My web

Requesting Approval for a Modification

![]()

Note: The following functionality is also available in Servicing Management Default UnderwriterTM (SMDU) and SMDU UI.

When submitting a borrower’s Fannie Mae conventional loan for a modification that requires Fannie Mae approval, you must request approval in HomeSaver SolutionsTM Network (HSSN) Workout Profiler. Upon approval, Fannie Mae will inform you as to whether or not the estimated trial payment amount and modification terms being recommended have been accepted.

Follow the steps below to request Fannie Mae’s approval for a loan modification:

- Log into AMN/HSSN and click Fannie Mae’s Workout Profiler™ link.

The Create Case screen appears.

For details on logging in, refer to Accessing AMN/Home Saver Solutions Network.

If you have already created a case and saved it as a draft, click on the Query Draft Cases link from the HSSN Main Menu and finish entering the case details.Note: If the case was initially created utilizing the incorrect campaign code, you will need to delete the case and re-enter the information with the proper campaign code.

- Enter the Fannie Mae loan number in the +Fannie Mae Loan No field.

Select the state from the +State drop-down menu.

Select the appropriate campaign from the Campaign ID field. Refer to Fannie Mae Modifications – Campaign Codes as needed.Click Submit.

The Fannie Mae’s Workout Profiler screen appears.

- Complete the required fields on the Fannie Mae’s Workout Profiler screen by keying in data manually or selecting from the drop-down lists, as applicable.

The tables below will describe how to properly enter the modification recommendation.

In order to expedite Fannie Mae’s decision process, it is suggested that you also complete the non-required fields that are pertinent to the workout being requested. - Complete the Borrower(s) Information section.

Field Action +Last Name Enter the borrower’s last name. First Name Enter the borrower’s first name. SS# Enter the borrower’s Social Security number. - If there is a second borrower, populate the additional fields provided. If there are more than two borrowers, click the Add Additional Borrowers link.

- Complete the View General Information section.

Field Action +If zero or blank, please enter the Remaining Term on this Loan If auto-populated, verify that the number of months is correct. If incorrect or the field is blank, enter the number of months remaining until loan maturity. - Complete the Update General Information section.

Field Action Unpaid Principal Balance Auto-populated with the borrower’s unpaid principal balance amount based on the last UPB reported in the Loan Activity Report (LAR) at month end. This field cannot be updated. +Last Paid Installment Date Auto-populated with the LPI date reported in the LAR at month end. If additional payments have been posted to the loan, update this date to match the LPI on your system of record. +Projected Foreclosure Date Enter the scheduled or projected foreclosure sale date. +No. of Autos Enter the number of autos owned and/or leased by the borrower(s). +Estimated/Actual Market Value Auto-populated with the original value. Update field by entering the current market value of the property. +No. of People in Household Enter the total number of people, including borrower(s), in the household. Borrower Contribution Enter the contribution made by the borrower(s), if applicable. Occupancy Status Select the occupancy status from the drop-down list. +Escrow Balance (+/-) Enter only the amount of the escrow balance to be considered for capitalization.

Place a minus sign (-) in front of the amount if the balance is negative (over-drawn escrow). If you place a plus sign (+) before the amount, the system will assume there is a surplus and it will be carried over to the capitalization information.

Refer to Fannie Mae’s Single-Family Servicing Guide and related Announcements on requirements for establishing an escrow account for modified loans.

If this is a non-escrowed account and you advanced more than one year’s taxes before you turned it into an escrowed account, you can only capitalize one year’s worth of taxes prior to the LPI. You must work out a repayment plan with the borrower for the balance. Ensure you include the repayment plan as an expense and liability in the financials.Delinquent Interest Through Date Auto-populates with an assumption for the date of the first new modified payment. The servicer will need to adjust the first new payment date based upon the trial payment period. The first new payment date should be the month following the final trial payment date. +Monthly Escrow Payment Enter the total monthly escrow payment amount including any additional monthly escrow payments required to cure escrow shortages.

