My web

Release of Liability

![]()

This document is not intended to provide detailed instructions for entering all the loan application data in Desktop Underwriter® (DU®). It shows you how to create a refinance loan casefile in DU to review a transferee’s credit and financial capacity when a borrower release of liability is requested. It explains the specific steps needed for entering the data for a release of liability.

A request for a release of liability may occur in connection with a transfer of the property to a new owner as described in the Servicing Guide.

When creating a loan casefile for a credit qualification for a release of liability you must only enter the information for the transferee(s) and/or the borrower(s) who will remain responsible for the loan. The order in which the transferee(s)/borrower(s) are entered does not impact the underwriting of the loan casefile.

To start, log in to DU. The Loan List is the first screen you see when you log in to DU. You can use the Loan List to create or import a loan casefile or to view a list of existing loan casefiles.

- To create a new loan casefile, click Create Loan.

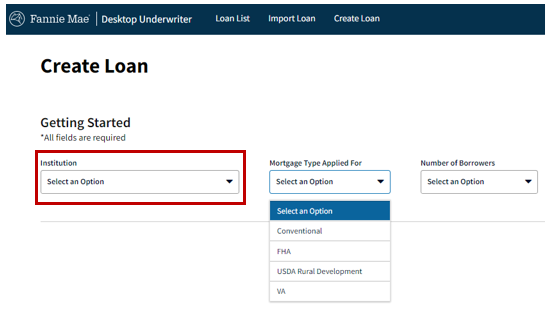

- On the Create Loan screen, select an Institution from the drop-down list. If you only have access to one institution, that is the only one you will see listed.

- In the Mortgage Type Applied For drop-down list, select the type of mortgage based on original terms of the loan.

- In the Number of Borrowers drop-down list, select the number of transferees and/or any borrower who will remain responsible for the loan.

- After you complete the first three fields, additional fields will appear to enter the personal information about the transferee(s) and/or any remaining borrower(s).

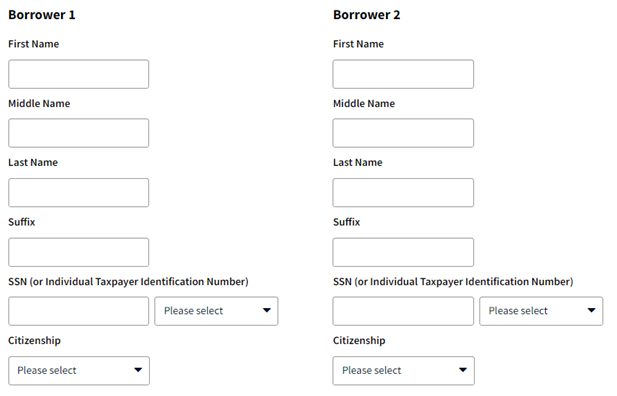

- Enter the name, SSN, or ITIN, and other applicable information for the transferee(s) and/or the borrower(s) who will remain responsible for the loan.

- Do not include the dashes in the SSN (or Individual Taxpayer Identification Number) field. Identify whether the number is an SSN and ITIN.

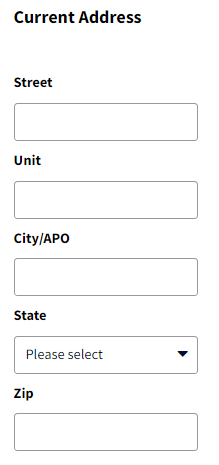

- Scroll down to the Current Address section to enter the address for each transferee and/or any remaining borrowers.

- Click Create Loan on the bottom right corner of the screen.

- You will be taken to the Loan Review screen.

Note: After entering the name, SSN or ITIN, and current address you can order or reissue their credit report, which is required for underwriting. For details, see Associating a Credit Report.

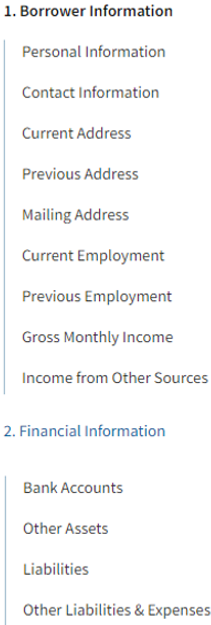

11. In the 1. Borrower Information and the 2. Financial Information sections, enter:

- The mailing address if different than the current address.

- The employment information including the self-employment information, if applicable.

- The monthly employment income and/or other income.

- The monthly debt obligations.

For details, see Borrower Information and Financial Information.

