My web

Processing a Fannie Mae Payment Deferral or Disaster payment deferral in HSSN

![]()

Note: The following functionality is also available in Servicing Management Default UnderwriterTM (SMDU) and SMDU UI.

This job aid has been created as a tool for servicers when entering cases in HSSN for loans eligible for Payment Deferral or a Disaster payment deferral solution (refer to Servicer Directive for additional details including eligibility criteria).

When submitting a case through HSSN, you must select the appropriate Campaign Code.

For cases that require approval, follow the instructions Requesting Approval for a Loan Modification, using the applicable Campaign Code from the list below.

|

Use Campaign Code... |

When requesting approval for… |

| SMDU Payment Deferral Non-Delegated | a non-delegated Fannie Mae payment deferral being submitted through SMDU and the borrower must be at least one month delinquent and not more than two months delinquent (i.e., the borrower is not past due for more than two full monthly contractual payments) and such delinquency status must have remained unchanged for at least three consecutive months, including the month of the evaluation. |

| SMDU Disaster Payment Deferral Non-Delegated | a non-delegated Fannie Mae disaster payment deferral being submitted through SMDU and the borrower has a financial hardship as a result of a disaster event that impacts his or her ability to pay the current contractual monthly payment and is 1-12 months delinquent at the time of the evaluation. |

| Payment Deferral Non-Delegated | a non-delegated Fannie Mae payment deferral being submitted through SMDU or HSSN when the servicer did not use SMDU to decision. The borrower must be at least one month delinquent and not more than two months delinquent (i.e., the borrower is not past due for more than two full monthly contractual payments) and such delinquency status must have remained unchanged for at least three consecutive months, including the month of the evaluation. |

| Disaster Payment Deferral Non-Delegated | a non-delegated Fannie Mae disaster payment deferral being submitted through SMDU or HSSN when the servicer did not use SMDU to decision. The borrower has a financial hardship as a result of a disaster event that impacts his or her ability to pay the current contractual monthly payment and is 1-12 months delinquent at the time of the evaluation. |

If you determine that the case does not require Fannie Mae approval prior to performing the workout, refer to Creating and Submitting a Closed Loan Modification Case using the applicable Campaign Code from the list below.

|

Use Campaign Code... |

When requesting approval for… |

| SMDU Payment Deferral | Fannie Mae payment deferral which had a decision by SMDU and the borrower must be at least one month delinquent and not more than two months delinquent (i.e., the borrower is not past due for more than two full monthly contractual payments) and such delinquency status must have remained unchanged for at least three consecutive months, including the month of the evaluation. |

| SMDU Disaster Payment Deferral | Fannie Mae disaster payment deferral which had a decision by SMDU and the borrower has a financial hardship as a result of a disaster event that impacts his or her ability to pay the current contractual monthly payment and is 1-12 months delinquent at the time of the evaluation. |

| Payment Deferral | Fannie Mae payment deferral where the servicer did not use SMDU to decision and needs to report the workout to Fannie Mae. Servicer may also use HSSN to submit the case. |

| Disaster Payment Deferral | Fannie Mae disaster payment deferral where the servicer did not use SMDU to decision and needs to report the workout to Fannie Mae. The borrower has a financial hardship as a result of a disaster event that impacts his or her ability to pay the current contractual monthly payment, and is 1-12 months delinquent at the time of the evaluation. Servicer may also use HSSN to submit the case. |

Entering the Payment Deferral Case

IMPORTANT NOTES:

-

Since there is no trial period for a payment deferral or disaster payment deferral a delegated case is expected to be created and closed in the same transaction.

-

P&I, Interest Rate, Maturity Date, Product Type, & Servicing Fee cannot change

-

A change in P&I and Interest Rate due to an ARM or STEP change during the delinquent/deferment period should continue to occur as scheduled.

-

The Maturity Date must remain the same, therefore the “term” will need to adjust to equal the pre-workout maturity date.

-

-

MBS mortgage loans subject to a payment deferral, or a disaster payment deferral will not be subject to automatic reclassification as described in A1-3-06, Automatic Reclassification of MBS Mortgage Loans.