Since there are no specific fields to enter the detailed breakdown for the monthly escrow amount for taxes, property insurance, homeowner’s association fees, mortgage insurance (if applicable), or escrow shortages (if applicable), you must enter this information in the +Recommendation Comment field of the Servicer Recommendation section.Attorney Fees/Costs (not in escrow) Enter attorney fees and costs that are not in escrow. Estimated Hazard Insurance Proceeds Enter the estimated or actual hazard insurance proceeds (loss draft/hazard claim funds). - Complete the MI Information section.

You must determine if MI company approval is required before completing a modification.Field Action MI Company Name Select the MI company’s name from the drop-down list. MI Certificate No. Enter the MI certificate number. MI Percent Coverage Enter the coverage percentage as stated on the MI certificate. - Complete the Financial Analysis section by clicking on the Financial Worksheet link.

The Financial Worksheet screen is displayed. On this screen, you will enter the borrower’s assets, liabilities, and wages. - Select the borrower’s expense level (high, medium, or low) from the Range drop-down list at the top of the screen.

- Complete the fields in the Assets column.

Field Action Home This field is pre-populated based on the information you entered in the Update General Information section.

Edit the current market value in this field if necessary.Checking Accounts Enter the total amount from the most current checking account statements for all borrowers who will be making payment on the loan. Savings Accounts Enter the total amount from the most current savings account statements for all borrowers who will be making payment on the loan. Other Property Enter the total value amount for other properties owned by the borrowers. If other property loans appear on the credit report but no asset is given by the borrower, contact the borrower for clarification. Boats/RVs Enter the total value amount to include boats and recreational vehicles. If loans for these items appear on the credit report but no asset is given by the borrower, contact the borrower for clarification. IRA Enter the total amount to include IRAs for all borrowers who will be making payments on the loan. Retirement Accounts Enter total account balances. If pay stubs indicate deductions for a 401K account and the borrower has not indicated an asset, contact the borrower for clarification. Stocks/Bonds Enter the total amount from the completed Financial Statement. Other Asset Enter any other asset value amount borrowers may have in this section. It is not necessary to enter the value of life insurance policies, home furnishings, or clothing. Total Assets This field automatically calculates all of the assets you entered in the Assets column. - Complete the fields in the Liabilities column.

Field Action UPB Auto-populated based on the information you entered in the Updated General Information section.

Verify that the auto-populated data is correct. If not, you may update the fields with the correct amounts with the exception of the UPB.Delinquent Interest Escrow Balance (+/-) Attorney Fees/Costs (not in escrow) Other Property Enter the total monthly payment amount for all other mortgages on other properties declared by the borrower. If other mortgage loans are included in the credit report, contact the borrower for clarification and enter the most up-to-date data. Other Liens Enter the total payment amount of liens on property secured by the Fannie Mae loan. If other liens or judgments are included in the credit report, contact the borrower for clarification and enter the most up-to-date data. Auto Loan Enter the total payment amount for any auto loans listed on the credit report. If the borrower declared auto on the financial statement and no loans show up on the credit report, contact the borrower for clarification and enter the most up-to-date data. Credit Cards Enter the total monthly payment amount of all outstanding credit card balances as shown on the credit report. Personal Loans Enter the total monthly payment amount of all outstanding personal loans declared by the borrower on the financial statement. Homeowners Dues Enter the amount declared by the borrower on the financial statement. If you have information to indicate the property is a townhome, condo, or co-op and the borrower did not declare fees, contact the borrower for information on possible past due amounts and enter the most up-to-date data. Medical Enter the total monthly payment amount that may be listed on the credit report along with the amounts declared by the borrower on the financial statement. If hardship indicates current or recent illness and no medical liabilities are evident, contact the borrower for clarification and enter the most up-to-date data. Other Enter the total monthly payment amount for other liabilities not covered for which the borrower is responsible. Total Liabilities This field automatically calculates all of the liabilities you entered in the Liabilities column. Net Worth This field automatically subtracts total liabilities from total assets to determine the borrower’s net worth. - Scroll down and complete the Borrower(s) Pay Schedule fields for each borrower.

