My web

Excess Interested Party Contributions

This document shows you how to enter excess interested party contributions (IPCs). This document is not intended to provide detailed instructions for entering loan application data in Desktop Underwriter® (DU®), but rather to provide you with an example of how to enter excess IPCs in DU.

As specified in the Selling Guide, maximum financing concessions must be calculated using the lower of the sales price or appraised value. Financing concessions that exceed the limits are considered sales concessions and must be deducted from the property's sales price.

The following is an example of how this must be reflected in DU.

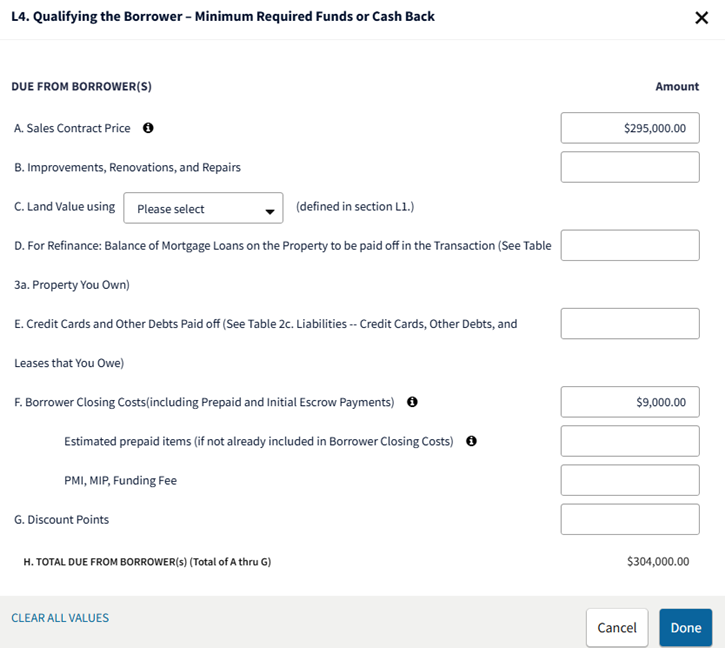

Sales Contract Price: $301,000

Appraised Value: $300,000

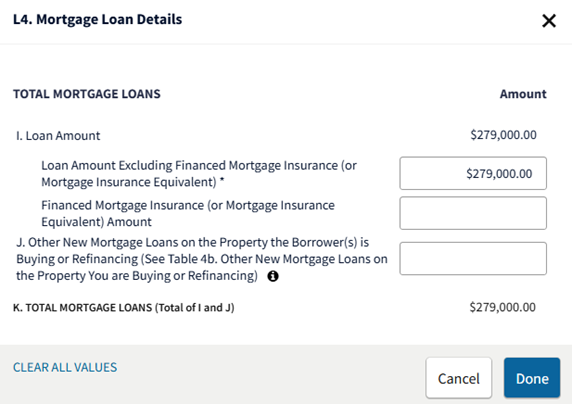

Loan Amount: $279,000

LTV = 93% (maximum financing concession = 3% of Appraised Value at $9,000)

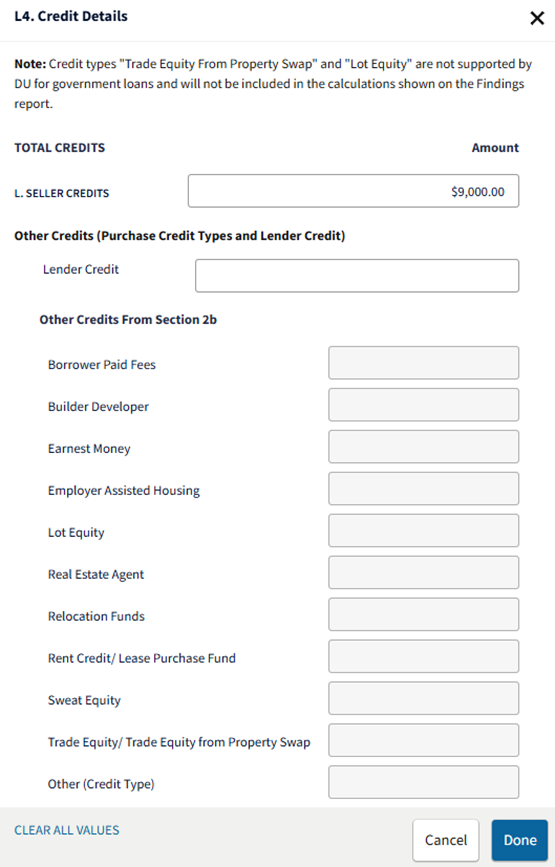

Seller paid closing costs: $15,000

Sales concessions: $6,000 (excess amount over allowable: $15,000 - $9,000)

The data entry for this example is displayed in the screens below:

Notes: The amount entered in A. Sales Contract Price was adjusted downward by the amount of the sales concession.

For transactions with a prorated real estate tax credit, only enter the borrower’s portion of the prorated real estate tax credit in DU. Do not enter the seller’s portion of the prorated real estate tax credit as a credit in DU.

Notes: The amount entered inL. Seller Credits was adjusted downward by the amount of the sales concession.

For transactions with a prorated real estate tax credit, do not enter the seller’s portion of the prorated real estate tax credit as a credit in DU.

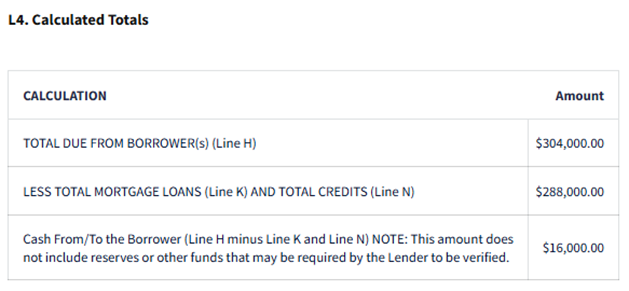

Note: The amount entered inA. Sales Contract Price was adjusted downward by the amount of the sales concession, and L. Seller Credits was adjusted downward by the same amount in order forCash From/To the Borrower to calculate correctly.