My web

Debt-To-Income (DTI) Ratio Calculation Questions

![]()

This document provides data entry guidance to ensure DU includes all applicable debts and income in the Debt-to-Income (DTI) Ratio shown on the Desktop Underwriter® (DU®) Underwriting Findings report.

You may scroll through this document, or click a link to be taken to the information for the specified topic:

Second Home & Investment Property Transactions

Primary Residence Transaction With Non-Occupant Borrower

Primary Residence Purchase With Pending Sale

Calculation Explanations & Examples

Note: Click here to view How to Calculate DTI Ratio in the Loan Delivery Job Aids.

Liabilities

Verify the liabilities are correct. Expand2.Financial Information in the navigation bar and click Liabilities.

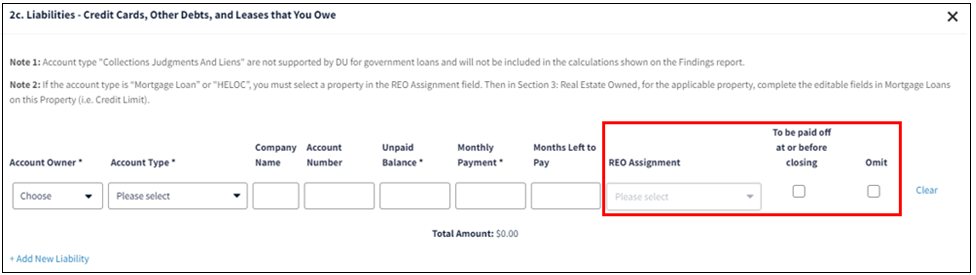

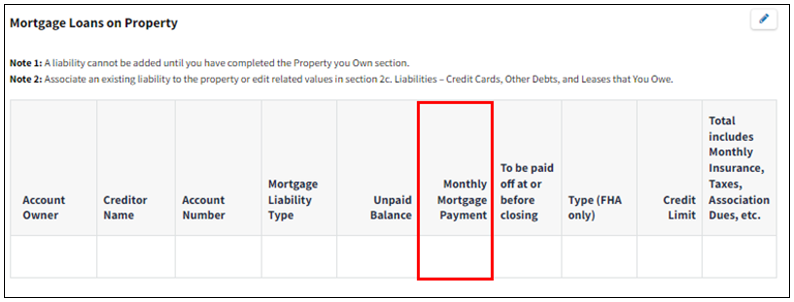

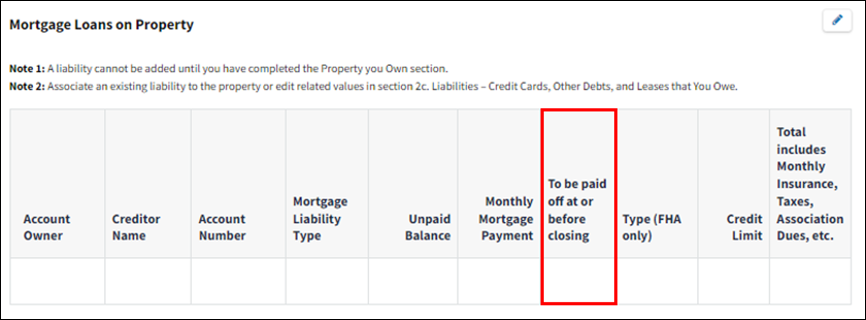

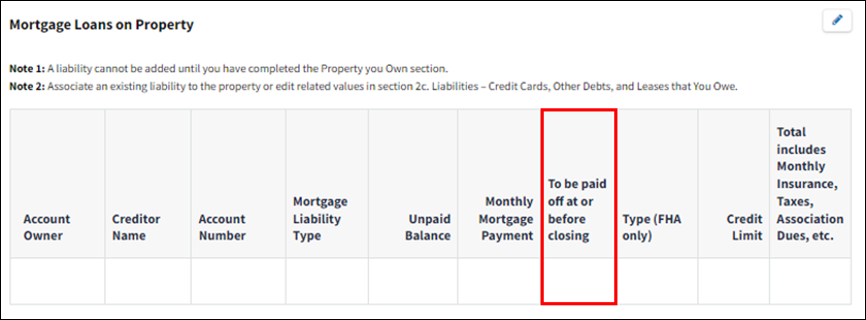

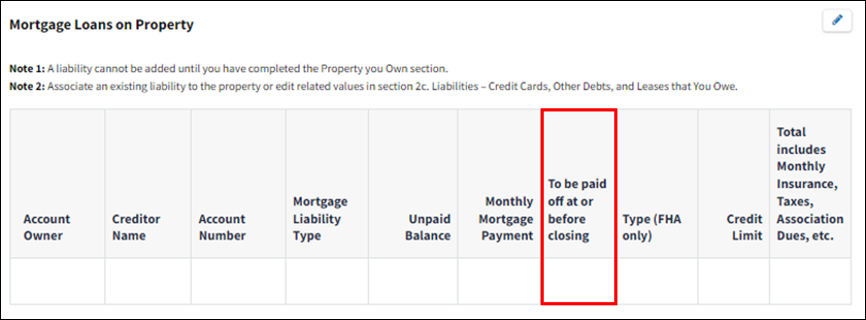