-

There is no capitalization. Populating any of the Capitalization or Contributions fields will result in a hard stop.

-

The following mortgage loans must be submitted as non-delegated: Bi-weekly, Daily Simple Interest (DSI), Long Term Standby Commitments (LTSC), cases with Payment Effective Date in the past (i.e., items which have been canceled and need to be resubmitted), and mortgage loans protected in accordance with the provisions of the Servicemembers Civil Relief Act (SCRA).

-

A servicer will not be able to cancel a payment deferral or a disaster payment deferral case; it can only be cancelled by Fannie Mae.

-

To cancel a case a servicer should send an email to [email protected] and include the loan number and reason for the cancelation request.

Follow the steps below to complete an accurate case.

- Select from the appropriate instructions below

- Submitting a delegated payment deferral or a disaster payment deferral - proceed to step 2 or,

- If submitting a non-delegated payment deferral or a disaster payment deferral - log into AMN and select Fannie Mae's Workout Profiler™. Enter the required information and then proceed to step 2.

Note: Due to the amount of data entry required to submit a non-delegated payment deferral or a disaster payment deferral case via HSSN, it is recommended to use the SMDU UI Create Manual Submission functionality in lieu of HSSN.

Note: The following loan types must be submitted as non-delegated: Bi-weekly, Daily Simple Interest (DSI), anything with a past Payment Effective Date (i.e. items which have been canceled, and need to be resubmitted), and LTSC (Long Term Standby Commitments).

2. Log into AMN and select Creating and Submitting a Closed Loan Modification Case. Enter the required information and select the appropriate campaign code. Only the

fields shown below are required to be populated.

-

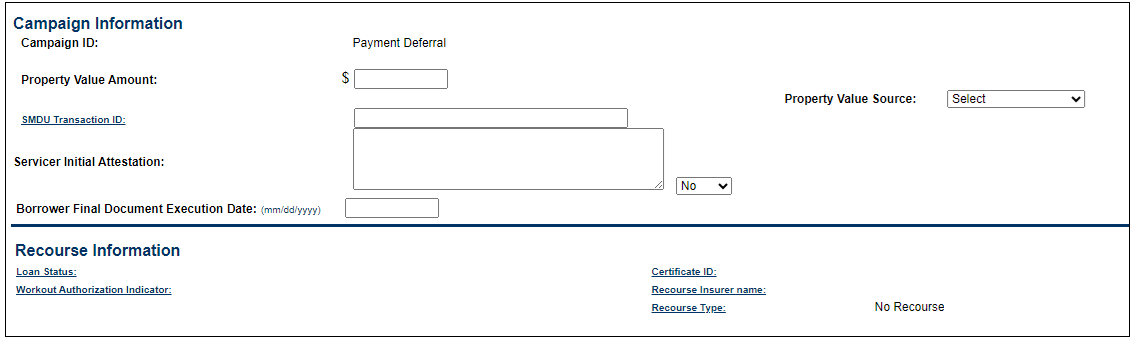

Campaign Information section:

No information is required to be entered in this section.

-

Recourse Information section:

No information is required to be entered in this section.

