click the Edit icon to add or change the Lender Loan Number.

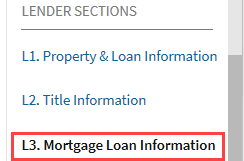

Loan Type

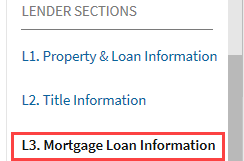

Click L3. Mortgage Loan Information in the navigation bar.

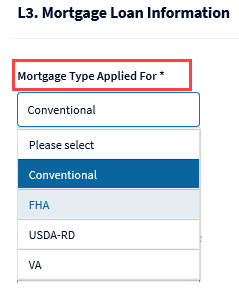

Click the Edit icon to specify the loan type.

The field is called Mortgage Type Applied For on this screen.

Note: Only the Conventional, FHA, and VA options will be underwritten through DU, which means DU will return an Out of Scope recommendation if USDA-RD is selected.

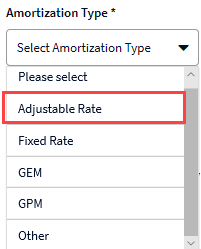

You can also specify if the interest rate is an adjustable rate on this screen by selecting Adjustable Rate in the Amortization Type field.

Note: Only the Fixed Rate and Adjustable Rate options will be underwritten through DU, which means DU will return an Out of Scope recommendation if any other option is selected.

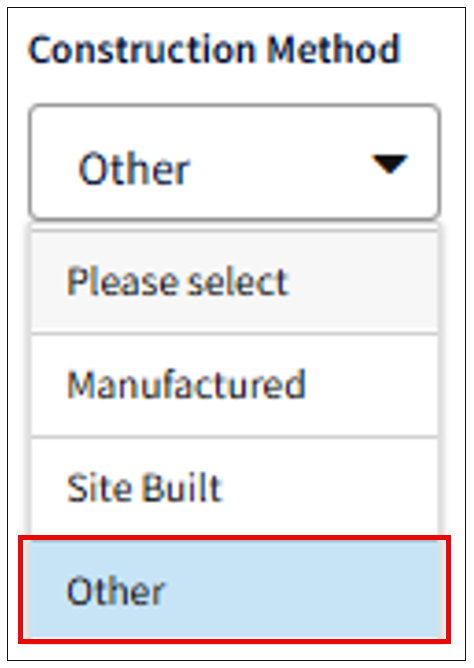

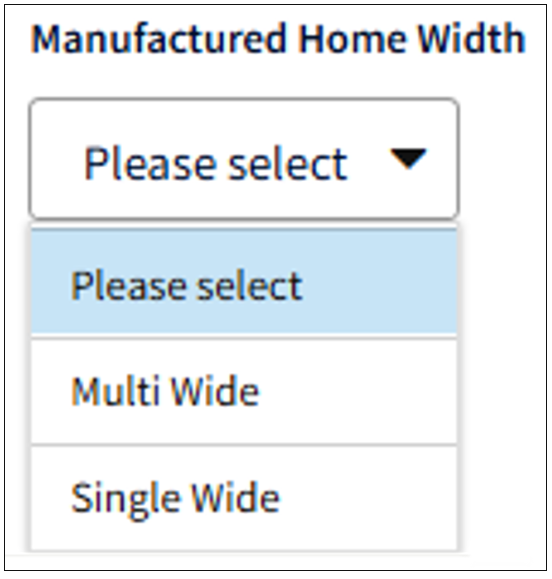

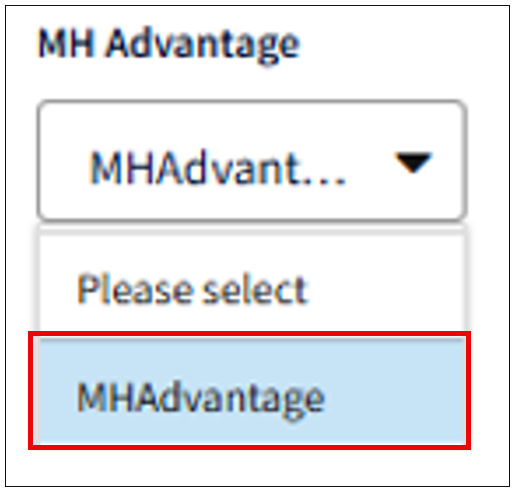

Manufactured Home

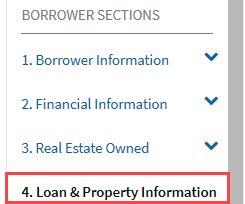

Click 4. Loan & Property Information in the navigation bar.