Click the Edit icon on the 2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe screen. Check the REO Assignment field for each mortgage and HELOC liability to make sure it is associated to the correct property in the Real Estate Owned section. Click Omit for a duplicate debt or a debt the borrower is not responsible for. In addition, ensure all liabilities paid by or before closing have a check in the To be paid off at or before closing checkbox.

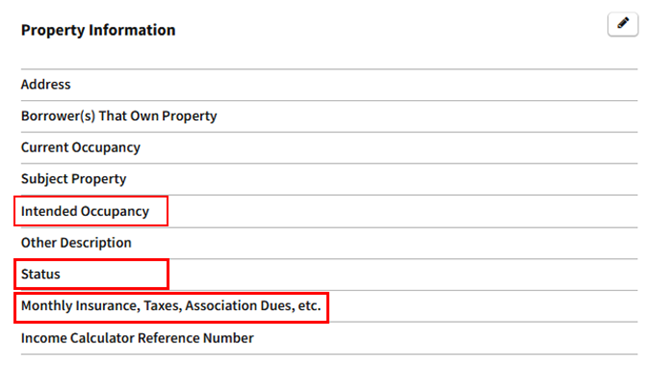

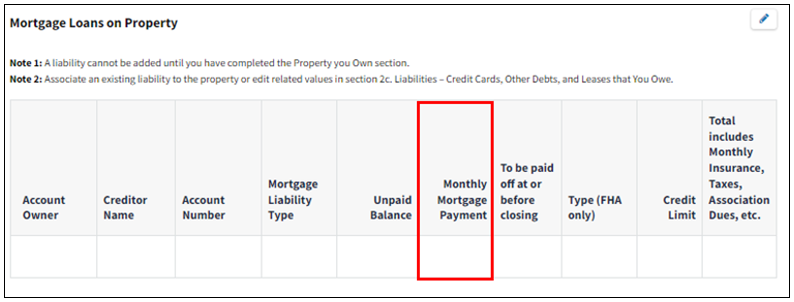

Note: If a mortgage payment includes the monthly insurance, taxes, association dues, etc., verify the Total includes Monthly Insurance, Taxes, Association Dues, etc. checkbox is checked in the applicable REO record on the Mortgage Loans on Property screen.

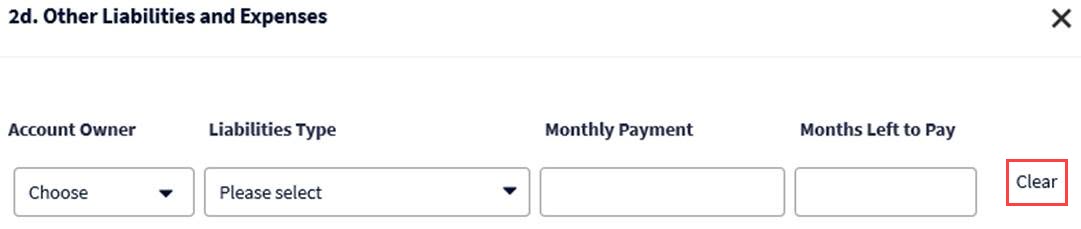

Click the Edit icon on the 2d. Other Liabilities and Expenses screen. Click Clear for a duplicate debt or a debt the borrower is not responsible for.

Rental Income

Verify rental income not associated with the subject property.