-

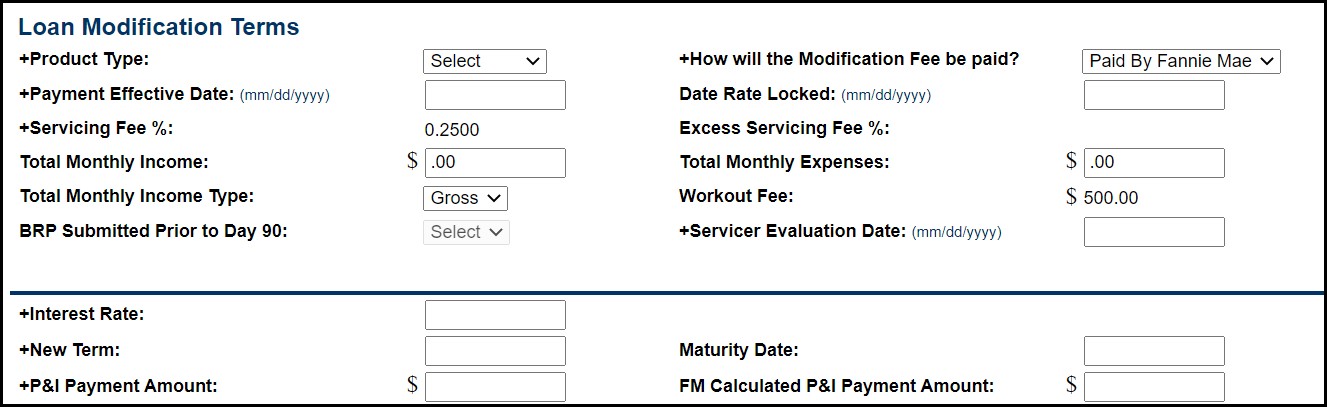

Loan Modification Terms section:

The following fields are required:

- Product Type - The product type cannot change.

- If the previous loan type was Step Rate, the last step change date should be in the past, indicating there are no future rate changes.

- Servicing Fee - Will not change.

- Interest Rate - The interest rate should match the current interest rate of the loan.

- A change in P&I and Interest Rate due to an ARM or STEP change during the delinquent/deferment period should continue to occur as scheduled.

- New Term - The Maturity Date should not change from what is reflected in SIR (Check SIR if necessary). Confirm a prior modification is not impacting the New Term entered.

- P&I Payment Amount - The P&I amount should match the current P&I amount of the loan.

- A change in P&I and Interest Rate due to an ARM or STEP change during the delinquent/deferment period should continue to occur as scheduled.

Note: If a pop-up message appears please disregard and click "X" to close the pop-up message.

-

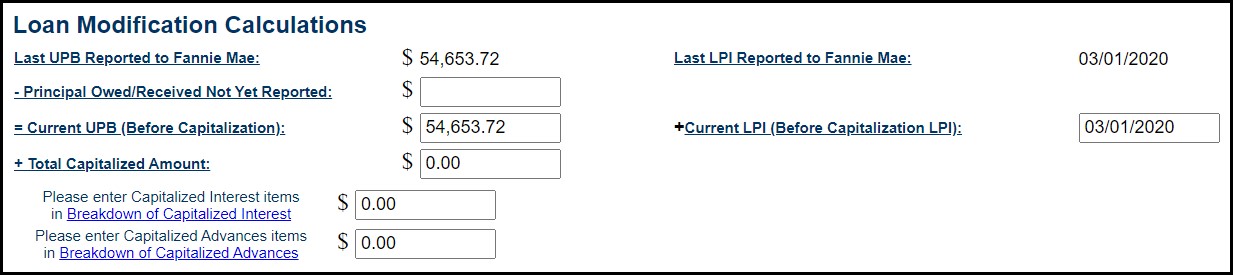

Loan Modification Calculations section:

No information is required to be entered in this section.

-

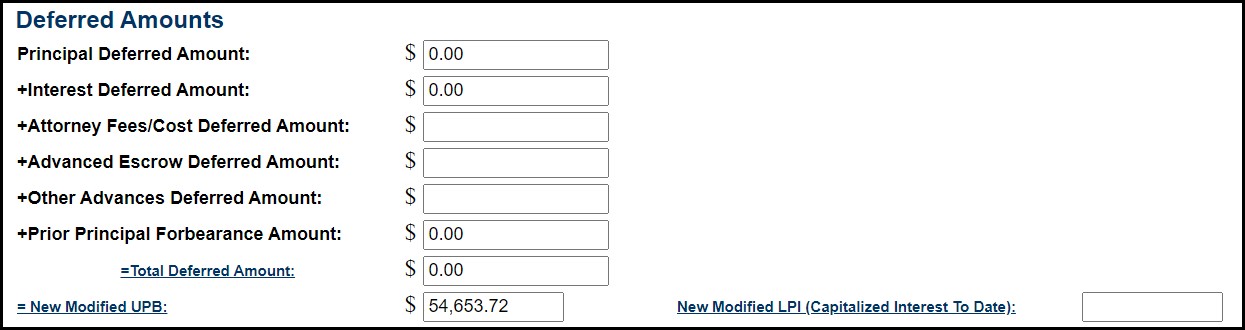

Deferral Amounts section:

The following fields are required:

|

Field Name |

Field Definition |

Required for payment deferral? |

Required for COVID-19 payment deferral? |

Required for disaster payment deferral? |

Delegated |

Non-Delegated / Workout Profiler |

| Principal Deferral Amount | The total dollar amount of the borrower's principal portion of the principal and interest payment(s) which are being deferred. Deferred payments are added to the end of the life of the loan which is non-interest bearing in the form of forbearance due at payoff. |

Yes |

Yes |

Yes |

HSSN will Auto Calculate based on data from Investor Reporting. Values must match exactly. Hard Stop. |

HSSN will Auto Calculate based on data from Investor Reporting. |

| Interest Deferred Amount | The total dollar amount of the borrower’s interest portion of the principal and interest payment(s) which are being deferred. Deferred payments are added to the end of the life of the loan which is non-interest bearing in the form of forbearance due at payoff. |

Yes |

Yes |

Yes |

HSSN will Auto Calculate based on data from Investor Reporting - There will be a very small tolerance amount allowed . Else, will be a Hard Stop. | HSSN will Auto Calculate based on data from Investor Reporting. |

| Attorney Fees/Cost Deferred Amount | The total dollar amount of deferred attorney fees and costs added to the end of life of the loan which is non-interest bearing in the form of forbearance due at payoff. |

Not Allowed |

Yes |

Yes |

Servicer Provided. | Once Case is Approved - Servicer may close the case (no Updates to any data after case Approval). |

| Advanced Escrow Deferred Amount | The total dollar amount of escrow advances deferred added to the end of life of the loan which is non-interest bearing in the form of forbearance due at payoff. |

Not Allowed |

Yes |

Yes |

Servicer Provided. | Once Case is Approved - Servicer may close the case (no Updates to any data after case Approval). |

| Other Advances Deferred Amount | The total dollar amount of other servicing advances deferred added to the end of life of the loan, non-interest bearing in the form of forbearance due at payoff. |

Not Allowed |

Yes |

Yes |

Servicer Provided. | Once Case is Approved - Servicer may close the case (no Updates to any data after case Approval). |

| Prior Principal Forbearance Amount | Any previous Principal Forbearance from a previously closed Loan Modification. |

If Applicable |

If Applicable |

If Applicable |

This amount will be pre-populated from SIR and is not editable. | This amount will be pre-populated from SIR and is not editable. |

| Total Deferred Amount | The total dollar amount of all allowed deferred amounts + any Prior Principal Forbearance. Due at the end of life of the loan, non-interest bearing in the form of forbearance due at payoff. |

N/A |

N/A |

N/A |

HSSN will Calculate Total on the screen. | HSSN will Calculate Total on the screen. |

| New UPB | Pre-Workout UPB (not including any prior principal forbearance) - Loan Principal Deferred Amount = New UPB |

N/A |

N/A |

N/A |

HSSN will Calculate on the screen | HSSN will Calculate on the screen |

-

Recommended Contribution section:

No information is required to be entered in this section.

-

MI Information section:

No information is required to be entered in this section:

-

Hardship Reason(s) section:

Select the correct hardship reason in the first drop-down field.