Field Action Borrower Enter the borrower’s name. Net Pay Enter the borrower’s net pay.

Ensure that you are entering the net pay in this field as HSSN automatically calculates the gross income.Frequency of Pay Select frequency of pay from the drop-down list.

To determine the borrower’s frequency of pay, look at the dates of the pay period on the borrower’s pay stub. This will tell you whether the borrower is paid weekly, every two weeks, or monthly. - Scroll down to the Monthly Income and Monthly Expenses section.

Use the following information to help you complete this section:- Credit reports, bank statements, or pay stubs.

- Conversations with the borrower.

-

The borrower’s completed Form 710 - Mortgage Assistance Application.

Note: If any expense, such as child support, is deducted directly from a borrower’s paycheck, do not enter it on this screen as the expense has already been accounted for in the net pay. If you enter it again here, you will be “double counting” that expense.

- Complete the fields in the Monthly Income column.

Field Action Monthly Net Wage This field is pre-populated based on the data you entered in the Borrower(s) Pay Schedule section above. Unemployment Do not enter unemployment income. Fannie Mae’s current guidelines do not allow use of unemployment insurance benefits or temporary sources of income for loans being evaluated for a modification. Disability Enter any amounts for disability as verified by letter, stubs, and/or deposits to bank accounts on statements. Child Support / Alimony Enter any amounts for child support and/or alimony verified by court order and/or deposits to bank accounts on statements. Rental Income Enter any amounts for rents received as verified by lease agreements and/or deposits to bank accounts on statements. 401K Enter any amounts for 401K income as verified by letter from the institution managing funds and/or bank accounts on statements. Stocks/Bonds Enter any amounts for stocks and/or bonds verified by stubs and/or deposits to bank accounts on statements. Other Enter any items of monthly income not addressed above that have been verified through a letter from source and/or deposits to bank accounts on statements. Total Income This field automatically calculates the total of all monthly income based on the information you entered in the Monthly Income column. - Complete the Monthly Expenses column. If discrepancies exist between the credit report and the financial statement completed by the borrower, contact the borrower for clarification.

Field Action P&I Pre-populated based on the information you entered in the Update General Information section. Escrow Payment Other Property Payments Enter the total monthly payments for loans on other properties declared by the owners and/or listed on the credit report. Other Liens Enter the total monthly payments for liens and/or judgments on property secured by a Fannie Mae loan. Auto Loan Enter the total monthly payments for auto loans. Auto Maintenance/ Insurance/ Fuel Pre-populated based on the information you entered in the Update General Information section.

Update the data in this field if necessary.Credit Cards Enter the minimum monthly payments shown on the credit report for credit cards.

If borrower has been through a bankruptcy and is not paying and/or credit cards are included in the bankruptcy, do not include in this field.Child Care Enter the total monthly payments provided by the borrower on the financial statement.

If the financial statement indicates dependents but there is no amount for child care, contact the borrower for clarification.Child Support / Alimony Enter the total monthly payments provided by the borrower on the financial statement as verified by court order and/or amounts credited from pay stubs or bank accounts on statements. Personal Loan Enter the total monthly payments provided by the borrower on the financial statement. Food Pre-populated based on the data that you entered in the Financial Worksheet section. Edit the data in these fields if necessary. Utilities / Telephone / Cable HOA Fees Enter the total monthly payments declared by the borrower on the financial statement. If you have information to indicate property is a townhome, condo, or co-op and the borrower did not declare fees, contact the borrower for clarification. Medical Enter the total monthly payments declared by the borrower on the financial statement and any amounts listed on the credit report due to medical providers. If the stated hardship indicates a recent illness and there are no medical expenses, contact the borrower for clarification. Other Enter the total monthly expenses not addressed above, declared by the borrower, or noted on the credit report. Include a reasonable amount in this field for entertainment, clothing, and miscellaneous expenses. Total Expenses This field automatically calculates the total expenses from the data entered in the Monthly Expenses column. Net Income This field automatically subtracts the borrower’s total expenses from the total income. - Click the Return to Profiler link located at the bottom left of the screen.