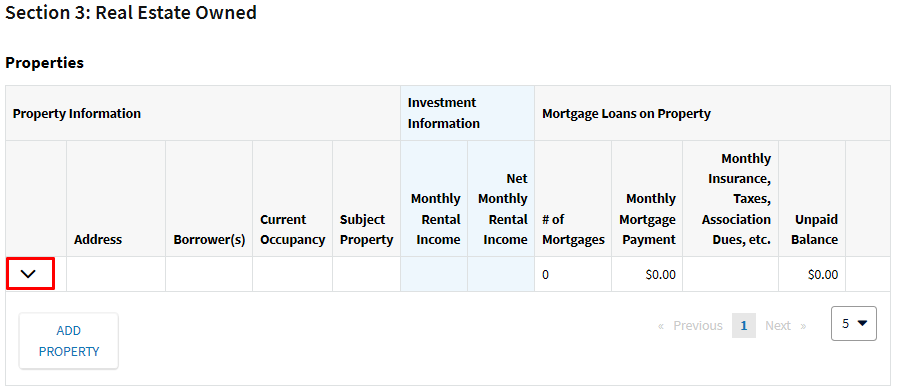

Click3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to each investment property to review the detailed real estate owned information.

Notes: Net rental income from a second home cannot be used when qualifying the borrower, and therefore, should not be entered on the loan application.

As a reminder, DU includes the mortgage payment and the taxes, insurance, association dues, etc. associated to a retained second home that is not the subject of the transaction in the total expenses.

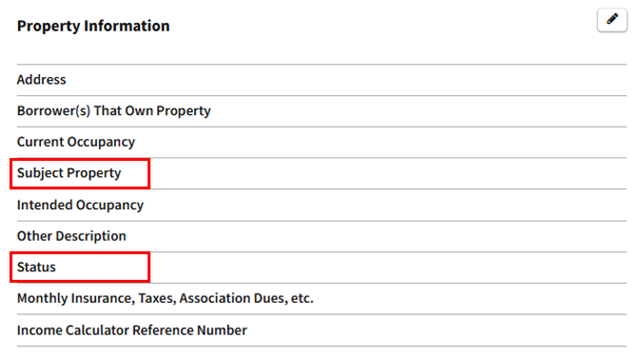

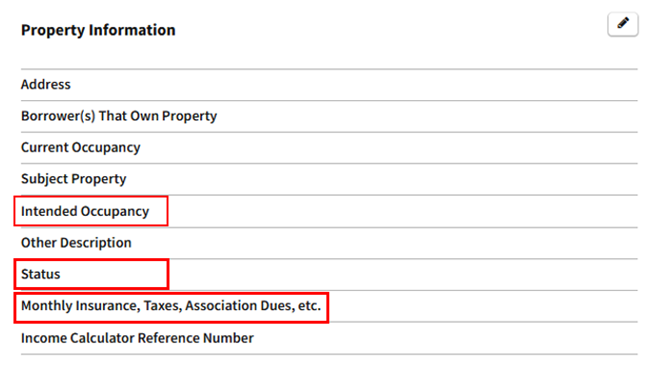

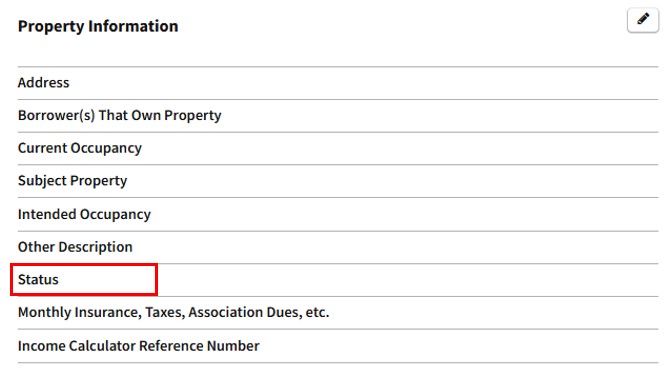

- For each investment property that is not the subject of the transaction, verify the Intended Occupancy is Investment and the status is Retained.

- For a 2-4 unit primary residence that is not the subject of the transaction, verify the Intended Occupancy is Primary Residence and the status is Retained.

