My web

Requesting Approval for a Deed-in-Lieu (Mortgage ReleaseTM) Case in Workout Profiler

![]()

Note: The following functionality is also available in Servicing Management Default UnderwriterTM (SMDU) and SMDU UI.

A borrower incentive may be available for borrowers who are willing to vacate their property. Payment is not made until after the property is vacant, a property inspection has been conducted to confirm that the property has been left in acceptable condition, and the executed deed has been accepted by the servicer.

There are benefits to a Mortgage ReleaseTM, especially when compared to foreclosure, such as:

- Possible borrower incentive fees.

- Fannie Mae receives the property sooner than we would by going through foreclosure.

- The property is likely to be in better condition and the borrower(s) may be able to make a contribution to reduce the potential loss.

Follow the steps below to request Fannie Mae’s approval for a Mortgage Release.

-

Log into AMN/HSSN and click on Fannie Mae’s Workout Profiler.

-

If you haven’t done so already, create and submit the case as explained in Entering and Submitting a Case to Workout Profiler job aid.

If you have already created a case and saved it as a draft, click on the Query Draft Cases link from the HSSN Main Menu. Finish entering case details and then click Submit.

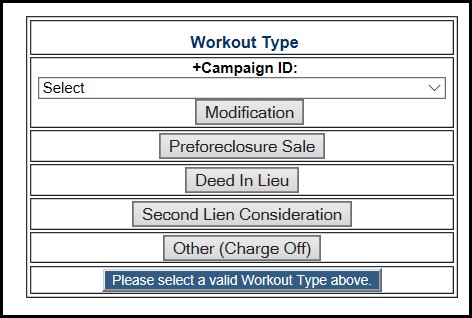

The Workout Profiler Options screen appears.

If your borrower does not want to remain in the property and has agreed to turn it over to you, you can submit a Mortgage Release™ request.

-

On the Workout Profiler Options screen, click Deed-in-Lieu.

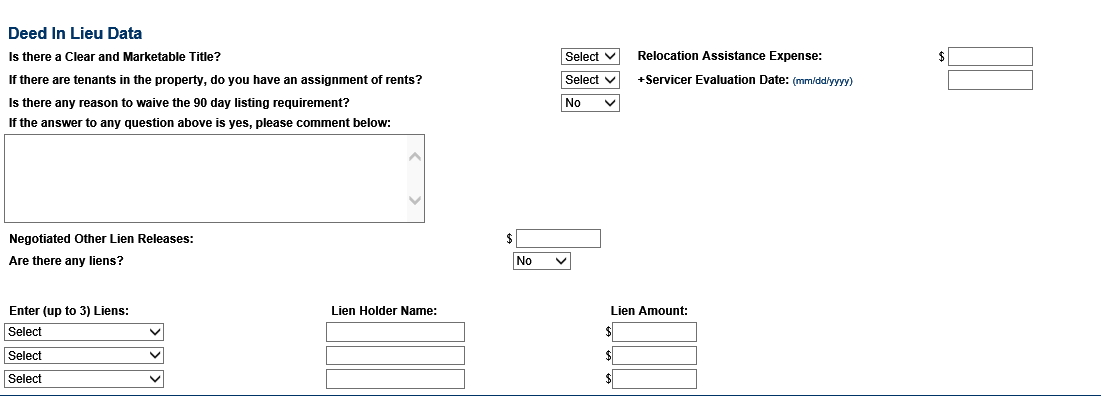

The Deed-in-Lieu Data screen appears.

You will complete this screen in the sections described below. Field names preceded by a plus sign (+) are required fields and must be completed.