The Financial Analysis section is displayed.

The Monthly Total Income, Monthly Total Expenses, and Monthly Net Income After Expenses fields are auto-populated based on the data you entered on the Financial Worksheet section. - Scroll down to answer four questions before submitting the case.

Field Action Has the borrower indicated a desire to remain in the home and/or keep the property? Select Yes or No from the drop-down list. Are you aware of any structural and/or environmental problems with the property? Select Yes or No from the drop-down list.

If Yes is selected, you can provide details later in the process.Is the loan insured by the Veterans’ Administration? Select No from the drop-down list.

VA loans are not eligible for this modification program.If this case is related to a natural or national disaster, choose from the list: Select an appropriate response from the drop-down list, if applicable. - Once you have completed all required fields and ensured that the data is accurate, click Submit to save the case and submit it to Workout Profiler.

Or, you can choose one of the following options:- Click Save Draft to save the data you entered (your answers to the last four questions will not be saved). The screen will update to say, “Draft has been saved.” To retrieve your case, select Query Draft Cases from the HSSN Main Menu.

- Click Cancel. The case will be deleted from the system and you will be returned to the main Create Case screen.

- Click Reset. Any updates you made to the data will either disappear or revert to the default values.

The Loan Modification screen appears after clicking the Submit button.

-

Complete the Campaign Information section.

Note: Some fields that indicate a required field will not be required until Fannie Mae Loss Mitigation has reviewed and approved the case.

Field Action +Borrower Trial Execution Date Leave this field blank. +Trial Payment Amount Enter the estimated trial payment amount.

The estimated Trial Payment Amount should include PITI and a monthly escrow shortage payment (if applicable) and reflect an amount that will demonstrate the borrower’s ability to make the modified payment amount based on the modification terms being recommended by the servicer.+Property Value Amount Enter the current market value amount. Requested Principal Forbearance Amount Enter the amount you are recommending for principal forbearance, if applicable. Property Value Date Enter the completion date of the property valuation. If you complete the +Property Value Amount field, this field is required. If you fail to input the date, you will receive a hard edit and be unable to submit the case. +Property Value Source Select the value source from the drop-down list. After the case is submitted, upload the property valuation document as detailed in Step 7. +Servicer Initial Attestation Select Yes from the drop-down list after you have reviewed the initial attestation terms. - The Trial Period Payment Information and Trial Extension fields in this section are not completed until after Fannie Mae provides an approval of the proposed terms and trial payments are received.

- Complete the Recommended Loan Modification Terms section.

Field Action How will the Modification Fee be paid? The system defaults to Paid By Fannie Mae. +Product Type Select Fixed Rate or Step Rate from the drop-down list.

Based on your review, select the product that will best enable the borrower to repay the debt.

Note: Fannie Mae prefers a “Fixed Rate” solution. If recommending a “Step Rate” solution, please provide justification in the +Recommendation Comment field of the Servicer Recommendation section.+Payment Effective Date Enter the recommended first payment due date for the effective date of the modification.

When making a recommendation for the payment effective date of the modification, be sure to allow sufficient time for Fannie Mae to review the case and reply with a decision. You should also allow time to prepare required documents that need to be sent to the borrower for execution. The payment effective date of the modification should be the 1st of the month following the end of the trial period payments.

The payment effective date of the modification must take into consideration whether a loan needs to be reclassed. If the loan is not in an MBS pool, the first payment effective date of the modification must be the first day of the month following the last trial payment due date.

If the loan is in an MBS pool and must be reclassed, refer to the last section of this job aid entitled, “Reclassifying MBS Pool Loans” for further instructions.Workout Fee Auto-populated with the servicer’s incentive for completion of a successful modification.