- The data entry for the Monthly Insurance, Taxes, Association Dues, etc. field differs depending on whether or not the mortgage payment includes the monthly insurance, taxes, association dues, etc.:

- If the mortgage payment includes the monthly insurance, taxes, association dues, etc., verify the Total includes Monthly Insurance, Taxes, Association Dues, etc. checkbox is checked on the Mortgage Loans on Property screen, and verify the correct amount is entered for the taxes, insurance, etc. payments.

- If the mortgage payment does not include the monthly insurance, taxes, association dues, etc., verify the Total includes Monthly Insurance, Taxes, Association Dues, etc. checkbox is not checked on the Mortgage Loans on Property screen, and verify that any amounts not included in the mortgage payment are correctly entered in the Monthly Insurance, Taxes, Association Dues, etc. field.

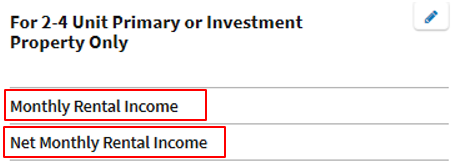

For each investment property that is not the subject of the transaction, verify the rental income information is correct. If there is a 2-4 unit primary residence that is not the subject of the transaction, verify the rental income information.

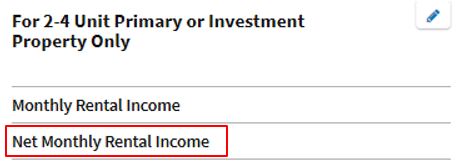

- If there is only an amount in the Monthly Rental Income field, DU will calculate the net monthly rental income using the following formulas:

Investment property: (monthly gross rental income x 75%) – (mortgage payments + monthly insurance, taxes, association dues, etc. if not already included in the mortgage payment) = monthly net rental income or loss,

2-4 unit primary residence: (monthly gross rental income x 75%) = monthly net rental income or loss

- If there is an amount in the Net Monthly Rental Income field, DU will use that amount instead of the amount entered in the Monthly Rental Income field.

If you have questions about how the net rental income should be manually calculated refer to the Selling Guide.

Note: DU will ignore a zero value in the Net Monthly Rental Income field. Therefore, in order for DU to use the net monthly rental income you provide (instead of calculating the amount using the monthly gross rental income) you must enter either a positive or negative amount. In other words, if the net rental income is a "breakeven" amount, you must enter either $0.01 or $-0.01.

For each investment property that is not the subject of the transaction, verify the mortgage payment(s).

- If the amount in the Monthly Mortgage Payment field includes the monthly insurance, taxes, association dues, etc. verify the Total includes Monthly Insurance, Taxes, Association Dues, etc. checkbox is checked.

- If any portion of the monthly insurance, taxes, association dues, etc. is not included in the monthly mortgage payment, then the Total includes Monthly Insurance, Taxes, Association Dues, etc. should not be checked. That portion of the monthly insurance, taxes, association dues, etc. not included in the mortgage payment should then be entered in the Monthly Insurance, Taxes, Association Dues, etc. field on the associated Property Information screen.

Note: DU does not include the mortgage payment and taxes, insurance, association dues, etc. associated to a non-subject investment property in the DTI because they should be factored into the net rental income calculation. If the net rental income is a "breakeven" amount, then see the above note regarding "breakeven" net rental income.

Note: If the combined total net rental income for all borrowers is positive, DU adds the net rental income to the qualifying income and includes it in the debt-to-income ratio. If the total is negative, DU treats the loss as a liability and includes it in the debt-to-income ratio.

Refer to the Entering Income from Rental Property job aid for additional information about entering rental income in DU.

Subject Property Income

Verify rental income associated with the subject property, which would apply to either a 2-4 unit primary residence or an investment property. The fields to verify will depend on the transaction type.

Subject Property Income for a Refinance Transaction

If it is a refinance transaction, click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the subject property to review the detailed real estate owned information.

Verify the amount entered in the Net Monthly Rental Income field is correct.

Notes: DU does not calculate the net rental income from the subject property based on the gross monthly income entered in the Monthly Rental Income field. The net rental income from the subject property should be manually calculated in accordance with the Selling Guide and entered in the Net Monthly Rental Income field, unless the subject property is a second home. Net rental income from a second home cannot be used when qualifying the borrower, and therefore, should not be entered on the loan application. See the Selling Guide for additional information.

On an investment transaction, DU does not include the proposed monthly payment for the subject property in the total expenses because it should be factored into the net rental income calculation for the subject property. On a 2-4 unit primary residence transaction, DU includes the proposed monthly payment for the subject property in the total expenses. See the Selling Guide for additional information.