In the 4a. Loan and Property Information screen, click the Edit icon. In the Construction Method field, select Manufactured.

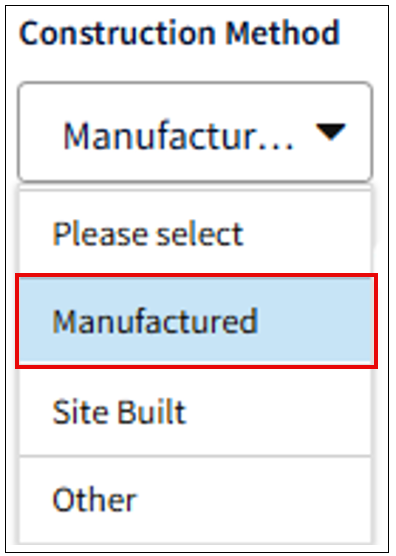

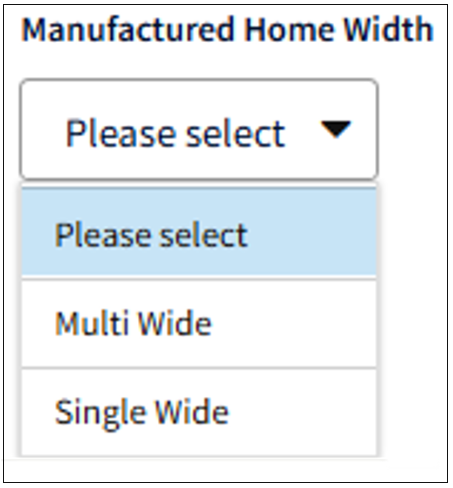

The Manufactured Home Width field will be displayed. Select the width of the manufactured home.

If it is MH Advantage, select Other in the Construction Method field. TheManufactured Home Width andMH Advantage fields will be displayed.

Select thewidth of the manufactured home in the Manufactured Home Width field.

SelectMH Advantage in theMH Advantage field.

Refer to the Valid Property Type Combinations resource for additional information on property types.

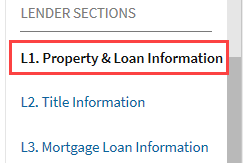

Property Types

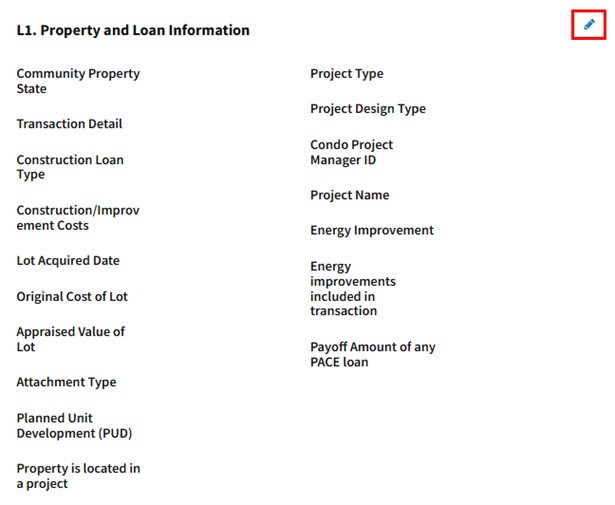

Click L1. Property & Loan Information in the navigation bar.

Click the Edit icon to specify the property type.

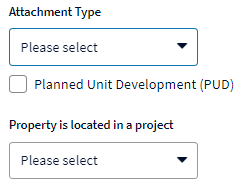

The Attachment Type field is where you select Attached or Detached. If the property is located in a planned unit development, click the Planned Unit Development (PUD) checkbox. If the property is located in a condominium or cooperative, select Yes in the Property is located in a project field.

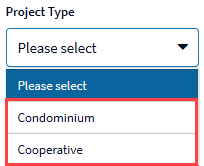

If the property is located in a condominium or cooperative, the Project Type field is where you select Condominium or Cooperative.

Refer to the Valid Property Type Combinations resource for additional information on property types.

