My web

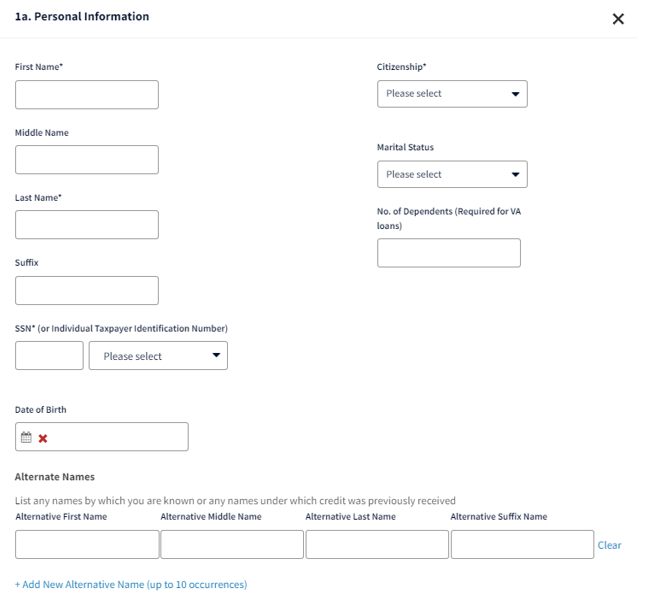

Borrower Information

![]()

This document shows you the Borrower Information screens and gives information about some of the fields.

You may scroll through this document or click a link to be taken to the specified screen.

Details

Here are the drop-down list options for the following fields:

|

Field Name |

Options |

|

Citizenship |

|

|

Marital Status |

|

Notes: If you create a loan, the borrower name and Social Security Number will be populated from the Create Loan screen. DU supports a maximum of four borrowers for conventional loans, but you can manually underwrite a loan with more than four borrowers.

If the borrower’s legal name does not consist of a separate first name or last name, the missing name field should include the signifier the borrower uses in other official documentation (if any). If no other signifier exists, since both a first and last name need to be provided from a technology perspective, at least one character should be entered in the missing name field (i.e., X, NA, etc.).

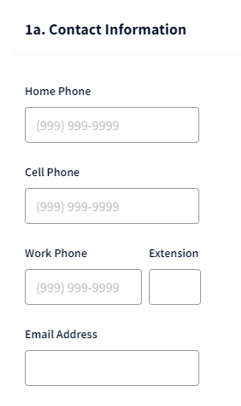

Contact Information

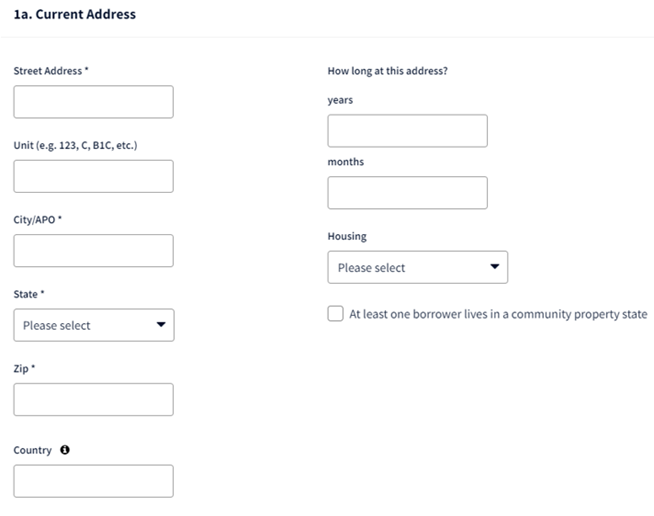

Current Address

Here are the drop-down list options for the following field:

|

Field Name |

Options |

|

Housing |

|

Notes: The current address must be within the U.S., U.S. territories, or an APO, FPO, or DPO military address in order to obtain a credit report that is compatible with DU loan casefile requirements. Borrowers with foreign credit reports must be manually underwritten.