Note: This field may not reflect the correct incentive fee. The amount will be corrected by Fannie Mae if applicable.Monthly Total Income Auto-populated based on data you entered in the Borrower’s Financial Worksheet in Workout Profiler.

Note: When available, it is preferred that the expense detail fields, including household/living expenses, are completed.Monthly Total Expenses Fannie Mae Calculated Gross Income Auto-populated based on Net Income entered. New Income Available After Expenses Auto-populated and is equal to the monthly income available to the borrower given current expenses and the new P&I after the modification. P & I Payment Amount Enter the payment and interest amount. The value in this field must match FM Calculated P&I Payment Amount.

Note: The P&I payment field must match the FM Calculated P&I Payment Amount for the first step and all subsequent steps if submitting a “step rate” solution.FM Calculated P&I Payment Amount This field is auto-populated. The amount is based on the term, interest, and modified UPB entered. Servicing Fee Auto-populated with the servicing fee. Note Interest Rate This rate should be the current interest rate on the loan, unless you are requesting a reduction.

Note: Fannie Mae prefers a “Fixed Rate” solution. If recommending a “Step Rate” solution, please provide justification in the Servicer Recommendation section in the +Recommendation Comment field.Maturity Date Auto-populated with the scheduled maturity date of the modified loan. New Term Auto-populated with the remaining term (shown in months) of what was entered on the Workout Profiler screen. You will need to adjust this based on the term of the new modified loan.

Note: Fannie Mae prefers extending the new modified term to 480 months.Excess Servicing Fee% If applicable, enter the excess servicing fee percentage or LPMI portion of the servicing fee for the modified loan. Generally, you should leave this field blank. Servicer Evaluation Date The date the servicer completed their evaluation and made the decision to move forward in offering the workout to the borrower. - Scroll down and complete the Loan Modification Calculations section.

Field Action Last UPB Reported to Fannie Mae This is the most current unpaid principal balance that has been reported to Fannie Mae.

It corresponds to the date in the Last LPI Reported to Fannie Mae field and must match the UPB and LPI on the servicer’s system.

Workout Profiler automatically populates the Last UPB Reported to Fannie Mae and Last LPI Reported to Fannie Mae fields, which are based on the LAR from Investor Reporting (IR).Last LPI Reported to Fannie Mae The most current last paid installment (LPI) date reported to Fannie Mae. LPI is not the date the last payment was received in office, but the due date of the last payment that was applied to the loan. - Principal Owed / Received Not Yet Reported Enter the principal received that has yet to be passed through to Fannie Mae as a positive value. If payments have been reversed since the LAR was reported to Fannie Mae, any principal owed that has yet to be reported to Fannie Mae should be entered as a negative value. = Current UPB (Before Capitalization) Displays UPB before capitalization.

This UPB must match the current UPB on your servicing system.+Current LPI (Before Capitalization LPI) Enter the most current last paid installment date only if it differs from what you entered in the Last LPI Reported to Fannie Mae field above. If this field is updated, the current UPB must also be updated to correspond with the current LPI.

This LPI must match the current LPI on your servicing system.+ Total Capitalized Amount This field is the sum of the Total Capitalized Interest + Total Capitalized Advances, which you will complete next. Please enter Capitalized Interest items in Breakdown of Capitalized Interest See Step 4. Please enter Capitalized Advances in Breakdown of Capitalized Advances New Modified UPB These fields will auto-populate after you have completed Step 4. New Modified LPI (Capitalized Interest To Date) - Click the Breakdown of Capitalized Interest link.

The Capitalized Details screen appears.

This screen is divided into two sections: Breakdown of Capitalized Interest and Breakdown of Capitalized Advances. - Complete the Breakdown of Capitalized Interest section.

