- Contents

My web page

Entering Housing Expenses for Second Homes and Investment Properties

IMPORTANT NOTE: The Real Estate Owned (REO) data used in the debt-to-income ratio calculation was updated in the DU Version 10.3 May Update to include the Insurance, Maintenance, Taxes & Misc entered in the REO section. The update is applied to loan casefiles created on or after June 1, 2020. The first set of instructions below are for loan casefiles created prior to June 1, 2020, followed by the instructions for loan casefiles created on or after June 1, 2020.

For loan casefiles created prior to June 1, 2020

For ease of reference, we will generally use the term “DU” to refer to Desktop Originator® and Desktop Underwriter® (DO®/DU®).

For loan casefiles involving the purchase or refinance of a second home or investment property, it is important that the Total Combined Housing Expense (excluding rent) is accurately accounted for on the Liabilities screen of DU. DU uses current housing expense data from the Liabilities screen in calculating the total expense qualifying ratio, instead of the data entered on the Income and Housing screen (Section V) with the exception of a rent payment. If there is a rent payment, then that only needs to be entered on the Income and Housing screen.

Note: These data entry instructions may also be used for entering the current housing expenses for a non-occupant applicant on a primary residence transaction.

This document provides an example of how to enter monthly housing expenses on the Income and Housing screen as well as how to make any necessary adjustments on the Liabilities screen.

Note: The data entry requirements provided in this document also apply to loan origination systems.

In this example,

John and Mary Homeowner (the loan applicants) own their current residence

and are applying for a loan to purchase a second home.

Below are the monthly housing expenses for their current residence:

-

First mortgage: $500

-

Second mortgage: $200

-

Hazard insurance: $75

-

Taxes: $100

-

Homeowner association dues (HOA): $125

This first step assumes that you have already ordered a credit report in DU and used the auto-populate liabilities feature to copy liabilities from the credit report to the 1003. For details on using this feature, see Ordering a new credit report or Reissuing a credit report.

-

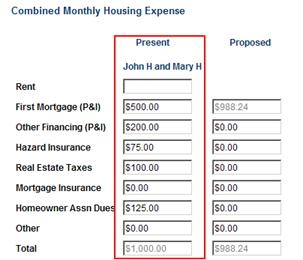

In the Combined Monthly Housing Expense section of the Income and Housing screen, enter the current housing expenses for the borrowers’ principal residence, including first and second mortgages, hazard insurance, taxes, mortgage insurance, and HOA.

As shown in the Total field in the Present column, the combined housing expense for the current residence is $1,000.

-

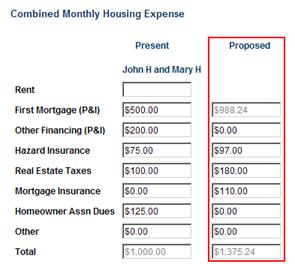

In the Proposed column, enter the applicable housing expenses for the subject property, including the second mortgage (if any), hazard insurance, taxes, mortgage insurance and HOA. The first mortgage is automatically calculated for you.

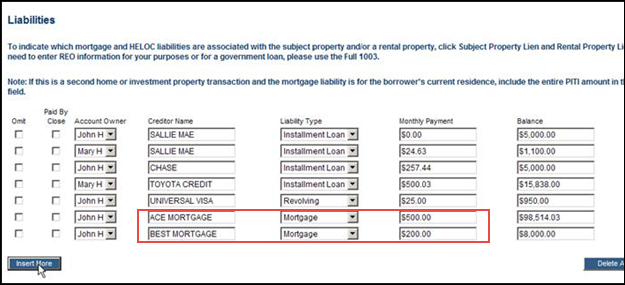

Click the Liabilities link in the navigation bar.

-

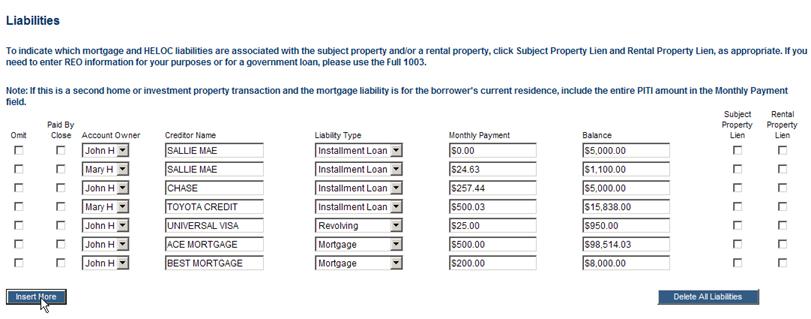

The Liabilities screen lists the mortgage liabilities, including the first mortgage ($500 monthly payment) and second mortgage ($200 monthly payment) for the borrowers’ current residence.

In this example, the total of these two liabilities ($700) includes only the P&I payment of the first and second mortgages, and does not include the expenses for mortgage insurance, real estate taxes, and HOA fees ($300). Therefore, the $1,000 total housing expense is not accurately reflected on the Liabilities screen.

Because DU uses the information on the Liabilities screen to calculate the total expenses qualifying ratio, it is important that all current combined housing expenses are accounted for on the Liabilities screen.

