My web

Creating and Submitting a Closed Loan Modification Case

![]()

Note: The following functionality is also available in Servicing Management Default UnderwriterTM (SMDU) and SMDU UI.

If you are a servicer that is delegated to underwrite modifications on behalf of Fannie Mae and are submitting a modification that does not require Fannie Mae’s approval, you must create and submit a closed loan modification case into HomeSaver Solutions TM Network (HSSN).

ALL servicers have permission from Fannie Mae to enter the case as a closed case when it meets the program guidelines as described in the Servicing Guide.

You must adhere to the following when submitting a case in HSSN:

- Enter a Campaign ID.

- Obtain a property valuation.

- Place borrower on a trial period plan.

When bridging to Investor Reporting, if the case hits a Failed Business Rule, if incorrect data was submitted on the case, or if a previously incorrect campaign ID was used, requiring cancellation and re-submission of the loan modification in HSSN, you will need to resubmit the case using the appropriate Modification Campaign Code.

IMPORTANT: If the borrower starts a modification Trial Period Plan and is determined to be eligible for a different modification program, take the following steps:

- Cancel the modification case.

- Re-enter a new case using the appropriate campaign code.

- Report the appropriate Trial Period Plan information.

Follow the steps below for step-by-step instructions on how to create and submit a closed loan modification case.

- Click on Create/Submit Closed Loan Modification Case from the menu within HSSN.

The Create Case screen appears. - Complete the Create Case screen as shown. Use the corresponding table below the screen shot to complete the fields.

- Click Submit.

The Create Delegated Case – Loan Modification screen appears. The Create Delegated Case – Loan Modification screen is divided into sections.

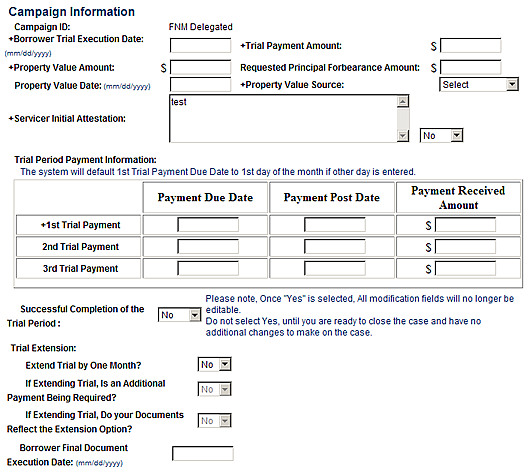

Data completeness and accuracy is important as it will ensure your case successfully moves to a closed status and ensures accurate transmission to the accounting system known as Servicer Investor Reporting (SIR). - Scroll down and complete the Campaign Information section as shown. Use the corresponding table and statements below the screen shot to complete the fields.

- Enter the trial period payment details in the Trial Period Payment Information section by entering the following data on the applicable row:

-

Enter the applicable payment due date in the Payment Due Date field. When reporting the first trial period payment, entry of the 1st trial period payment due date will auto-populate the 2nd, 3rd, and 4th (if applicable) trial period payment due dates.

-

In the Payment Post Date field(s), enter the date(s) for when the payments were received.

-

Enter the payment(s) received in the Payment Received Amount field(s).

-

Select No from the Successful Completion of the Trial Period drop-down list.

Important: You must select No even if you are reporting the final payment of the trial period. DO NOT change the drop-down selection to Yes as you will be unable to make final edits to the modification details.

Note: When the servicer reports receipt of the third (or fourth, if applicable) trial payment, HSSN will automatically submit a request to have the loan removed (reclassed) from the MBS pool, if applicable. The cut-off date to request reclassification is the 15th of the month. If the third trial payment is received and/or reported in HSSN between the 16th and the last day of the month, the servicer will need to extend the trial period payment by one month as reclassification from the MBS pool will not occur until the following month.

-

-

To extend the trial period by an extra month, you must answer the three questions that are below the Trial Extension section.

- Extend Trial by One Month? Answer Yes or No as appropriate.

- If Extending Trial, is an Additional Payment Being Required? Answer Yes or No as appropriate.