If Rent is selected in the Housing field, the Rent Amount field will be displayed. Refer to the Second Home & Investment Property Transactions section in the Debt-To-Income (DTI) Ratio Calculation Questions job aid for information about entering rent.

If the transaction is eligible for the positive rent payment history to be considered in the DU risk assessment, the rent payment must be entered on this screen and the Verification of Asset report information must be entered on the borrower's Borrower Verification Reports screen. Refer to the DU Validation Service job aid. If the borrower’s rent has changed in the last 12 months for any reason (e.g. due to either moving, a rent increase or decrease, or the share of rent the borrower pays has changed) the amount of the previous rent should be provided as the rent amount under the Previous Address. This will assist DU in finding matching rent amounts for that 12-month period. If the borrower’s rent has changed while living at the same address, enter the address in both the Current and Previous Address sections, and the two rent amounts the borrower paid for the given time frames.

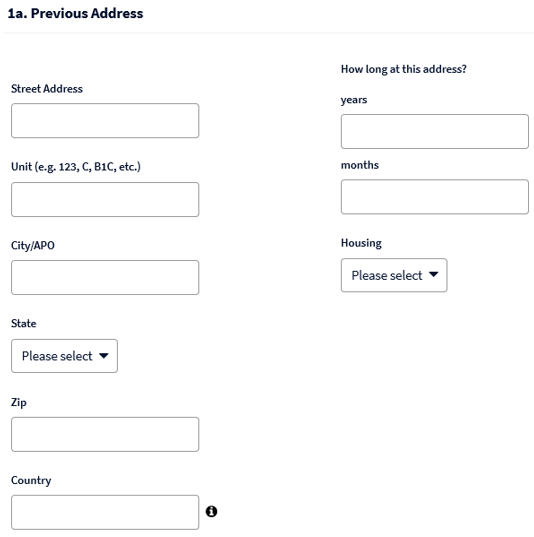

Previous Address

Here are the drop-down list options for the following field:

|

Field Name |

Options |

|

Housing |

|

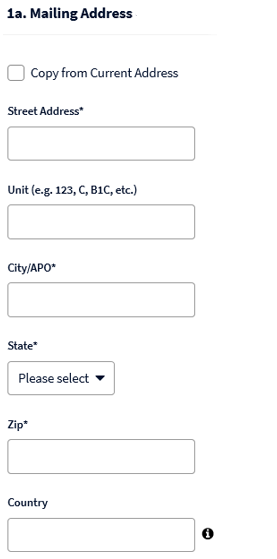

Mailing Address

Note: If the borrower's mailing address is the same as their current address, you can click theCopy from Current Address checkbox.

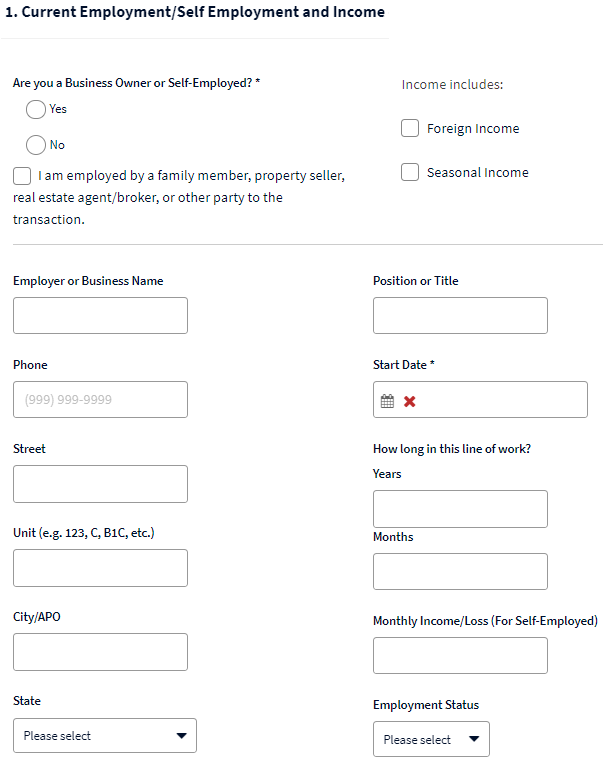

Current Employment

Here are the drop-down list options for the following field:

|

Field Name |

Options |

|

Employment Status |

|

Notes: Only actual employer information should be entered in the employment section of the loan application. For example, do not enter “retired” or “homemaker” as the borrower’s current employer.