Mortgage/HELOC Liabilities

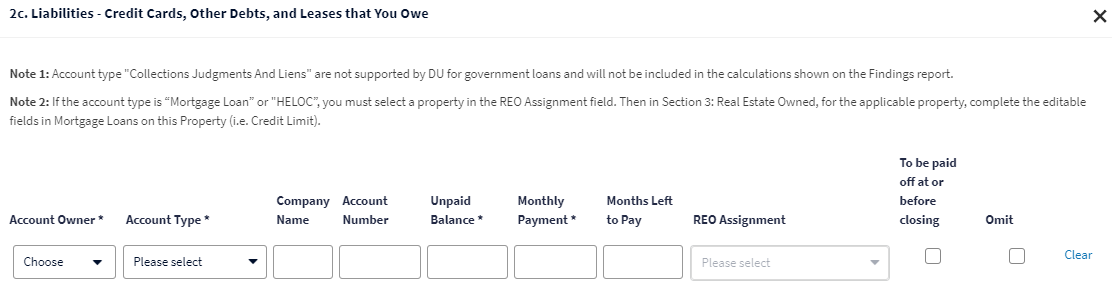

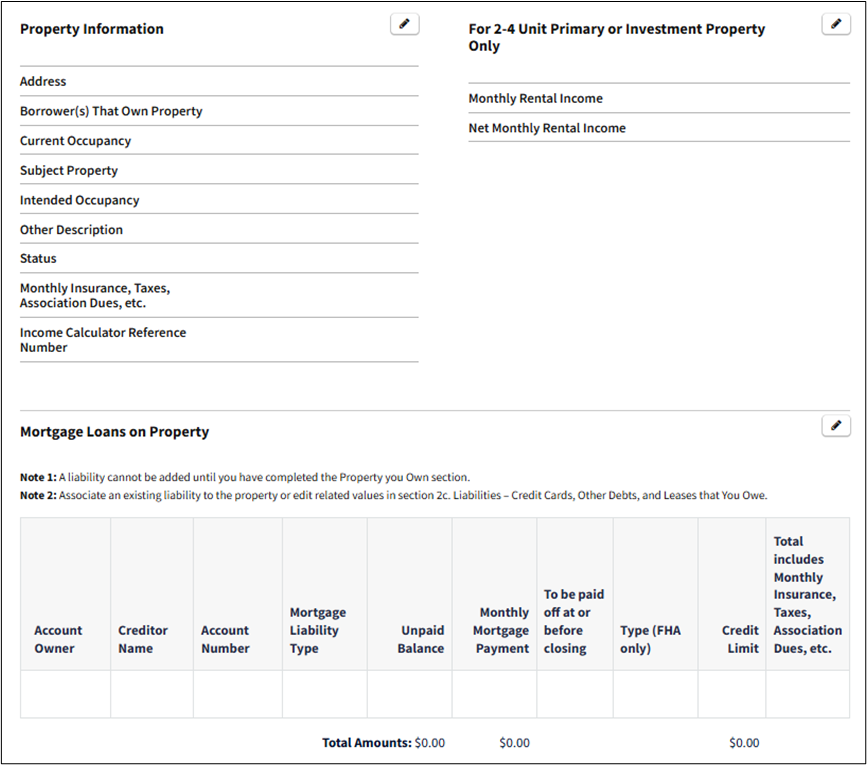

The mortgage and HELOC liabilities are displayed in the Real Estate Owned section, however most of the data associated to them can only be entered and/or edited on the2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe screen.