In this example, $300 per month in taxes, insurance, and HOA from the current residence must be added to the screen.

Note: If the expenses are associated to a non-occupant applicant on a primary residence transaction and they are reflected in the Insur, Maint, Taxes field in the Real Estate Owned screen, then they do not have to be added in the Liabilities screen.

Additional

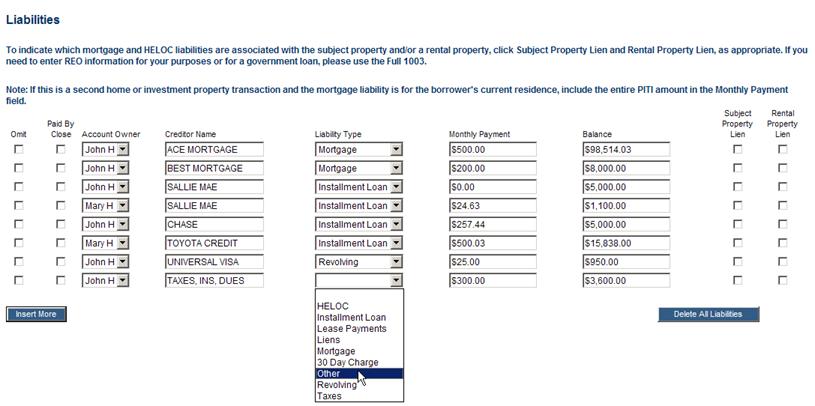

expenses can be added to the Liabilities screen by clicking Insert More.

-

In this example, enter the $300 as Taxes, Ins, Dues. Under Liability Type, we will select Other.

Enter $300 under Monthly Payment. In the Balance field, enter the annualized amount. In this example, the balance would be $3,600 ($300 x 12 months).

Now that the current combined housing expenses have been accounted for on the Liabilities screen, DU can correctly calculate the total expense ratio.

For loan casefiles created on or after June 1, 2020

For loan casefiles involving the purchase or refinance of a second home or investment property, it is important that the Total Combined Housing Expense (excluding rent) matches what is on the Liabilities screen and potentially the Real Estate Owned screen. The mortgage payment on the Liabilities screen either needs to include the other expenses, or the property needs to be included in the REO screen with a payment for the total other expenses entered in the Insur, Maint, Taxes field.

Date Entry Tip: If there is an REO record on the Real Estate Owned screen for the borrowers’ current residence and the payment for the total other expenses is in the Insur, Maint, Taxes field, then you should not enter a payment for those on the Liabilities screen.

Note: These data entry instructions may also be used for entering the current housing expenses for a non-occupant applicant on a primary residence transaction.

This document provides an example of how to enter monthly housing expenses on the Income and Housing screen as well as how to make any necessary adjustments on the Liabilities screen.

Note: The data entry requirements provided in this document also apply to loan origination systems.

In this example,

John and Mary Homeowner (the loan applicants) own their current residence

and are applying for a loan to purchase a second home.

Below are the monthly housing expenses for their current residence:

-

First mortgage: $500

-

Second mortgage: $200

-

Hazard insurance: $75

-

Taxes: $100

-

Homeowner association dues (HOA): $125

This first step assumes that you have already ordered a credit report in DU and used the auto-populate liabilities feature to copy liabilities from the credit report to the 1003. For details on using this feature, see Ordering a new credit report or Reissuing a credit report.

-

In the Combined Monthly Housing Expense section of the Income and Housing screen, enter the current housing expenses for the borrowers’ principal residence, including first and second mortgages, hazard insurance, taxes, mortgage insurance, and HOA.

As shown in the Total field in the Present column, the combined housing expense for the current residence is $1,000.

-

In the Proposed column, enter the applicable housing expenses for the subject property, including the second mortgage (if any), hazard insurance, taxes, mortgage insurance and HOA. The first mortgage is automatically calculated for you.

Click the Liabilities link in the navigation bar.

-

The Liabilities screen lists the mortgage liabilities, including the first mortgage ($500 monthly payment) and second mortgage ($200 monthly payment) for the borrowers’ current residence.

In this example, the total of these two liabilities ($700) includes only the P&I payment of the first and second mortgages, and does not include the expenses for mortgage insurance, real estate taxes, and HOA fees ($300 total). The $300 payment can either be added to one of the mortgage payments or an REO record can be created for the property and the $300 payment should be entered in the Insur, Maint, Taxes field.

Click the Full 1003 link, and then click the Real Estate Owned link.

-

Enter the following information about the borrowers’ current residence, and make sure the total monthly payment amount for the non-mortgage current housing expenses in the Income and Housing screen match what you enter in the Insur, Maint, Taxes field, which is $300 in this case.

-

Select a borrower in the Property Owner field. Note: It must be the same borrower associated to the mortgage in the Liabilities section.

-

Select Current Residence for the Property Indicator.

-

Select Retained for the Property Disposition.

-

Select the applicable property type in the Type of Property field.

-

Enter the appraised value in the Market Value field. Note: It can be an estimated value.

-

Enter the payment for the non-mortgage current housing expenses in the Insur, Maint, Taxes field.

© 2021 Fannie Mae. Trademarks of Fannie Mae.