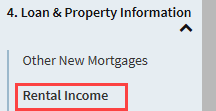

Subject Property Income for a Purchase Transaction

If it is a purchase transaction, expand 4. Loan and Property Information in the navigation bar and click Rental Income.

Verify the amount entered in the Expected Net Monthly Rental Income field is correct.

Notes: DU does not calculate the expected net monthly rental income from the subject property based on the gross monthly income entered in the Expected Monthly Rental Income field. The expected net monthly rental income from the subject property should be manually calculated in accordance with the Selling Guide and entered in the Expected Net Monthly Rental Income field. Expected net rental income from a second home cannot be used when qualifying the borrower, and therefore, should not be entered on the loan application. See the Selling Guide for additional information.

On an investment transaction, DU does not include the proposed monthly payment for the subject property in the total expenses because it should be factored into the expected net rental income calculation for the subject property. On a 2-4 unit primary residence transaction, DU includes the proposed monthly payment for the subject property in the total expenses. See the Selling Guide for additional information.

Refinance Transactions

Verify the property status and loan information. Click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the subject property to review the detailed real estate owned information.

Verify Subject Property is Yes and the Status is Retained.

Verify To be paid off at or before closing is Yes for any mortgage or HELOC being paid off.

Refer to the Entering Income from Rental Property job aid for additional information about entering rental income in DU.

Second Home & Investment Property Transactions

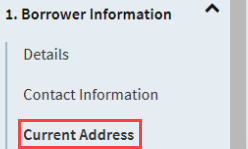

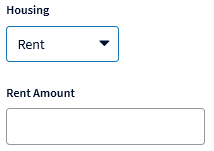

Verify the current housing expenses for each borrower are being accounted for correctly. If the borrower rents, expand 1. Borrower Information in the navigation bar and click Current Address.

Click the Edit icon on the 1a. Current Address screen associated to the borrower to verify the rent payment.

Note: If borrowers are renting together, the rent payment should either be only entered for one of the borrowers or split between them. If the entire rent payment is entered for both borrowers it will be double counted.

Refer to the note in the Present Housing Expenses section the Navigating Loan Application Fields job aid for important information about the present housing expenses.

If the borrower owns a primary residence, click 3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the primary residence to review the detailed real estate owned information.

Verify theIntendedOccupancy is Primary Residence, theStatus is Retained, and the Monthly Insurance, Taxes, Association Dues, etc. amount is correct.

Note: If a mortgage payment includes the monthly insurance, taxes, association dues, etc., verify the Total includes Monthly Insurance, Taxes, Association Dues, etc. checkbox is checked in the applicable REO record on the Mortgage Loans on Property screen.

Note: If there is more than one borrower, verify the current housing expenses for each borrower.

Refer to the note in the Present Housing Expenses section in the Navigating Loan Application Fields job aid for important information about housing expenses.

If the transaction is a cash out refinance of a second home or investment property and a primary residence mortgage and/or HELOC is being paid off with the transaction, verifyTo be paid off at or before closing isYes for the mortgage and/or HELOC associated to the primary residence.

Primary Residence Transaction With Non-Occupant Borrower

Verify the current housing expenses for each non-occupant borrower. See the applicable Second Home & Investment Property Transactions section above.

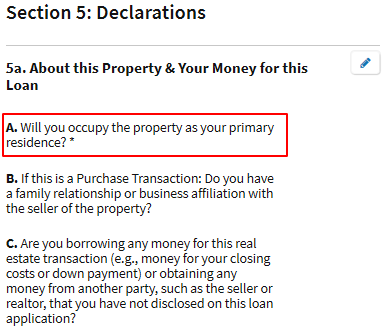

In addition, click 5. Declarations.

On the 5a. About this Property & Your Money for this Loan screen associated to each non-occupant borrower, verify A. Will you occupy the property as your primary residence? is No.

Also verify A. Will you occupy the property as your primary residence? isYes for the occupant borrower(s).

Primary Residence Transaction With Pending Sale

Click3. Real Estate Owned in the navigation bar.

The Properties screen, which contains a summary of the real estate owned information, will be displayed. Click the down arrow next to the pending sale property to review the detailed real estate owned information.

Verify the status isPendingSale.