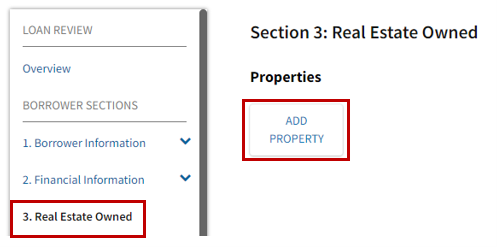

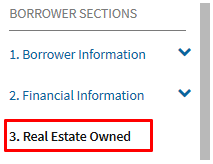

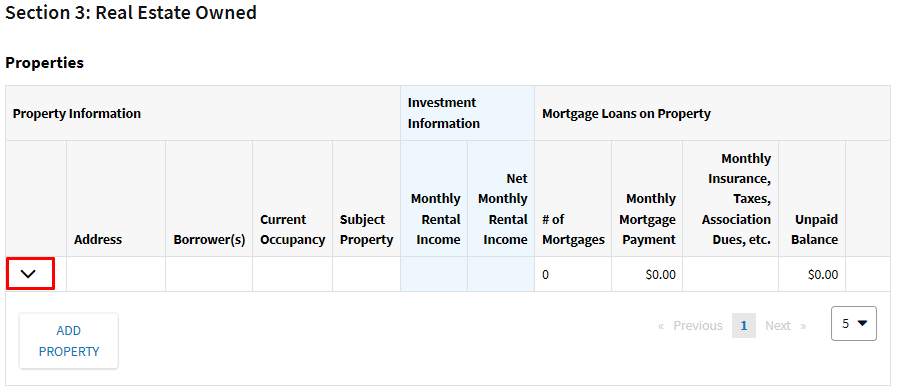

The REO Assignment field only applies to Mortgage Loan and HELOC liabilities, and the properties entered in the REO section will be included in the drop-down list. If no properties are listed in the drop-down list, click 3. Real Estate Owned in the navigation bar to add the property information.

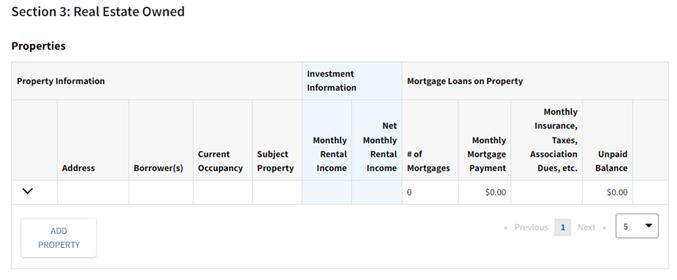

Click ADD PROPERTY.

Enter the property information for all properties. Enter the rental income information for a 2-4 unit primary residence and any investment properties. Enter the editable information for the mortgage(s) and/or HELOC(s).

Note: If the balance of a HELOC liability is being paid down or off, but remaining open, click the To be paid off at or before closing checkbox. Add another HELOC liability with the remaining balance (if paying down) or $0.00 (if paying off) and associate it to the REO record. Enter the credit limit in the Credit Limit field so DU can calculate the HCLTV.

Refer to the Debt-To-Income (DTI) Ratio Calculation Questions job aid for information about entering rental income and the payment for the monthly property insurance, taxes, etc.

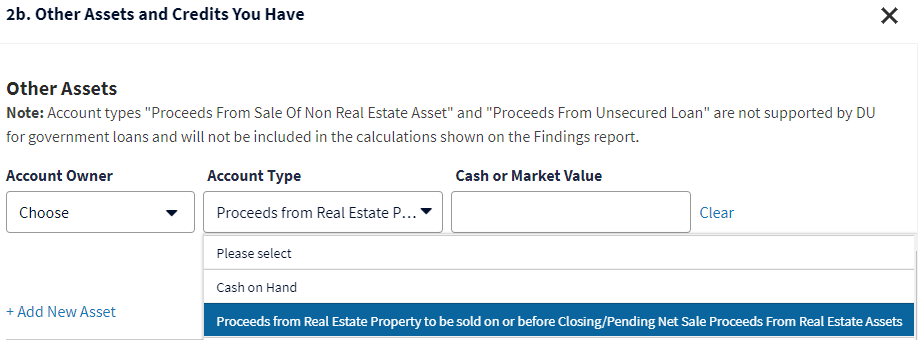

Pending Sale Proceeds

Expand 2. Financial Information in the navigation bar and click Other Assets.

Click the Edit icon for the 2b. Other Assets and Credits You Have screen.

In the Account Type field, select Proceeds from Real Estate Property to be sold on or before Closing/Pending Net Sale Proceeds From Real Estate Assets. Make sure to complete the other two fields.

Rental Income

For income associated to a property that is not the subject of the transaction.

Click 3.Real Estate Owned in the navigation bar.

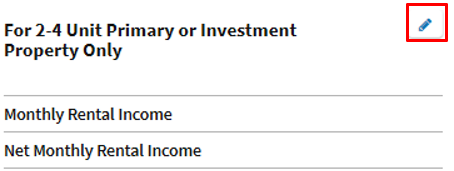

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the applicable property.

Click the Edit icon for the For 2-4 Unit Primary or Investment Property Only screen.

Refer to the Rental Income section in the Debt-To-Income (DTI) Ratio Calculation Questions job aid for information about rental income from a non-subject property.

Subject Property Income

For income associated to the subject property. The fields used will depend on the transaction type.

Subject Property Income for a Refinance Transaction

If it is a refinance transaction, click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the subject property.

Click the Edit icon for the For 2-4 Unit Primary or Investment Property Only screen.