-

Contact Information section:

The following fields are required:

- Servicer Contact Name

- Phone

-

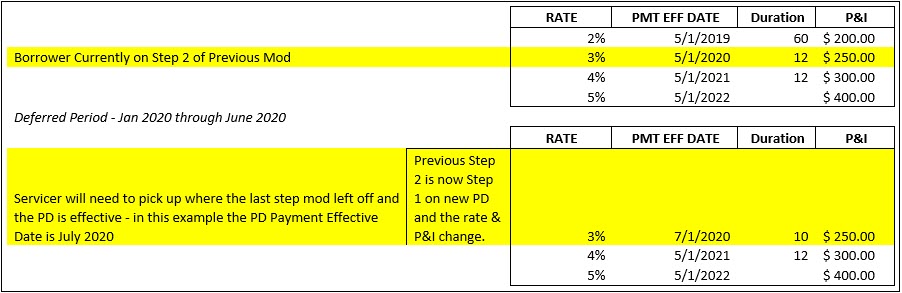

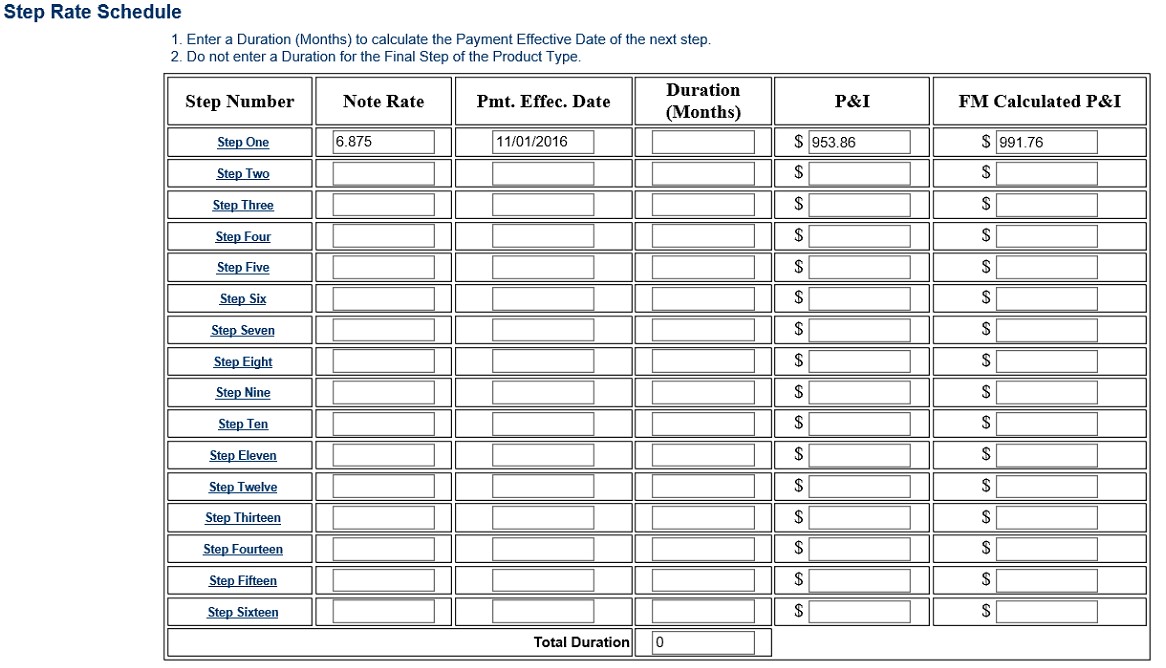

Step Rate Schedule section:

If a prior Loan Modification had a Step Schedule, the Step Schedule of the payment deferral should pick up at the point to where the payment deferral is

effective and match the remainder of the schedule exactly.

In this example the first yellow line is from a previous closed loan modification. In the second yellow line now represents step one in the payment deferral

schedule which takes the data from the first yellow line and now move the date to 7/1/2020 with a duration of 10 month because 2 of the 12 original months

have been used. Ensure that if there is more than one step, the other steps need to be entered into the Step Rate Schedule accordingly.

-

Click Test Authority Levels to confirm if any fields or data needs updating.

Note: Since there is no trial and the case will go directly to Closed status, the servicer should click Test Authority Levels before they Submit. Servicer needs to carefully review all inputs, test authority levels to see if any edits will trigger, make those updates, then review all inputs again, before clicking Submit.

-

Click Submit when you are ready to close the case.