Only one current primary employment will be used in underwriting, so if a borrower has more than one current employment, select one as the primary and the other one(s) as secondary.

DU will issue a verification message related to employment offers and contracts if the borrower's current employment start date is after the date the loan casefile was created.

If you click Yes for Are you a Business Owner or Self-Employed, two radio buttons will be displayed: 1) When I have an ownership of less than 25% is selected, DU will not consider the borrower self-employed (in accordance with the Selling Guide) or 2) When I have an ownership share of 25% or more is selected, DU will consider the borrower self-employed.

-

For borrowers with ownership of 25% or more the income must be entered on this screen (1. Current Employment/Self-Employment and Income) in the Monthly Income/Loss (for Self-Employed) field.

-

For borrowers with less than 25% ownership, the income must be entered in 1b. Current Gross Monthly Income.

-

For borrowers who are not self-employed, income must be entered in 1b. Current Gross Monthly Income.

-

Any income from other sources must be entered in 1e. Income from Other Sources

If you click Yes for Are you a Business Owner or Self-Employed?, the Income Calculator Reference Number field will be displayed. Additional information about Fannie Mae’s Income Calculator can be found on the Income Calculator page.

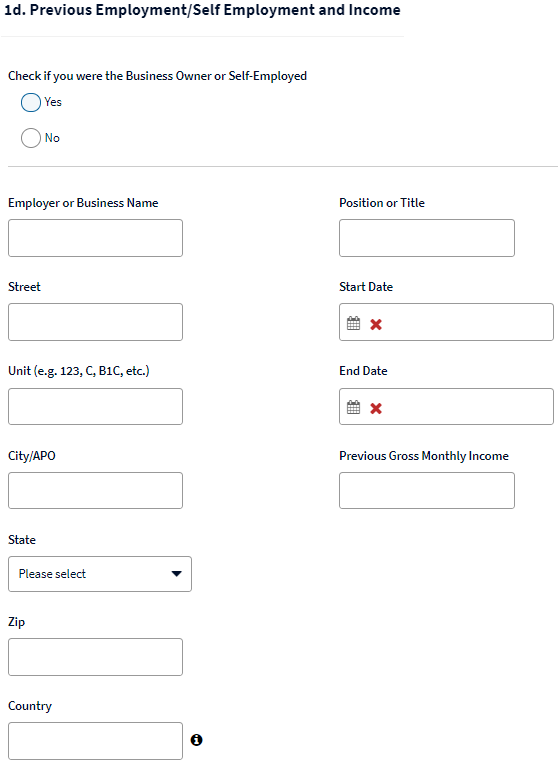

Previous Employment

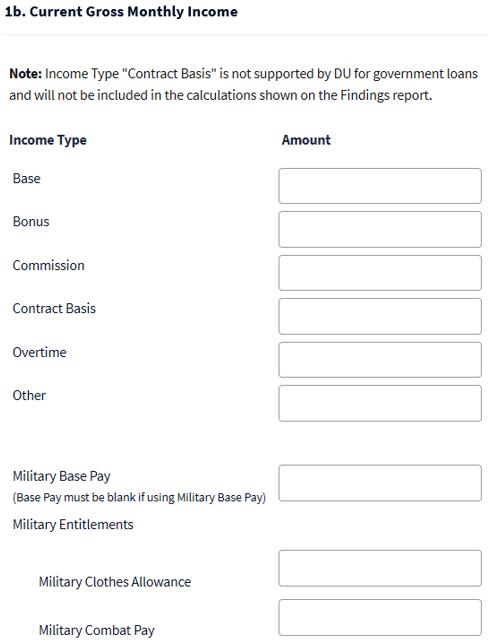

Gross Monthly Income

The additional military income fields not shown are Military Flight Pay, Military Hazard Pay, Military Overseas Pay, Military Prop Pay, Military Quarters Allowance,MilitaryRationsAllowance andMilitaryVariableHousingAllowance.