- If Extending Trial, Do Your Documents Reflect the Extension Option? Answer Yes or No as appropriate.

- If you are reporting the final payment of the trial period, a pop-up will appear asking you to enter Successful Completion of the Trial Period. Click OK on the pop-up. DO NOT change the drop-down selection to Yes as you will be unable to make final edits to the modification details.

- Enter the date on the signed modification agreement in the Borrower Final Document Execution Date field.

- Scroll down and complete the Recourse Information section as shown. Use the corresponding table below the screen shot to complete the field.

Field Description Officer Signature Date Date the servicer's officer approved the loan modification. This date field is required if a loan was in a pool that was reclassified.

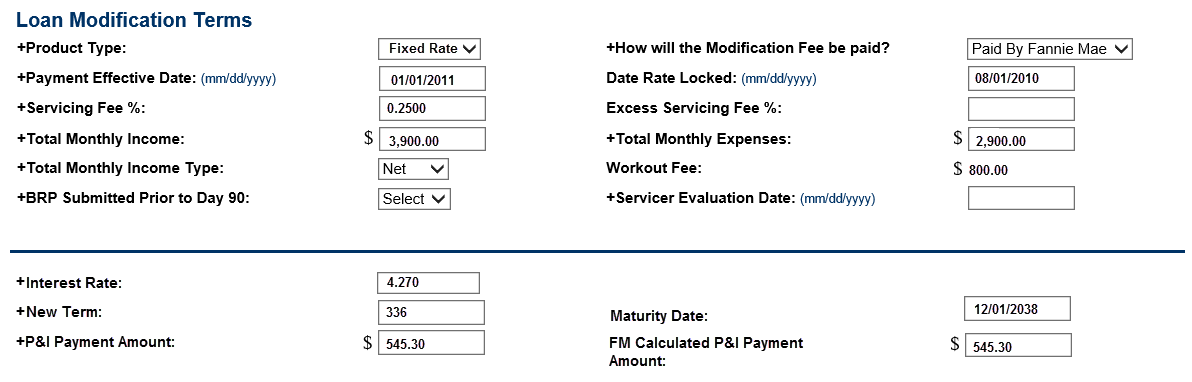

If entering an officer signature date, make sure it is not before the reclassification date. - Scroll down and complete the Loan Modification Terms section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description Product Type Select ’fixed’. How will the Modification Fee be paid? System will default to “Paid by Fannie Mae”. Payment Effective Date First payment due date for the modification. Date Rate Locked Day the servicer negotiated and agreed upon the loan modification terms with borrower and locked in interest rate. Used if change needs to be made to borrower’s interest rate. Servicing Fee % Auto populated with the post modification servicing fee.

For modified mortgage loans closed in HSSN, see Servicing Guide A2-3-02. Servicing Fees for Portfolio and MBS Mortgage Loans.Total Monthly Income Borrower’s monthly income. Total Monthly Expenses Borrower’s total monthly expenses, excluding mortgage payment. Total Monthly Income Type Select net or gross from the drop-down menu to describe the borrower’s monthly income type. Workout Fee Auto-populates your incentive for completion of a successful modification. BRP Submitted Prior to Day 90 A Y/N indicator that the servicer selects, which determines whether or not a borrower submitted the complete Borrower Response Package prior to the 90th day of delinquency. If the timing is within 90 days, the servicer would apply the 40% HTI feature of Flex Mod. Servicer Evaluation Date Non SMDU Users: The date the Servicer completed their evaluation and made the decision to offer the workout to the borrower. SMDU Users: The date that corresponds with the SMDU transaction ID used to create the HSSN case for the workout. For loan modifications – this is the Transaction ID associated with the Trial Structuring call. Interest Rate The new modified interest rate should be entered as the current note rate, the current market rate plus a servicing fee rounded to the nearest 8th, or the step one rate for a step-rate modification. New Term Number of months of the term. Maturity Date Automatically calculated from the term entered. P&I Payment Amount New modified P&I payment amount. FM Calculated P&I Payment Amount Automatically calculated from the term entered and should be the same amount as in the P&I Payment Amount field. - Scroll down and complete the Loan Modification Calculations section as shown. Use the corresponding table below the screen shot to complete the fields.

