My web

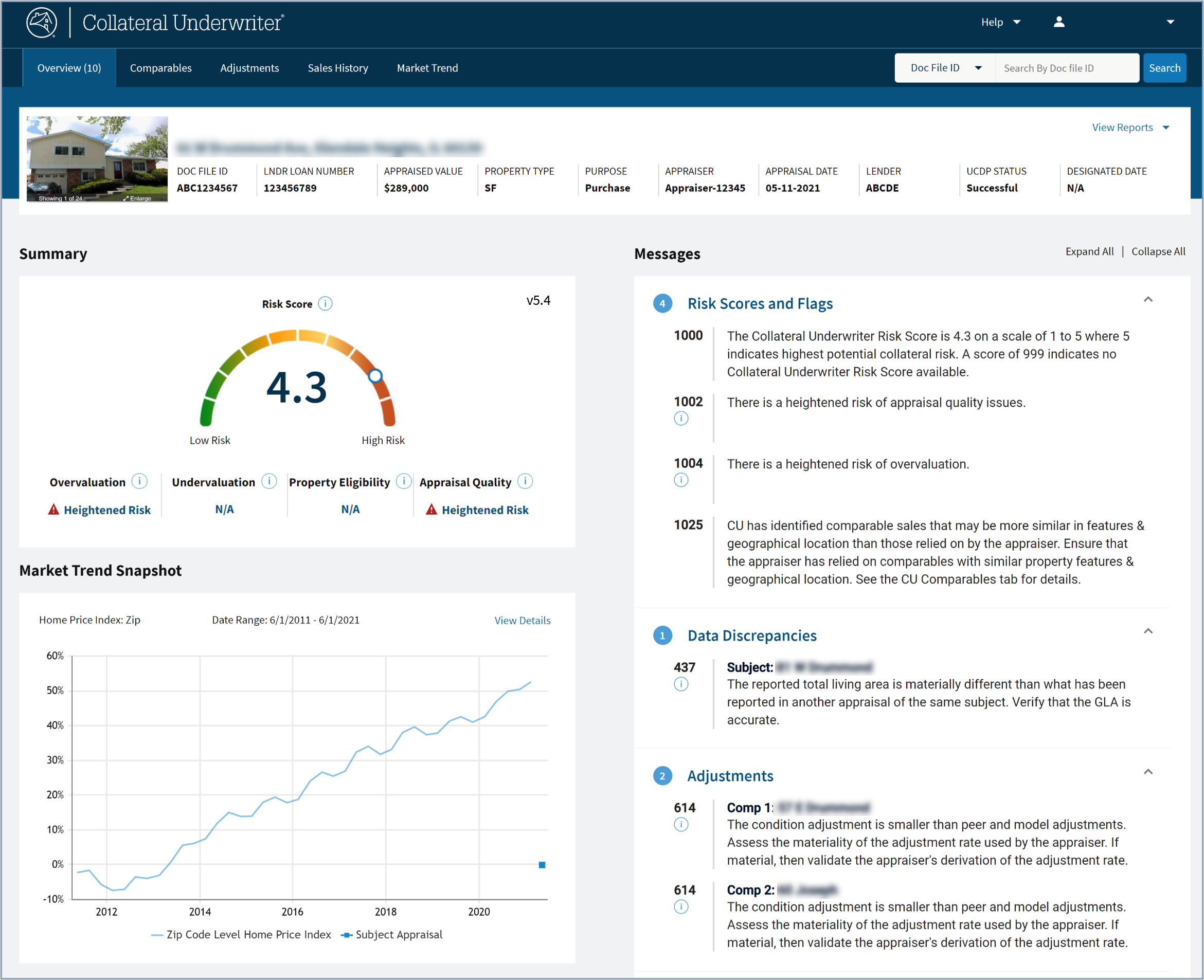

Risk Score and Flags Overview

![]()

The purpose of Collateral Underwriter (CU) is to identify appraisals with heightened risk of overvaluation, undervaluation, appraisal quality issues, or property eligibility or policy compliance violations. A single, overall risk score will help identify high-risk appraisals, while flags and messages provide additional clarity. The CU web application provides free access to a comprehensive suite of research tools to help proactively manage appraisal quality.

Risk Score

CU performs a comprehensive assessment of the appraisal and returns a single risk score that reflects the results of that automated analysis. Each appraisal receives a score on a scale of 1.0 to 5.0, with 1 indicating the lowest risk and 5 indicating the highest risk.

A score of 999 is returned if CU is unable to generate results such as the inability to geocode a property.

Lenders may use the CU risk score to segment appraisals by risk profile, thereby facilitating more efficient workflow management and resource allocation.

It’s important to think of the CU risk score in terms of “low risk and high risk,” and not in terms of “good or bad”. As with any automated analysis, there is opportunity for false negatives and false positives. While CU is effectively predictive of appraisal defects and overvaluation, a high-risk score does not necessarily mean the appraisal is bad. Lenders should perform additional due diligence on appraisals with high risk scores to determine if corrections are necessary. It may be beneficial to document the loan file with the results of the due diligence.

Flags

The CU risk score is a composite of three flags, or collateral risk factors: overvaluation, appraisal quality, and property eligibility and policy compliance. These flags identify the risk factors contributing to higher risk scores. On appraisals with high scores, you will see at least one of these flags. (The fourth flag or risk factor, undervaluation, is not currently used to determine the CU risk score.) The intention is to help the end-user understand the nature of the risk. Are there appraisal quality issues leading to potential overvaluation? Does the appraisal appear acceptable, but there may be a potential property eligibility issue? This is important because the reviewer’s course of action may vary depending on the situation.

There are four categories of flags. For more information on the flags, click the links below to open job aids for each topic.

- Overvaluation - Statistical modeling is used to identify appraisals with higher probability of material overvaluation.

- Undervaluation - Statistical modeling is used to identify appraisals with higher probability of material undervaluation.

- Appraisal Quality - The mechanics of the appraisal and the appraiser’s methodology including:

- Property Eligibility and Policy Compliance - Fatal Uniform Appraisal Dataset, or UAD, edits and the Critical Proprietary Messages.

For information on reconciliation messages, refer to the CU User Guide.