VerifyTo be paid off at or before closing isYes for the associated mortgage and/or HELOC.

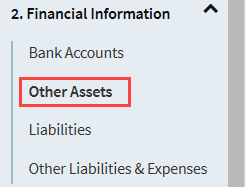

Expand 2. Financial Information in the navigation bar and click Other Assets.

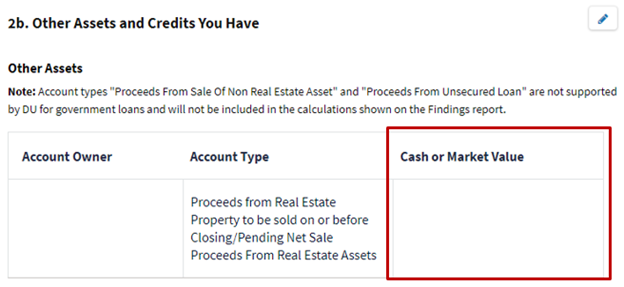

On the 2b. Other Assets and Credits You Have screen, verify the Cash or Market Value entered for the Proceeds from Real Estate Property to be sold on or before Closing/Pending Net Sale Proceeds From Real Estate Assets is correct.

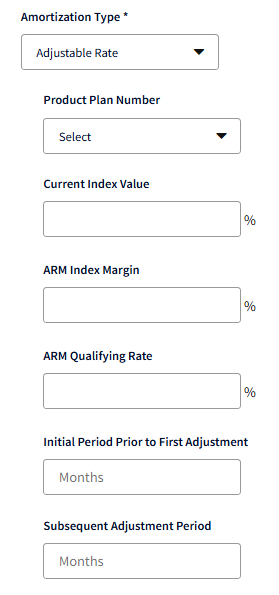

Adjustable Rate Transactions

On an Adjustable Rate Mortgage (ARM) transaction, the principal and interest payment DU calculates is based on the ARM qualifying rate. The ARM qualifying rate rules can be found in the Selling Guide and the DU Qualifying Interest Rate for Proposed Monthly Housing Expense document.

Verify the ARM information.

Click L3. Mortgage Loan Information.

On the L3. Mortgage Loan Information screen, verify the ARM index and margin are correct.

Note: DU will use a rate entered in the ARM Qualifying Rate field when the ARM plan selected in the Product Plan Number field isLender ARM Plan. If you send an ARM plan that DU does not recognize, it will be considered a "Lender ARM plan".

Calculation Explanations & Examples

Housing Expense Ratio

On a primary residence transaction, the housing expense ratio is calculated by adding the proposed monthly payments, which will include the principal, interest, real estate taxes, insurance (PITI) and can also include mortgage insurance, homeowner’s association (HOA) dues and miscellaneous fees (PITIA), together and dividing that by the total income. On a conventional loan, if there is a non-occupant borrower, DU will also include their housing expenses in the housing expense ratio.

Note: Refer to the note in the Present Housing Expenses section in the Navigating Loan Application Fields job aid for important information about the present housing expenses.

Example (note: all amounts are monthly):

Subject property PITIA $1,000

Total Income $5,500

Calculation: $1,000 (PITIA) divided by $5,500 (total income) multiplied by 100 equals 18.18%.

On a second home or investment property transaction, the housing expense ratio is the borrower(s’) primary residence PITIA, instead of the subject property proposed monthly PITIA, divided by the total income. See the Selling Guide section B3-6-03: Monthly Housing Expense.

Example (note: all amounts are monthly):

Primary residence PITIA $1,700

Total Income $8,000

Calculation: $1,700 (PITIA) divided by $8,000 (total income) multiplied by 100 equals 21.25%.

Debt-To-Income Ratio

Total monthly obligation includes all monthly debts per the Selling Guide Section B3-6-02: Debt to Income Ratios. Debts include, but are not limited to, mortgage payments, car payments, credit card payments, child support payments, alimony, negative net rental income, personal loan payments, etc.

Note: Positive net rental income will be added to the total monthly income. Negative net rental income will be added to the total monthly expenses.

Example (note: all amounts are monthly):

Car Payment $485

Student Loan $125

Personal Loan $225

Credit Cards $285

Housing payment $1,281

Total Expenses $2,401

Total Income $8,912

Calculation: $2,401 (total expenses) divided by $8,912 (total income) multiplied by 100 equals 26.94%.