.jpg)

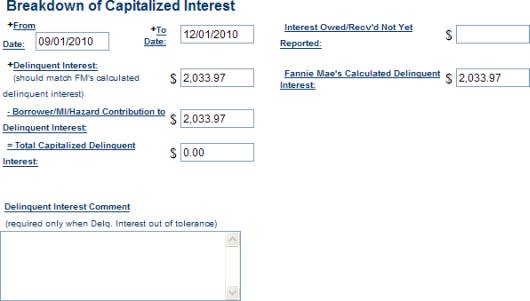

Field Description Last UPB Reported to Fannie Mae Corresponds to the date in the Last LPI Reported to Fannie Mae field and must match the UPB and LPI on the servicer’s system. LPI is the last paid installment payment. This is not the date the last payment was received in office, but the date the last payment was applied to the loan. Last LPI Reported to Fannie Mae Date auto-populates and must match the UPB and LPI on the servicer’s system. LPI is the last payment due that was paid. - Principal Owed/Received Not Yet Reported Reconciliation errors such as the principal portion of the P&I payment that was either received or reversed during the month, but not reported to SIR. = Current UPB (Before Capitalization) Will match your system of record, bringing it into balance with HSSN. + Current LPI (Before Capitalization LPI) Will match your system of record, bringing it into balance with HSSN. + Total Capitalized Amount Not an entry field. It is automatically calculated from the data entered into the Breakdown of Capitalized Interest and Breakdown of Capitalized Advances fields. Click on the links to enter information to pre-fill into these two fields. The Capitalization Detail section appears to allow you to enter information for both. - Requested Principal Forbearance Amount This field is only required for Payment Deferral Campaigns. + Total Deferred Amount This field is only required for Payment Deferral Campaigns. = New Modified UPB This field is only required for Payment Deferral Campaigns. New Modified LPI (Capitalized Interest to Date) The LPI associated with the New Payment Effective Date on the new workout. - Complete the Breakdown of Capitalized Interest portion of the Capitalization Detail section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description +From Date The date the LPI posted to the loan. +To Date The date prior to the due date for the 1st payment of the modification. Interest Owed/Recv’d Not Yet Reported Enter the interest portion of a payment received or reversed. This field is completed only if the Principal Owed/Received Not Yet Reported was completed on the Enter Loan Modification Calculations screen. +Delinquent Interest Should match the amount in the Fannie Mae’s Calculated Delinquent Interest field. Only a $75.00 tolerance between the servicer’s calculated interest and Fannie Mae’s calculated delinquent interest is allowed.

For a calculation definition, right click on the hyperlink for Delinquent Interest.Fannie Mae’s Calculated Delinquent Interest Pre-fills or automatically calculates based on entry for Current LPI and Modification Effective Date. - Borrower/MI/Hazard Contribution to Delinquent Interest Amount received from the borrower being applied to delinquent interest in order to reduce the capitalization amount. = Total Capitalized Delinquent Interest Automatically calculated based on the amount entered for delinquent interest less borrower contribution. Delinquent Interest Comment (required only when Delq. Interest out of tolerance) Only a $75.00 tolerance between the servicer’s calculated interest and Fannie Mae’s calculated delinquent interest is allowed. Add notes here when there is more than a $75.00 variation and contact Servicing Solutions for assistance to move the case to a closed status. - Complete the Breakdown of Capitalized Advances part of the Capitalization Detail section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description Attorney Fees/Costs Enter applicable amount. Could be costs paid or due to be paid prior to completion of the modification. +/- Escrow Balance

Negative Escrow Balance must be entered as a positive numberEnter projected escrow balance as of the new modified LPI date and the amount of any escrow advances paid.