Subject Property Income for a Purchase Transaction

If it is a purchase transaction, expand 4. Loan & Property Information in the navigation bar andclick Rental Income.

Click the Edit icon for the 4c. Rental Income on Property You Want to Purchase screen. Enter the income for the subject property in the Expected Net Monthly Rental Income field.

Refer to the Subject Property Income section in the Debt-To-Income (DTI) Ratio Calculation Questions job aid for information about rental income from a subject property.

Undrawn HELOC Amount

New HELOC

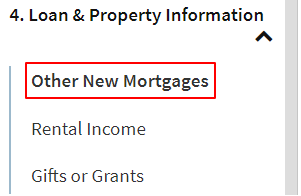

For a new HELOC, expand 4. Loan & Property Information in the navigation bar and click Other New Mortgages.

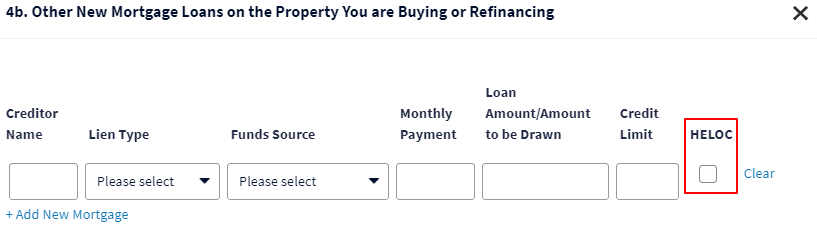

Click the Edit icon for the 4b. Other New Mortgage Loans on the Property You are Buying or Refinancing screen.

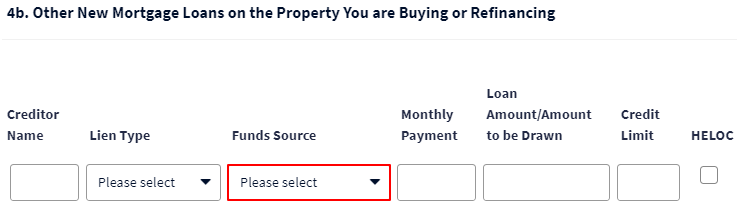

Enter the required data. Click the HELOC checkbox. DU calculates the undrawn HELOC amount by subtracting the amount you enter in the Loan Amount/Amount to be Drawn field from the amount you enter in the Credit Limit field. The result of the calculation is included in the HCLTV.

Refer to the note in the Mortgage Loan Details section of the Qualifying the Borrower job aid for important information about how a new HELOC should be reflected on line J. of the L4 Mortgage Loan Details section.

Existing HELOC

For an existing HELOC, click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the subject property.

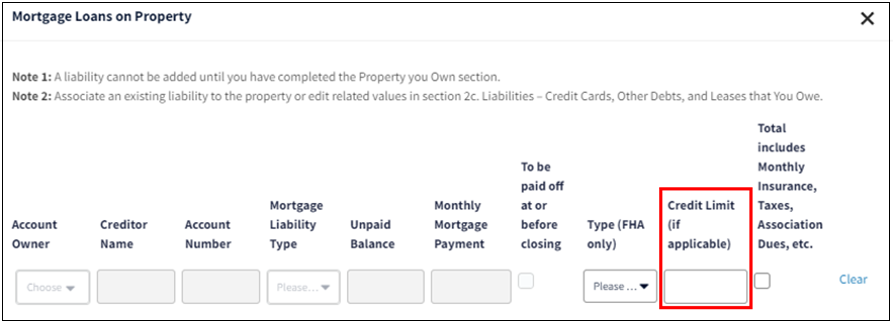

Click the Edit icon for the Mortgage Loans on Property screen and enter the total HELOC amount in the Credit Limit field.

DU calculates the undrawn HELOC amount by subtracting the amount in the Unpaid Balance field from the amount you enter in the Credit Limit field. The result of the calculation is included in the HCLTV.

Present Housing Expenses

As there is not a specific section to provide the borrower’s present housing expenses, DU uses information from other sections to determine those expenses. If the borrower rents, DU uses the rent payment on the 1a. Current Address screen. If the borrower owns, DU uses the mortgage payment on the 2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe screen and the taxes, insurance, etc. payment on the Property Information screen from the REO record indicated as the borrower’s Primary Residence.

Note: If there are two borrowers with a joint credit report, they will be on the same loan application and DU will only use the mortgage payment and taxes, insurance, etc. payment (if applicable) associated to the primary borrower. Therefore, there are two scenarios that would require individual credit reports for the two borrowers.