Capitalized interest consists of delinquent interest, interest that’s owed or received but that you have not reported, and any contribution to delinquent interest from the borrower or mortgage insurance company.Field Action +From Date Auto-populated with the last LPI date reported. Update if applicable. +To Date Auto-populated as one month prior to the Payment Effective Date of the modification. Interest Owed/Recv’d Not Yet Reported Enter the interest received that has yet to be passed through to Fannie Mae as a positive value. If payments have been reversed since the LAR was reported to Fannie Mae, any interest owed that has yet to be reported to Fannie Mae should be entered as a negative value.

Complete this field only if the Principal Owed/Received Not Yet Reported was completed on the Enter Loan Modification Calculations screen.+Delinquent Interest (Should match FM’s calculated delinquent interest) If the pre-modification product type is a fixed rate loan, the delinquent interest you enter should match Fannie Mae’s delinquent interest calculation.

Only a $75.00 tolerance between the servicer’s calculated interest and Fannie Mae’s calculated delinquent interest is allowed.Fannie Mae’s Calculated Delinquent Interest For fixed rate loans, this field is auto-populated based on what you entered in the Current LPI and Payment Effective Date fields for the modification. This field is blank for ARM or other non-fixed rate loans. - Borrower / MI / Hazard Contribution to Delinquent Interest Enter the portions of the borrower’s, the MI’s and the Hazard Insurance contributions that are to be applied towards the total capitalized delinquent interest that is due. The value entered cannot be a negative number. = Total Capitalized Delinquent Interest Auto-populated as the Total Delinquent Interest – Borrower/MI Contribution to Delinquent Interest – Delinquent Interest Forgiven (if applicable). Delinquent Interest Comment (required only when Delq. Interest out of tolerance) Add notes here when there is more than a $75.00 variation between the servicer’s calculated interest and Fannie Mae’s calculated delinquent interest. - Scroll down and complete the Breakdown of Capitalized Advances section.

Field Action Attorney Fees/Costs Verify that the amount shown in the Attorney Fees/Costs field is accurate.

If necessary, update the value in this field. The value entered cannot be a negative number.

If the loan is in foreclosure or has been dismissed from bankruptcy, you would have entered the attorney’s fees in the General Information screen of Workout Profiler before submitting the case. That amount will auto-populate in the Attorney Fees/Costs field. Because this number may be greater than your current corporate advances, be sure that it’s accurate and includes any fees/costs that have been incurred but not yet billed.+/- Escrow Balance

( Negative Escrow Balance must be entered as a positive number)Enter the escrow amount to be capitalized (what is owed by the borrower) as a positive number. If the borrower has escrow reserves that have not yet been accounted for in Form 571, enter the amount as a negative number.

Refer to Fannie Mae’s Single-Family Servicing Guide and related Announcements on requirements for establishing an escrow account for modified loans.

If this was a non-escrowed account and you advanced more than one year’s taxes before you turned it into an escrowed account, you can only capitalize one year’s worth prior to the LPI. You’ll need to work out a repayment plan with the borrower for the balance. Be sure to include that repayment plan as an expense and liability in the borrower’s financials.+ Other The value entered cannot be a negative number. Enter zero if there are no ‘other’ advances.

Any amount entered in this field must be explained in the Recommendation Comment field.- Borrower / MI / Hazard Contribution to Advances Enter the portions of the borrower’s, the MI’s and the hazard insurance contributions that are being applied towards the total capitalized advances that are due.

In a pre-claim advance, also called a partial claim advance, the MI company brings the loan current and either enters into a repayment plan with the borrower to pay the amount back or reduces the final claim amount by the amount of the advance.

If they’re only advancing part of the arrearage, that counts as a contribution toward the modification. If the borrower enters into a repayment plan with the MI company, you must add that monthly payment and liability to their financials.- Disbursements Forgiven Do not enter anything in this field. = Total Capitalized Advances Auto-populated with the Attorney Fees/Costs + Escrow Balance + Other – Borrower/MI Contribution to Advances – Disbursements Forgiven. MTMLTV The amortizing Market to Market Loan to Value is based on the property value and data you entered in New Modified UPB field. -

Click on the Return to Capitalization Summary link.