Notes: If the borrower is not self-employed or is self-employed with less than a 25% ownership share, enter their income on this screen. For borrowers with less than 25% ownership of a partnership, S corporation, or limited liability company (LLC), the Schedule K-1 income must be entered on this screen as Other.

If the borrower is self-employed with a 25% or more ownership share, enter their income on the 1. Current Employment/Self Employment and Income screen in the Monthly Income/Loss (For Self-Employed) field. Other types of income would be entered on the 1.e Income from Other Sources screen.

Income from Other Sources

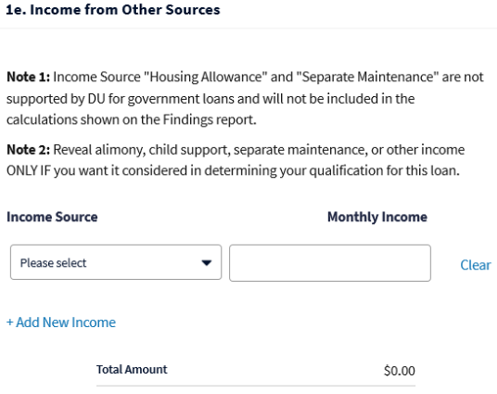

Here are the drop-down list options for the following field:

|

Field Name |

Options |

|

Income Source |

|

| Description (free-text sub-category when an Income Source of Other is selected) |

|

Notes: Other income must be entered in DU if it applies.

Only one of each other income source per borrower will be used in underwriting, so if a borrower has more than one of an other income source the amounts should be combined. For example, if a borrower has $2,600 monthly income from one retirement account and $2,400 monthly income from another retirement account, just one retirement income should be entered with a $5,000 amount.

If the borrower is required to make alimony or separate maintenance payments for more than ten months and you want to treat the obligation as a reduction to income, select Alimony or Separate Maintenance in the Income Source field and enter the amount of the alimony or separate maintenance obligation payment as a negative amount in the Monthly Income field. When the borrower also receives alimony or separate maintenance income, combine the amount of the alimony or separate maintenance income and the alimony or separate maintenance obligation payment and enter the net amount.

DU does not provide any unique messaging identifying the use of adjusted gross income. Refer to the Selling Guide for guidance on how to calculate adjusted gross income for nontaxable income.

Temporary Leave Income

When income from temporary leave is being used to qualify for the mortgage loan, the lender must enter the appropriate qualifying income amount into DU based on the requirements provided in B3-3.3-09, Temporary Leave Income.

- If the borrower will return to work as of the first mortgage payment date, the lender can consider the borrower's regular employment income in qualifying and must enter the income into DU using the applicable income type.

- If the borrower will not return to work as of the first mortgage payment date, but is able to qualify using the lesser of the borrower's temporary leave income (if any) or regular employment income, that “lesser of” income amount must be entered into DU.:

- If the borrower's temporary leave income is the lesser amount, enter the income amount into DU using the other income source Temporary Leave.

- If the borrower's regular employment income is the lesser amount, enter the income amount in DU using the applicable income type.

- If the borrower's temporary leave income is used and the lender is able to “supplement” the temporary income with available liquid reserves (per B3-3.3-09, Temporary Leave Income), the following must be applied:

- The lender must enter the combined temporary leave income and supplemental income from reserves in DU using the other income source Temporary Leave. The combination of these two amounts may not exceed the borrower's regular monthly employment income. DU is not able to determine that supplemental income is being used, nor is it able to determine the amount of reserves used to supplement the temporary income. As a result, the lender must manually reduce the amount of the borrower's total liquid assets by the amount of reserves used to supplement the temporary income (in order to avoid the reserves being used for both income and assets).