Complete the Deed in Lieu Data section as shown. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +Is there a Clear and Marketable Title? | Select Yes as the title should be clear of any liens or judgments. The title must be clear and marketable; that is, the property must be delivered to Fannie Mae with no liens or judgments attached. If the title has a junior lien against it, the servicer should work with the borrower and the junior lien holder to ensure that the title is clear. If it’s in Fannie Mae’s best interest, we may agree to pay an aggregate amount of $6,000 to address eligible subordinate liens in exchange for their agreement to release the lien. In the event of foreclosure when the property is worth less than the first mortgage debt, a junior lien holder would not receive any proceeds from the sale. This can incent a junior lien holder to accept a reduced amount and agree to release the lien, rather than have the junior lien extinguished through foreclosure. Tax liens and some homeowner or condominium association liens have priority over the mortgage lien and would survive a foreclosure. Fannie Mae cannot accept a Mortgage Release™ if the title is not clear and marketable. |

| If there are tenants in the property, do you have an assignment of rents? | Select Yes or No from the drop-down list. Unless a transition option is being pursued, a single-family property must be vacant at the time the deed is executed, regardless of whether it’s owner- or tenant-occupied. If it’s a 2-4 family property, we generally allow tenants to remain as long as rents are assigned to us and at least one unit of the property is vacant; however, this arrangement is subject to approval by our National Property Disposition Center. |

| Is there any reason to waive the 90- day listing requirement? | Select Yes or No from the drop-down list. |

| If the answer to any question above is yes, please comment below. | Provide comments if necessary. |

| Relocation Assistance Expense | Enter ALL Borrower Relocation Assistance in this field. Enter the amount that may be paid to the borrower(s) for relocation expenses by the servicer. Offer the full relocation incentive amount the borrower qualifies for minus any required deductions. |

| Servicer Evaluation Date | Non SMDU Users: The date the servicer completed its evaluation and made the decision to move forward in offering the workout to the borrower. SMDU Users: The date that corresponds with the SMDU Transaction ID used to create the HSSN case for the workout. This is the Transaction ID associated with the pre-qualifying call. |

| Negotiated Other Lien Releases | Populates based on the liens entered if the servicer negotiated with the junior lien holder(s) for an amount to be paid through proceeds. |

| Are there any liens? | Select Yes or No from the drop-down list. |

| Enter (up to 3) Liens | If there are subordinate liens, click on the drop-down list to select the lien type. You may enter up to three liens. |

| Lien Holder Name | If there are subordinate liens, enter the name of the company or agency holding the subordinate lien. |

| Lien Amount | If there are subordinate liens, enter the total debt for each lien. |

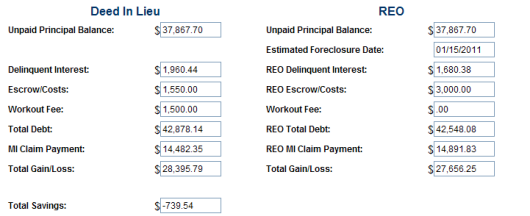

- Scroll down to complete the Deed in Lieu and REO comparison section. Use the corresponding table below the screen shot to complete the fields. By completing this comparison, you can determine if accepting a deed will be more beneficial over foreclosure. The Mortgage Release figures are current numbers, while the REO figures are based on the projected foreclosure date. All of these fields are automatically populated from information you’ve previously entered. You’ll need to get an interior/exterior appraisal or an interior BPO and submit this information to Fannie Mae along with the case. BPOs and appraisals must have clear – and preferably color – photos of the interior/exterior.

| Deed in Lieu | REO | |||

| Field | Action | Field | Action | |

| Unpaid Principal Balance | Enter unpaid principal balance. | Unpaid Principal Balance | Enter unpaid principal balance. | |

| N/A | N/A | Estimated Foreclosure Date | Enter estimated foreclosure date. | |

| Delinquent Interest | Enter delinquent interest. | REO Delinquent Interest | Enter estimated delinquent interest. | |

| Escrow/Costs | Enter escrow / costs. | REO Escrow/Costs | Enter estimated escrow/costs. | |