1. A primary residence transaction when one borrower is a non-occupant borrower.

2. A second home or investment transaction when the borrowers do not share a primary residence (have separate housing expenses).

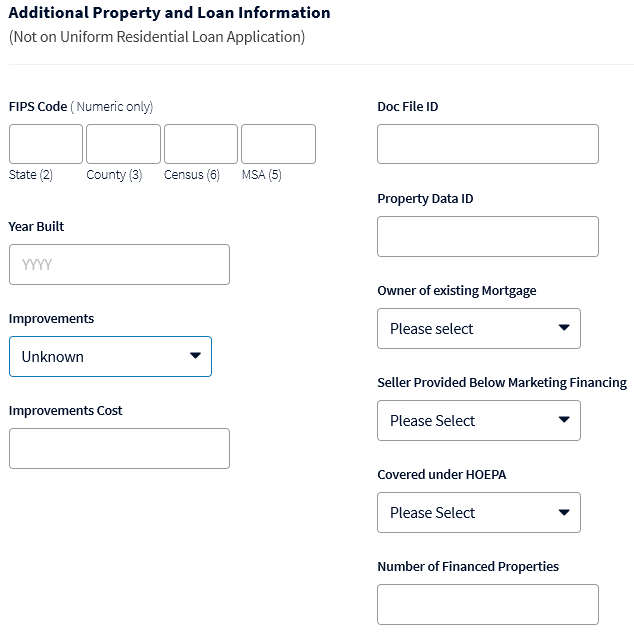

FIPS Code

Doc File ID

Owner of Existing Mortgage

Number of Financed Properties

Click Additional Property and Loan Information in the navigation bar.

Click the Edit icon to add or change the data.

Notes: If you select Yes in the Covered under HOEPA field, DU will return an Ineligible recommendation as loans covered by the Home Ownership and Equity Protection Act (HOEPA) are not eligible for delivery to Fannie Mae.

Only a valid Doc File ID should be entered in the Doc File ID field. Placeholder values (e.g., N/A, 0, Null, etc.) should not be entered in this field.

A zero is not a valid number to enter in the Number of Financed Properties field.

Properties Excluded from the Multiple Financed Properties Policy

DU applies the Multiple Financed Properties Policy guidelines specified in the Selling Guide to second home and investment property loan casefiles. As commercial real estate, multifamily properties, vacant lots, and farms are not included in the properties subject to the limitations in the policy, additional information in the REO record is needed to accurately apply the guidelines.

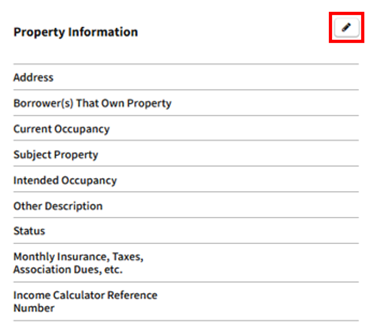

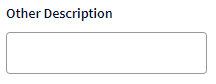

Click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the property.

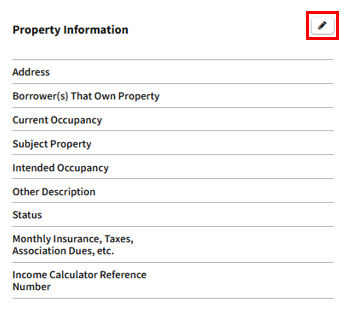

Click the Edit icon for the Property Information screen.

Scroll down to the Other Description field. Enter one of the following applicable descriptions: Commercial, Multifamily, Land, Farm, Chattel, or Timeshare. DU will use the information when applying the eligibility and reserve requirements associated to the multiple financed properties policy.

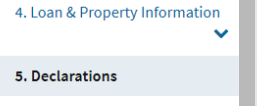

Derogatory Credit Policy Feature Codes

Click 5. Declarations in the navigation bar.

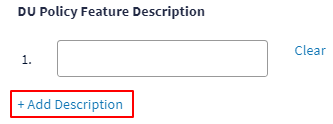

Scroll down and click the Edit icon for the 5b. About your Finances screen for the borrower and enter the applicable code in the DU Policy Feature Description field. If another code applies, click + Add Description and enter the code.

Note: The code tells DU to disregard the derogatory credit event from the DU eligibility assessment. Refer to the Selling Guide for more information about using the codes and the associated requirements.