If there are escrow advances or a projected escrow is needed, this field should indicate a (-) sign in front of the advanced amount.+ Other Amounts that do not apply in any previous fields. Since this is a required field, enter zero if there are no ‘other’ advances. If there is an amount, this should be noted in comments. - Borrower/MI/Hazard Contribution to Advances Borrower contribution applied to capitalized advances. - Disbursements Forgiven Should not be populated since Fannie Mae is not forgiving debt on modifications. = Total Capitalized Advances Contains an amount based on attorney fees and costs, escrow balance and any amounts entered in the Other field less the borrower contribution. Cannot be a negative number. - Click Return to Capitalization Summary to return to the worksheet in the Loan Modification Calculations section.

- Complete the remaining fields in the Loan Modification Calculations section as shown. Use the corresponding table below the screen shot to complete the fields.

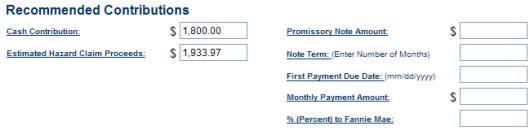

Field Description = New Modified UPB Automatically calculated based on either the last reported UPB or the current UPB depending on whether there was an adjustment and the total capitalized amount entered. This modified UPB should match the modification UPB on the document that was executed by the borrower. New Modified LPI (Capitalized Interest to Date) Automatically populated based on the payment effective date entered in the loan modification terms. - Scroll down and complete the Recommended Contributions section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description Cash Contribution Enter the amount applied towards advance contributions or capitalized interest. This field must equal the combination of the two fields from the capitalization detail screen. Promissory Note Amount All fields relating to the promissory note are not applicable to loan modification. Leave this field blank. Estimated Hazard Claim Proceeds Applicable if a hazard claim is being used to reduce capitalized advances on the modification. Note Term All fields relating to the promissory note are not applicable to loan modification. Leave these four fields blank. First Payment Due Date Monthly Payment Amount % (Percent) to Fannie Mae - Scroll down and complete the MI Information section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description MI Company Name The three fields within the MI Information section will pre-populate if the information has been reported on SIR. The fields are blank when the loan does not have mortgage insurance. MI Certificate No MI Percent Coverage - Scroll down and complete the Hardship Reason(s) section as shown.

Use the corresponding table below the screen shot to complete the fields.

| Field | Description |

| +Select Hardship Reasons (At least one must be selected) | There are 25 selections. At least one must be selected, however up to three selections can be chosen. |

| Hardship Reason Comment | Add any additional hardship comments. |

-

Scroll down and complete the Contact Information section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description +Servicer Contact Name Enter name of the person entering the case or who Fannie Mae would speak with regarding the case. +Phone Enter phone number to reach the contact. Extension Enter extension for the contact, if applicable. Fax Enter contact’s fax number. Email Enter contact’s email address. - Scroll down and complete the Servicer General Comment section as shown. Use the corresponding table below the screen shot to complete the fields.

Field Description Comment Enter any important notes regarding the case in this section.

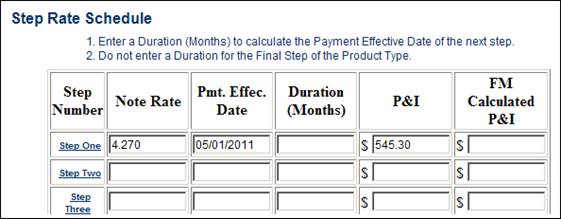

The Step Rate Schedule section will auto-populate with data in the Step One fields as shown. Additional data does not need to be entered when selecting ‘Fixed Rate’ as the loan product type in the Loan Modification Terms section.

- Click Submit.

The message, "The Case has been successfully submitted and is in Trial status” appears.

If an approved message is received, it could mean that either the servicing fee is incorrect, or the delinquent interest is out of tolerance.- If a servicing fee error is received, choose Close an Approved Case from the Main Menu, bring up the case, and correct the servicing fee to resubmit. Contact your portfolio manager or Servicing Solutions for assistance if needed.

- If a delinquent interest error is received, Fannie Mae will review the case and make corrections before the case can move to close.

- The Cancel button will take you back to the Main Menu and the Reset button will clear all data entered on the Create Case screen.