| Workout Fee | Leave blank | Workout Fee | Leave blank | |

| Total Debt | Enter total debt. | REO Total Debt | Enter estimated total debt. | |

| MI Claim Payment | Enter MI claim payment. | REO MI Claim Payment | Enter estimated MI claim payment. | |

| Total Gain/Loss | Enter total gain / loss. | Total Gain/Loss | Enter estimated total gain/loss. | |

|

Total Savings |

Enter total savings. |

|||

- Scroll down to complete the Streamlined Documentation section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +Streamlined Documentation | Select Y for Yes if streamlined documentation is being used. Otherwise, Select N for No. |

| Last LPI Reported to Fannie Mae | This field auto-populates and cannot be changed. |

| +User Entered LPI Date | Enter the date of the last paid installment. |

| +Property Type | Select the property type from the drop-down menu. |

| +Occupancy Status | Select the occupancy status from the drop-down menu. |

| +Projected Foreclosure Date | Enter the projected foreclosure date. |

| +Is Projected Foreclosure Date Actual/Estimate | Select whether the projected foreclosure date is an actual or estimated date from the drop-down menu. |

| Most Recent Representative FICO Score | Enter the most recent FICO score. |

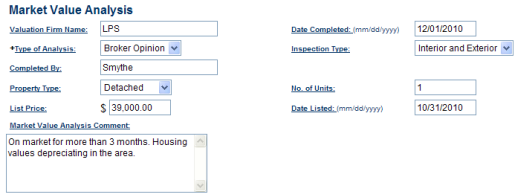

- Scroll down and complete the Market Value Analysis section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| Valuation Firm Name | Enter the name of the firm that completed the valuation. |

| Date Completed | Enter the date that the valuation was completed. |

| +Type of Analysis | From the drop-down list, select the type of analysis that was completed. |

| Inspection Type | Select the inspection type used in completing the valuation from the drop-down list. |

| Completed By | Enter the name of the person who completed the valuation. |

| Property Type | Select the property type from the drop-down list. |

| No. of Units | Enter the number of units that comprise the subject property (1-4). |

| List Price | If the subject property is currently listed with a realtor, enter the current list price. |

| Date Listed | If the property is currently listed, enter the date on which the property was first listed. |

| Market Value Analysis Comment | Enter any comments regarding the valuation. |

- Scroll down and complete the Marketing Strategy section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| Repair Description | Enter a description for any repairs done to the property. |

| Cost | Enter the estimated cost for the repair type selected. Repeat above steps for additional repairs if necessary. |

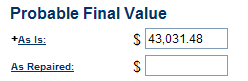

- Scroll down and complete the Probable Final Value section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +As Is | Auto-populated with a value based on the origination value, origination date, and market conditions in the property area. For a DIL case, the probable final “As Is” value from the current appraisal or BPO should be entered in this field. |

| As Repaired | If the appraisal specifies a repaired value, enter that value in this field. |

- Scroll down and complete the Recommended Contributions section. Use the corresponding table below the screen shot to complete the fields.

| Field | Amount |

| Cash Contribution | Amount of cash the borrower is contributing to reduce the loss to Fannie Mae. If the borrower has the ability to make a contribution against our loss, enter the Cash Contribution amount. If the borrower had a Ch. 7 bankruptcy discharge that included this property, a contribution cannot be requested without a reaffirmation agreement. If Fannie Mae is made whole but the MI company requires a contribution, enter that in the MI information section, not here. If Fannie Mae is not made whole, any borrower contribution comes to us to reduce our loss, which reduces the MI claim. |

| Estimated Hazard Claim Proceeds | Enter insurance proceeds if applicable. |

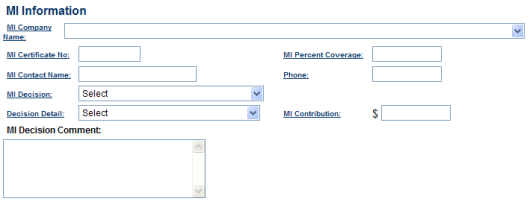

- Scroll down and complete the MI Information section. Use the corresponding table below the screen shot to complete the fields as applicable.

