My web

Qualifying the Borrower

![]()

This document shows you the Qualifying the Borrower screens and explains how to enter some of the data.

You may scroll through this document, or click a link to be taken to the information for the specified field:

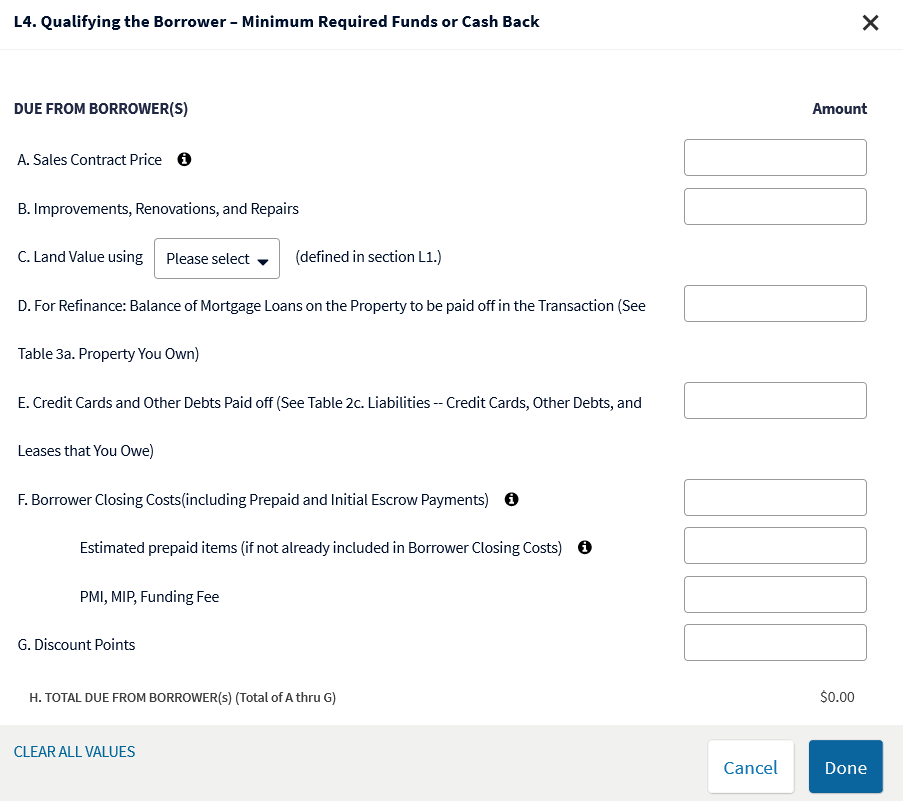

Qualifying the Borrower - Minimum Required Funds or Cash Back

Qualifying the Borrower - Minimum Required Funds or Cash Back

Here are the notes for the following fields:

|

Field Name |

Notes |

|

A. Sales Contract Price |

|

|

B. Improvements, Renovations, and Repairs |

|

|

C. Land Value using |

|

|

D. Balance of Mortgage Loans on the Property to be paid off in the Transaction |

|

|

E. Credit Cards and Other Debts Paid off |

|

|

F. Borrower Closing Costs and Estimated prepaid items |

|

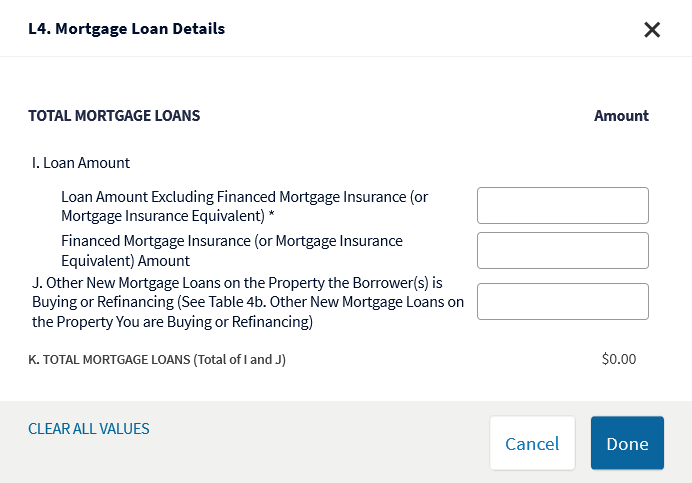

Mortgage Loan Details

Notes: The balance entered on the Other New Mortgage Loans on the Property the Borrower(s) is Buying or Refinancing (line J.) should match the total subordinate lien balance entered in section 4b. Other New Mortgage Loans on the Property You are Buying or Refinancing.

For any new HELOC(s) associated with the transaction, the balance entered on line J. should only include the drawn portion of the HELOC(s).

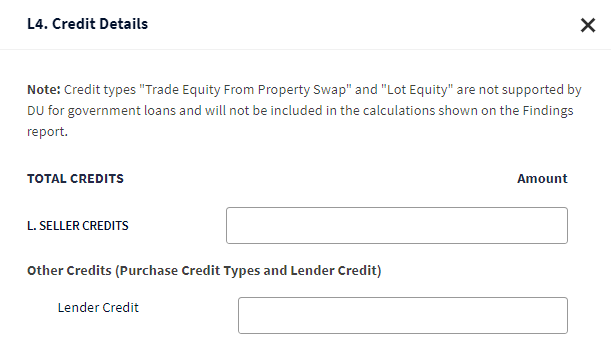

Credit Details

Note: The calculated total displayed in the M. Other Credits (Purchase Credit Types and Lender Credit) Total field includes the Other Credits that were entered in section 2b. Credits.

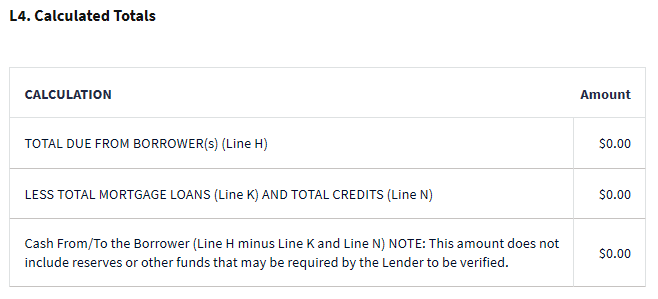

Calculated Totals

The information displayed in theL4.Calculated Totals section is automatically calculated for you based on the data input in the Qualifying the Borrower – Minimum Required Funds or Cash Back, Mortgage Loan Details, and Credit Details sections of the loan application.

Note: The amount displayed in Cash From/To the Borrower can be different than the Funds Required to Close amount on the DU Underwriting Analysis Report. For example, on a purchase transaction the balance of an installment debt marked To be paid off at or before closing in 2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe is not included in the amount displayed in Cash From/To the Borrower, but the balance will be included in the Funds Required to Close because an installment debt can't be paid off with a purchase transaction.