My web

Delivering Income & Expense

![]()

How to Deliver the Monthly Income (Loan Level)

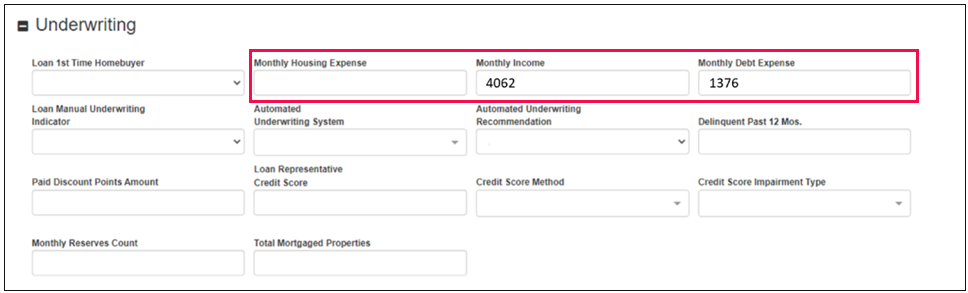

Monthly Income (Sort ID 291) is to be delivered with the combined qualifying gross monthly income of all borrowers. This is the denominator of the loan's Debt-to-Income Ratio. This field is located in the Underwriting section of the Loan Detail screen in Loan Delivery.

NOTE: Income must be reported to Fannie Mae for all high LTV refinance loans at the time of loan delivery, even for those transactions where there is no maximum DTI ratio. For high LTV refinance loans with payment changes less than or equal to 20%, the lender must report the stated income on the loan application (if any). If the borrower does not state any income and the lender uses the verification of reserves option as the income source, the lender must deliver the equivalent of the new monthly payment (PITIA) as the “Monthly Income” data element (Sort ID 291).

The max length for the Monthly Income field is 6 digits. For any values over 6 digits provide 999,999.

How to Deliver the Qualifying Income (Borrower Level)

Qualifying Income (Sort ID 573) is to be delivered with each individual borrower/co-borrower’s qualifying gross monthly income. This field is located in the Borrower/Co-Borrower section of the Loan Detail screen in Loan Delivery.

Considerations for Both Income Data Points

-

Provide gross income (before tax), not net income (after tax).

-

Negative monthly income will not be accepted.

-

Loan Delivery will not allow negative income to be entered. Fatal Edit 003 will be generated, stating, “The Monthly Income is required at delivery. Please enter a Monthly (or Qualifying) Income and re-Save the loan data.”

-

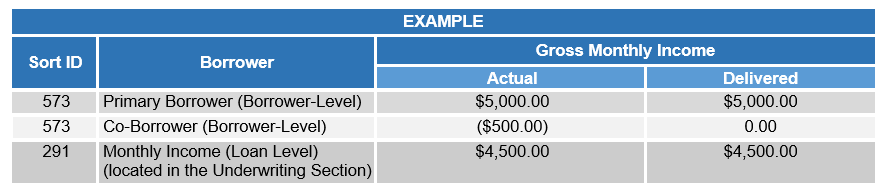

For self-employed borrowers who have negative income, lenders should:

-

provide “0” as the Qualifying Income for that borrower

-

deduct the negative amount from the Monthly Income (the total gross income for the loan).

-

See example below:

-

-

Refer to the Selling Guide for the requirements for self-employed borrowers and negative income.

-

How to Calculate DTI Ratio

The following ULDD attributes (Sort IDs) are used for debt-to-income (DTI) ratio calculations that are used in Loan Delivery for determining eligibility for purchase.

Loan Delivery Field Name |

ULDD Sort ID |

MISMO Data Point Name |

MISMO Definition |

FNMA Conditionality Details |

FNMA Implementation Notes |

|

Monthly Debt Expense |

290 |

TotalLiabilitiesMonthlyPaymentAmount |

The total monthly liabilities for all borrowers on the loan. |

Required for all loans |

Enter the sum of the monthly debt payment for all borrowers calculated in accordance with the Fannie Mae Selling Guide and using the TotalMonthlyProposedHousingExpenseAmount (Sort ID 292). Round to the nearest dollar. The only reasonable values supported at this time are restricted to a format of Numeric 5. |

|

Monthly Income |

291 |

TotalMonthlyIncomeAmount |

The total monthly income for all borrowers on the loan. |

Required for all loans |

Enter the sum of BorrowerQualityingIncomeAmount (Sort ID 573) for all borrowers. Round to the nearest dollar. The only reasonable values supported at this time are restricted to a format of Numeric 6. |

|

Monthly Housing Expense* |

292 |

TotalMonthlyProposedHousingExpenseAmount |

Insufficient Credit History |

Significant Errors Score |

When the PropertyUsageType (Sort ID 69) is PrimaryResidence:

When the PropertyUsageType (Sort ID 69) is Second Home or Investment, enter the sum of the primary housing expense for all borrowers, not the subject property housing expense. Round to the nearest dollar. The only reasonable values supported at this time are restricted to a format to five numeric digits. |

* TotalMonthlyProposedHousingExpense (Monthly Housing Expense) is not used in the DTI Ratio calculations, however there are scenarios where the TotalMonthlyProposedHousingExpense is used when determining the value provided in TotalLiablilitiesMonthlyPaymentAmount (Monthly Debt Expense).

NOTE: The above ULDD attributes should match the values used by DU to calculate the DTI ratio in DU. See the ULDD Specification (Appendix D) for additional information.

Rounding for DTI Ratio Calculations

At loan delivery, DTI ratio calculations to determine purchase eligibility use conventional rounding when converting to a percentage.

Calculated DTI Value |

Rounded DTI for Eligibility |

|

|

45.005% |

45% |

DTI value is rounded down to whole number, if the value after the decimal place is less than .5.

|

|

45.2134% |

45% |

|

|

45.4999% |

45% |

|

| 45.5000% | 46% | DTI value is rounded up to whole number, if the value after the decimal place is greater than or equal to .5. |

| 45.8976% | 46% | |

How to Deliver the Monthly Housing Expense

Monthly Housing Expense (Sort ID 292) is to be delivered with the total proposed housing expense related to the borrowers’ primary residence, regardless of the property usage type (primary residence, second home, or investment) of the subject loan. Include the housing expense of the primary residence of all non-occupant borrowers. This is the numerator of the loan’s Housing Expense-to-Income Ratio. When the subject loan is the borrower’s primary residence, the Monthly Housing Expense must be greater than or equal to the value delivered for Initial P&I (Sort ID 268). This field is located in the Underwriting section of the Loan Detail screen in Loan Delivery.

How to Deliver the Monthly Debt Expense

Monthly Debt Expense (Sort ID 290) is to be delivered with the combined monthly qualifying debt of all borrowers. This is the numerator of the loan’s Debt-to-Income Ratio. This field is located in the Underwriting section of the Loan Detail screen in Loan Delivery.