| Field | Action |

| MI Company Name | Select the MI company’s name from the drop-down list. |

| MI Certificate No. | Enter the MI certificate number. |

| MI Percent Coverage | Enter the percent of coverage as stated on the MI certificate. |

| MI Contact Name | Enter the name of the primary MI contact for this case. |

| Phone | Enter the phone number of the primary MI contact for this case. |

| MI Decision | Select an MI decision (Approved, Declined, Pending, etc.) from the drop-down list. |

| Decision Detail | Select a reason (No Legitimate Hardship, Had Assets and Refused to Contribute, etc.) for the MI company’s decision from the drop-down list. |

| MI Contribution | Enter the dollar amount of any contribution that the MI is required from the borrower(s). |

| MI Decision Comment | If the MI approval is conditional on anything, such as a closing date, net proceeds, or a borrower contribution, enter those conditions here. |

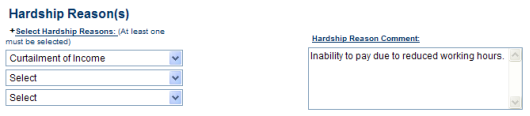

- Scroll down and complete the Hardship Reason(s) section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +Select Hardship Reasons (At least one must be selected) | Select at least one hardship reason from the drop-down list. You can select up to two additional hardship reasons if necessary. |

| Hardship Reason Comment | Enter additional commentary about the hardship to explain the reasons for the delinquency. We need to know why the borrower stopped making payments and what has changed in the borrower’s situation that will enable him/her to resume payments. |

- Scroll down and complete the Contact Information section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +Servicer Contact Name | Enter the name of the loss mitigation contact. |

| +Phone | Enter the servicer’s phone number. |

| Extension | Enter the servicer’s phone extension, if applicable. |

| Fax | Enter the servicer’s fax number. |

| Enter the servicer’s email address. Email is Fannie Mae’s preferred method of communication to request additional information from servicers and to inform them of final decisions. If you don’t provide an email address, you can get approval letters directly from the HSSN main page using the Query Case Letters function. NOTE: As a reminder, you must use a company email address and not a personal email address when submitting a case. Using a personal email address is a violation of our Non-Public Information (NPI) Policy and could result in delays of the review process. |

|

| Attorney Contact Name | Enter the name of the foreclosing attorney representing the servicer. |

| Phone | Enter the phone number of the foreclosing attorney representing the servicer. |

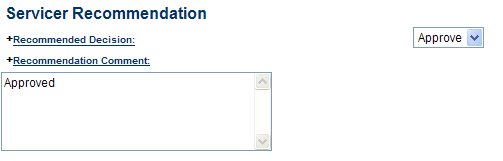

- Scroll down and complete the Servicer Recommendation section. Use the corresponding table below the screen shot to complete the fields.

| Field | Action |

| +Recommended Decision | Select Approve or Decline from the drop-down list. |

| +Recommendation Comment | Enter comments to support your recommendation. Provide as much information is possible so that Fannie Mae can make an informed decision. Enter additional important notes regarding the case. |

- Click Submit to send the case to Fannie Mae for their review.

Fannie Mae will review the case to see if it meets our guidelines for approval and inform you of a decision via email.

In the event that Fannie Mae incurs a financial loss due to the DIL, the borrower may be required to make a contribution in accordance with Fannie Mae guidelines.

If the borrower is unwilling to make the suggested contribution, Fannie Mae may agree to accept the Mortgage Release if it makes economic sense to do so.

- Upload the BPO/Appraisals documents in HSSN to support the case you submitted in Workout Profiler. If there is a 30% or more decrease in value since origination, you will need to order a second valuation. Please note that the value cannot be provided by the listing or selling agent in the transaction.