The Loan Modification Calculations section is displayed.

The following fields auto-populate based on the data you entered on the Capitalization Detail screen.- Breakdown of Capitalized Interest

- Breakdown of Capitalized Advances

- New Modified UPB

- New Modified LPI (Capitalized Interest To Date)

- Review all the numbers in the Loan Modification Calculations section. Since these are the figures that Fannie Mae uses to review your recommendation, you’ll want to make sure that the information is accurate.

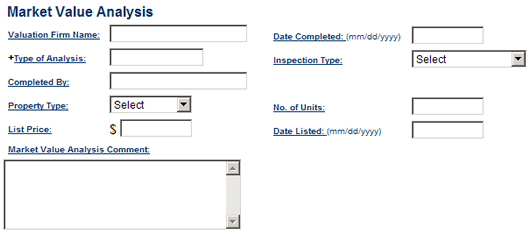

- Scroll down and complete the Market Value Analysis section as shown. Use the corresponding table below the screen shot to complete the fields.

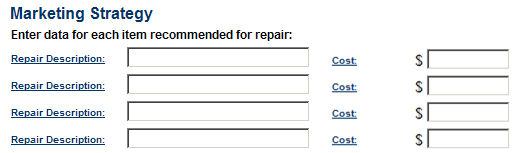

Field Action Valuation Firm Name Enter the name of the firm that completed the valuation. Leave this field blank if you are using an AVM. Date Completed Enter the date that the valuation was completed. +Type of Analysis Auto-populated from the Property Value Source field. Inspection Type Select the inspection type used in completing the valuation from the drop-down list. For an AVM, select No Inspection from the drop down box. Completed By Enter the name of the person who completed the valuation. For an AVM, leave this field blank. Property Type Select the property type from the drop-down list. No. of Units Enter the number of units that comprise the subject property (1-4). List Price If the subject property is currently listed with a realtor, enter the current list price. Date Listed If the property is currently listed, enter the date on which the property was first listed. Market Value Analysis Comment Enter any comments regarding the valuation. - Scroll down and complete the Marketing Strategy section as shown. Us the corresponding table below the screen shot to complete the fields.

Field Action Repair Description Enter a description for any recommended repairs noted for the property, if provided in the valuation document. Cost Enter the estimated cost for the repair type selected.

Repeat above steps for additional repairs if necessary. - Complete the Probable Final Value section.

Field Action +As Is Auto-populated from the +Property Value Amount field As Repaired Enter the repaired value, if provided in the valuation document. - Complete the Recommended Contributions section.

Field Amount Cash Contribution Enter the amount of cash the borrower is contributing to reduce the loss to Fannie Mae.

The amount in the Cash Contribution field must match the sum of the Borrower/ MI / Hazard Contribution to Delinquent Interest and Borrower/ MI / Hazard Contribution to Advances.

Note that the other fields in this section are not applicable to modifications. - Complete the MI Information section.

- Check with the MI company to see if they require approval for the modification.

Field Action MI Company Name Select the MI company’s name from the drop-down list. MI Certificate No. Enter the MI certificate number. MI Percent Coverage Enter the percent of coverage as stated on the MI certificate. MI Contact Name Enter the name of the primary MI contact for this case. Phone Enter the phone number of the primary MI contact for this case. MI Decision Select an MI decision (Approved, Declined, Pending, etc.) from the drop-down list. Decision Detail Select a reason (No Legitimate Hardship, Had Assets and Refused to Contribute, etc.) for the MI company’s decision from the drop-down list. MI Contribution Enter the dollar amount of any contribution that the MI is required from the borrower(s). MI Decision Comment If the MI approval is conditional on anything, such as a closing date, net proceeds, a borrower contribution or a limit on the modified UPB, enter those conditions here. - Complete the Hardship Reason(s) section.