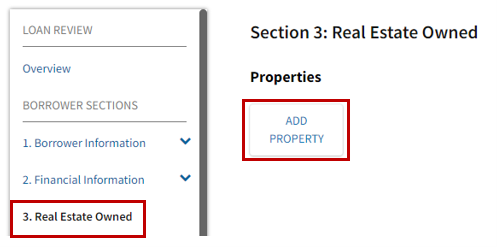

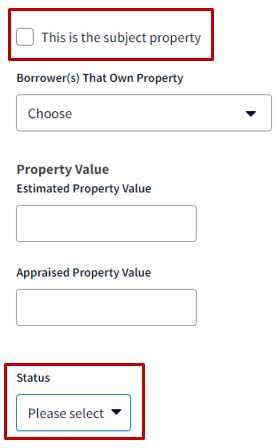

- In the 3. Real Estate Owned section, click the Add Property button.

- Enter the property information. Make sure to click the This is the subject property checkbox and select Retained from the Status field drop-down list. For more details, see Real Estate Owned.

Note: If this is a second home or investment transaction, the present housing expenses need to be included in the ratios. For details, see the Second home & Investment Property Transactions section in Debt-To-Income (DTI) Ratio Calculation Questions.

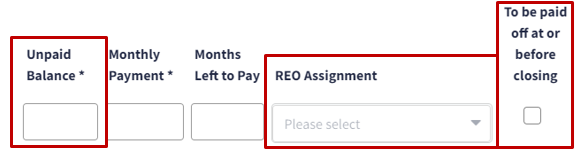

- If the lien being assumed with the transaction was not auto-populated on the 2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe screen it must be added. Do the following for the lien liability:

a. If needed, update the mortgage liability unpaid balance:

- If it is a fixed rate transaction, the balance is the original loan amount.

- If it is an ARM transaction, the balance is the current UPB.

Note: The unpaid balance should reflect all funds due at payoff, which could include but is not limited to, non-interest-bearing principal balance amounts.

b. Select the property from the REO Assignment field drop-down list.

c. Click the To be paid off at or before closing checkbox.

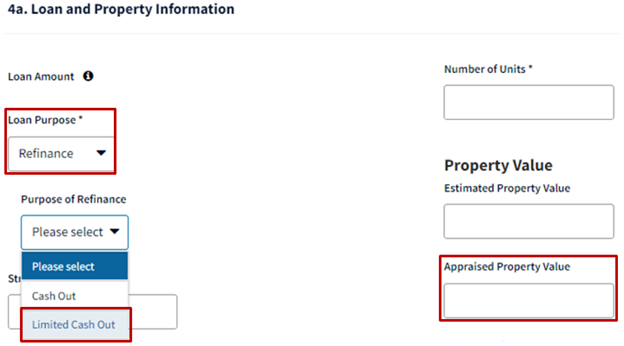

- On the 4a.Loan and Property Information screen, select Refinance from the Loan Purpose drop-down list and Limited Cash Out from the Purpose of Refinance drop-down list. In the Appraisal Property Value field, enter the original value of the property as defined in the Selling Guide. Complete the other applicable information, such as the number of units and occupancy. For more details, see Loan & Property Information.

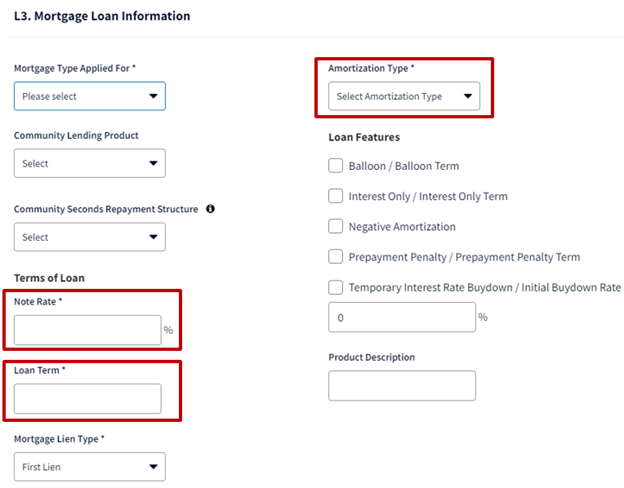

- On the L3. Mortgage Loan Information screen.

a. If it is fixed rate transaction:

- In the Note Rate field enter the interest rate based on original terms for the loan.

- In the Loan Term field enter the number of months based on original terms for the loan.

- In the Amortization Type field select Fixed Rate from the drop-down list.

b. If it is an ARM transaction:

- In the Note Rate field enter the interest rate based on current interest rate.

- In the Loan Term field enter the number of months remaining on the loan term.

- In the Amortization Type field, select Adjustable Rate from the drop-down list.