- Save the appraisal document to your computer as a PDF file.

- From the Asset Management Network home screen, click Query Manager located under the HSSN Reporting section.

The Query Manager screen appears.

- Enter the Fannie Mae Loan No. or Servicer Loan No. in the appropriate field and click Submit.

The Query Manager – Results screen appears. - Click on the Case Number link associated with the case you submitted through HSSN.

Case Information screen appears. - In the Upload Case Document section, click Browse to search your computer for the document you want to upload.

- The Choose file window opens in a new window.

- Select the file location from the Look in drop-down list.

- Select the file name from the File name drop-down list.

- Click Open. The document name appears in the field to the left of the Browse button in the Upload Case Document section.

- Click Upload.

If the document was successfully uploaded, a note will appear at the top middle of the page indicating that the document was successfully uploaded. If there were any issues with uploading the documents, you will receive an error message stating why the document could not be uploaded.

Once you have received an approval from Fannie Mae, follow the steps below.

If the case was not approved, no further action is required.

After You Submit the Case

-

Retain the executed Personal Property Release Form in the servicing file.

-

The attorney handling the transaction should review the subject property’s title commitment that can be upgraded to a title insurance policy once the loan is with the Fannie Mae REO department. Clear and marketable title should be verified so the property can be sold by the Fannie Mae REO department as quickly as possible.

In addition to the homeowner executed DIL documents, and depending on the specific state and regional requirements, the borrower(s) may be required to execute an Estoppel Agreement. - Notify the borrower of the terms and conditions for the DIL approval.

- Work with the foreclosure attorney to put the foreclosure action on hold pending receipt of the executed documents.

- Stay in touch with the borrower to let him/her know when the deed will be ready for his/her signature and, to ensure the borrower’s move-out plans are on schedule. If there’s a borrower incentive payment, advise the borrower when to expect the payment.

- Ensure that the property is vacant, secure, and has been inspected. Confirm the house is in broom swept condition, free of interior and exterior trash, debris or damage, and all personal belongings removed. Personal Property left by the borrower with a cash value equal to or greater than $500 requires Fannie Mae’s prior written approval before completing a Mortgage Release. The yard must be clean and neat and all keys and controls must be delivered. All inspection reports are fully reimbursable and if you work with an inspection vendor, you may have to specifically ask for an interior inspection.

- Once the servicer has received all required documentation, including the interior property inspection report, if applicable, it must report its final acceptance of the Mortgage Release to Fannie Mae by closing the case in HSSN. Refer to Closing Approved Cases for more details.

- Review and confirm the REOgram notification in Property 360 within one business day upon receipt of the daily REOgram notification from Property 360 once the servicer completes its final acceptance of the executed Mortgage Release. The servicer must review and resolve any exceptions from the daily notification in Property 360 no later than three business days, if applicable. Fannie Mae may charge the servicer a $100 compensatory fee for each day it is late in confirming the REOgram.

- Send the deed for recording immediately. Place "Fannie Mae" as the name on the deed. Once the deed has been recorded and returned, send a copy of the executed deed or any other applicable conveyance document(s) within two business days after title to the property is conveyed. The document(s) must be clearly identified/marked with the following:

-

Fannie Mae lender identification number

-

Fannie Mae loan number

-

Servicer name

-

Servicer loan number

Send all required documents to Fannie Mae at:

Fannie Mae

5600 Granite Parkway VII

Plano, TX 75024

-

- Remit any cash contribution to Investor Reporting using special remittance code 324.

- In your next reporting cycle, make sure that the loan is changed to IR Action Code 70 (uninsured loans) or 72 (insured loans).

- Ensure that the foreclosure is cancelled, request final attorney’s bill.

- Submit the Cash Disbursement Request Form 571, available on fanniemae.com, to receive your reimbursements.

- File an MI claim, if applicable.

- Report the acceptance of the deed to the credit bureaus.