Field Action +Select Hardship Reasons (At least one must be selected) Select at least one hardship reason from the drop-down list. You can select up to two additional hardship reasons if necessary. Hardship Reason Comment Enter additional commentary about the hardship to explain the reasons for the delinquency. - Complete the Contact Information section.

Field Action +Servicer Contact Name Enter the name of the loss mitigation contact in your shop that is responsible for this case. +Phone Enter the phone number of the servicer contact. Extension Enter the phone extension of the servicer contact, if applicable. Fax Enter the fax number of the servicer contact. +Email Enter the email address of the servicer contact. Email is Fannie Mae’s preferred method of communication to request additional information from servicers and to inform them of final decisions. NOTE: As a reminder, you must use a company email address and not a personal email address when submitting a case. Using a personal email address is a violation of our Non-Public Information (NPI) Policy and could result in delays of the review process. Attorney Contact Name Enter the name of the foreclosing attorney representing the servicer in this case, if applicable. Phone Enter the phone number of the foreclosing attorney representing the servicer in this case, if applicable. - Complete the Servicer Recommendation section.

Field Action +Recommended Decision Select Approve from the drop-down list. +Recommendation Comment Enter comments to support your recommendation.

List the monthly payment amounts for taxes, property insurance, HOA dues and MI (if applicable) in this field and label accordingly. If the borrower is currently on a repayment plan to cover any escrow shortages, provide the terms of the plan in this field.

Provide as much information and detail as possible as to why the borrower is a good candidate for a loan modification so that Fannie Mae can make an informed decision. Include details about their hardship (including confirmation of resolution of hardship) or other pertinent information about the property’s status.

If an amount greater than zero (0) is entered in the + Other advances field, a breakdown will need to be provided in this field. - Click Submit to send the case to Fannie Mae for review.

The message, “The Case has been submitted successfully!” appears.

Fannie Mae will review the case and contact you with any questions. - You must contact the borrower to:

- get answers to any questions Fannie Mae has raised,

- offer them the terms we have discussed, and

- get the borrower’s verbal agreement once Fannie Mae has approved the terms of the modification.

- Fannie Mae will approve the case when the terms of the modification are agreed to. If the case is not approved, Fannie Mae will inform you by issuing a denial letter. You will need to communicate the modification decision to the borrower and review the case for other workout alternatives and/or communicate the declination as applicable, per state and federal laws.

- Ensure that you report any trial period payments received. Refer to Reporting Monthly Trial Period Payments for details on how to enter trial period payments in HSSN.

- Once all trial period payments are received, submit the final attestation and close the case in HSSN. Refer to Submitting the Final Attestation to Fannie Mae for Successful Trial Periods and Closing the Case Using HSSN for details.

- Upload BPO/Appraisal/AVM or other required documents in HSSN to support the case you submitted in Workout Profiler. If the property is listed for sale, please note that the value cannot be provided by the listing or selling agent in the transaction.

- Save the BPO/Appraisal/AVM or other required documents to your computer as a PDF file.

- From the Asset Management Network home screen, click Query Manager located under the Home Savers Solutions Reporting section.

The Query Manager screen appears. - Enter the Fannie Mae Loan No. or Servicer Loan No. in the appropriate field.

The Query Manager – Results screen appears. - Click on the Case Number link associated with the case you submitted through HSSN.

The Case Information screen appears. - In the Upload Case Document section, click Browse to search your computer for the document you want to upload.

The Choose file window opens in a new window. - Select the file location from the Look in drop-down list.

- Select the file name from the File name drop-down list.

- Click Open.

The document name appears in the field to the left of the Browse button in the Upload Case Document section. - Click Upload.

If the document was successfully uploaded, a note will appear at the top middle of the page saying that the document was successfully uploaded.

If there were any issues with uploading the documents, you will receive an error message stating why the document could not be uploaded. Documents must be in PDF format and smaller than 5MB. Larger documents may require separation to upload in smaller segments, i.e. appraisals with photos.