RefiNow™ Opt Out Option

If a limited cash-out refinance loan casefile is underwritten as RefiNow, but you do not want it to be underwritten as RefiNow, you can instruct DU to underwrite the loan casefile as a standard limited cash-out refinance.

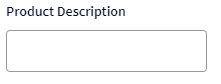

Click L3. Mortgage Loan Information in the navigation bar.

Click the Edit icon for the L3. Mortgage Loan Information screen. Enter Standard LCOR in the Product Description field.

First-time Homebuyer

There is not a field to specify to DU that a borrower is a first-time homebuyer. DU uses the following to determine whether there is a first-time homebuyer on the loan casefile:

1. The transaction is a purchase,

2. The occupancy is primary residence, and

3. Any borrower that is going to occupy the property has indicated “No” for the A.1 If Yes, have you had an ownership interest in another property in the last three years? declaration.

The logic is based on the definition of a first-time homebuyer in the Selling Guide.

Note: The Selling Guide also specifies that an individual who is a displaced homemaker or single parent will be considered a first-time homebuyer if they had no ownership interest in a principal residence other than a joint ownership interest with a spouse during the preceding three-year time period. When the borrower specifies that they have had an ownership interest in another property in the last three years for declaration A.1, but that borrower can be considered a first-time homebuyer using this exception, the lender can provide “FTHB Exception” in the DU Policy Feature Description field in section 5b. About Your Finances for that borrower, and DU will determine the borrower to be a first-time homebuyer.

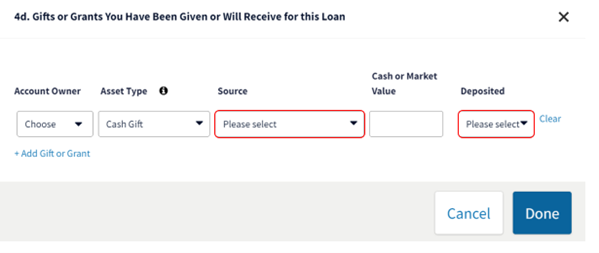

Gift/Grant Source

The source of a gift or grant can impact eligibility, so it must be completed.

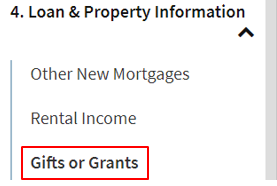

Expand 4. Loan & Property Information in the navigation bar and click Gifts or Grants.

Click the Edit icon for the 4d. Gifts or Grants You Have Been Given or Will Receive for this Loan screen. Select the provider of the gift or grant in the Source field. If the gift or grant has been deposited in an asset account (i.e. savings account), select Yes in the Deposited field. If the gift or grant has not been deposited in an asset account, select No in the Deposited field.

Note: If Yes is selected in the Deposited field, DU will not include the amount entered in the Cash or Market Value field in the total available assets. If No is selected in the Deposited field, DU will include the amount entered in the Cash or Market Value field in the total available assets.

New Subordinate Financing Source

The source of new subordinate financing must be completed.

Expand 4. Loan & Property Information in the navigation bar and click Other New Mortgages.

Click the Edit icon for the 4b. Other New Mortgage Loans on the Property You are Buying or Refinancing screen. Select the source of the new subordinate financing in the Funds Source field.

Earnest Money

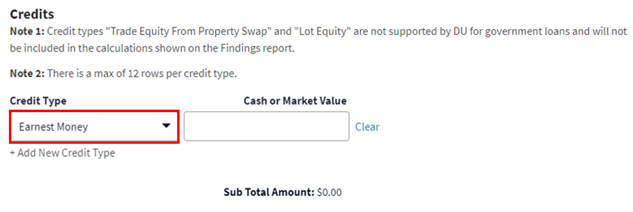

Expand 2. Financial Information in the navigation bar and click Other Assets.

Click the Edit icon for the 2b. Other Assets and Credits You Have screen and scroll down to the Credits section. Select Earnest Money in the Credit Type field. Enter the earnest money amount in the Cash or Market Value field.

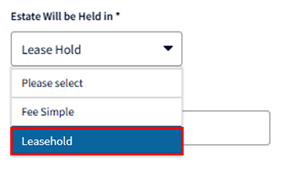

Leasehold Estates

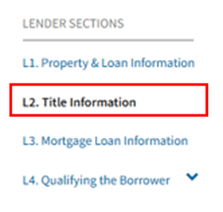

Click L2. Title Information in the navigation bar.