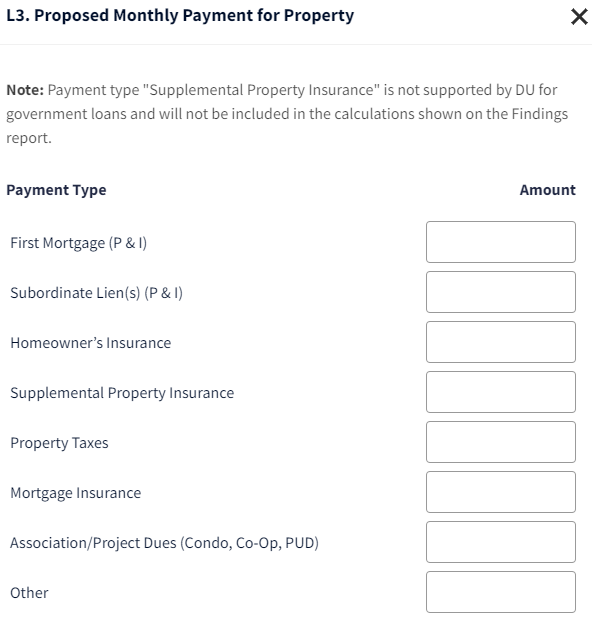

- On the L3. Proposed Monthly Payment for Property screen, enter the housing expenses associated to the subject property.

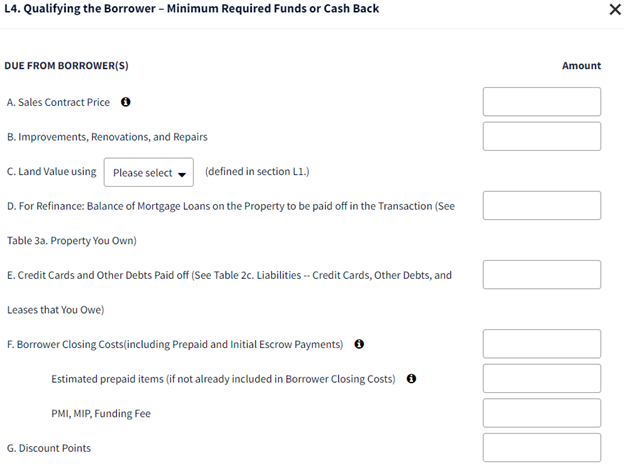

- On the L4. Qualifying the Borrower - Minimum Required Funds or Cash Back screen, only complete line D. If it is a fixed rate transaction, enter the original loan amount. If it is an ARM transaction, enter the current UPB.

Note: The amount should match the unpaid mortgage balance amount on the 2c. Liabilities - Credit Cards, Other Debts, and Leases that You Owe screen.

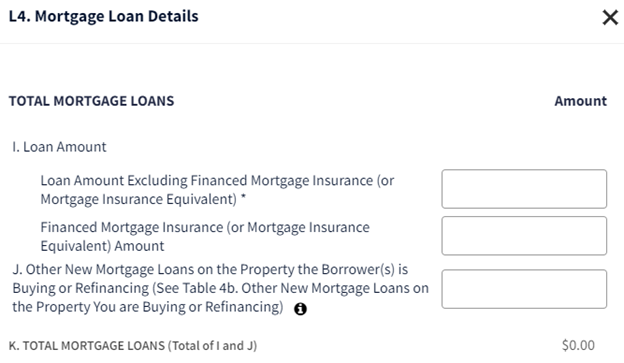

- On the L4. Mortgage Loan Details screen, only complete the Loan Amount field. If it is a fixed rate transaction, enter the loan amount based on original terms for the loan. It is an ARM transaction, enter the loan amount based on the current UPB.

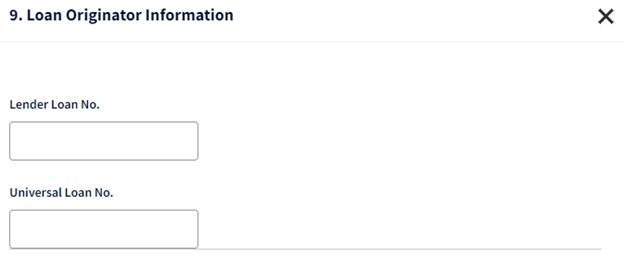

- On the 9. Loan Originator Information screen, enter original lender loan number in the Lender Loan No. field.

21. Complete all other required loan application information, such as the declarations. When finished, submit for underwriting if you have already associated a credit report, if not submit for credit and underwriting. For details, see Associating a Credit Report and Submitting for an Underwriting Recommendation.

Refer to the Selling Guide regarding DU recommendations.