In the L2. Title Information screen, click the Edit icon. In the Estate Will be Held in* field, select Leasehold.

When Leasehold is selected for Estate Will be Held in* field, an Expiration Date field appears. Enter the Expiration Date.

Notes: The Estate Will be Held in* field should be left blank for leasehold estates granted by community land trusts.

Refer to Selling Guide section B2-3-03, Special Property Eligibility and Underwriting Considerations: Leasehold Estates for information about leasehold estates.

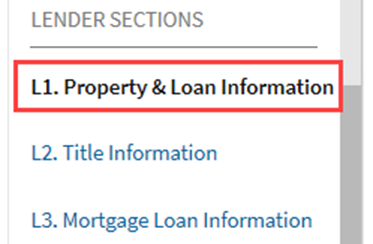

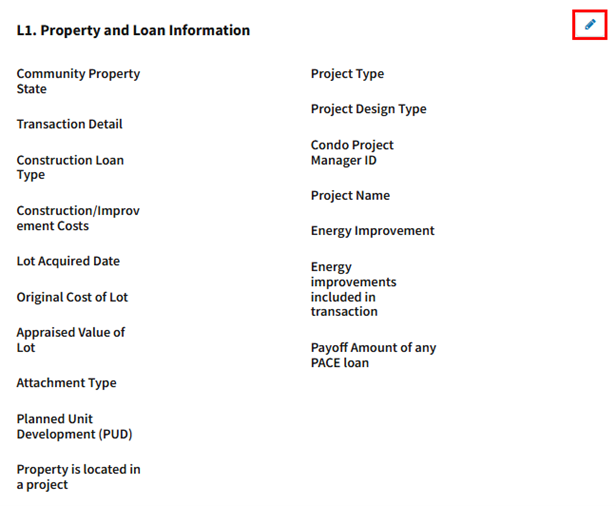

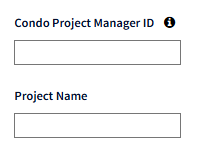

Condo Project Manager ID / Project Name

Click L1. Property & Loan Information in the navigation bar.

Click the Edit icon for the L1. Property and Loan Information screen.

The project name and/or Condo Project Manager ID can be entered in the following fields:

Note: In order for DU to contact Fannie Mae’s Condo Project Manager (CPM™), either a CPM ID or a complete property address along with the Project Name must be provided.

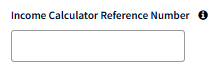

Income Calculator Reference Number

The field used to enter the Income Calculator Reference Number in DU will depend on the type of income that was calculated using Fannie Mae’s Income Calculator.

Entering the Income Calculator Reference Number for Rental Property Income

Click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the applicable property.

Click the Edit icon for the Property Information screen.

Enter the Income Calculator Reference Number.

Entering the Income Calculator Reference Number for Self-Employment / Business Ownership Income

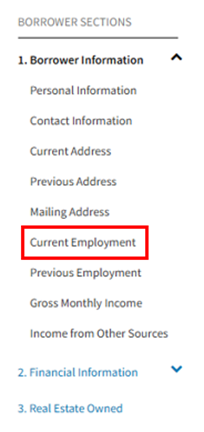

Expand 1. Borrower Information in the navigation bar and click Current Employment.

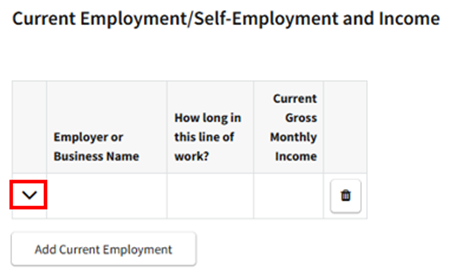

The Current Employment/Self-Employment screen will be displayed. Click the down arrow next to the applicable employment record.

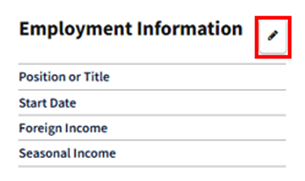

Click the Edit icon for the Employment Information screen.

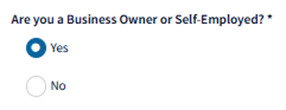

When the user selects Yes for the question Are you a Business Owner or Self-Employed? *, the Income Calculator Reference Number field will be displayed.

Enter the Income Calculator Reference Number.

Additional information about Fannie Mae’s Income Calculator can be found on the Income Calculator page.