My web

Completing the Reconciliation of Mortgage Portfolio - Schedule 1 (Form 473)

![]()

Overview

Every month, a servicer must use the Reconciliation of Mortgage Portfolio – Schedule 1 (Form 473) to reconcile the servicer’s trial balance to Fannie Mae’s Trial Balance for their Actual/Actual (A/A) portfolio.

Schedule 1 is used to identify discrepancies in the following:

- P&I Mortgage Payments

- Loan Counts

- Actual Unpaid Principal Balances (UPBs)

This review determines the cumulative effect on the servicer’s shortage/surplus for their Actual/Actual portfolio. Schedule 1 lists the loans that are causing discrepancies and identifies the entity (either the servicer or Fannie Mae) that is responsible for the resolution. Servicers must prepare a separate Schedule 1 for each unique 9-digit server number. (Servicers with Scheduled/Actual (S/A), Scheduled/Scheduled MRS Acquired (S/S Cash) or Scheduled/Scheduled MBS (S/S MBS) should use Schedule 1A Form 512).

Completing Schedule 1

Use the following documents to complete Schedule 1:

|

Form |

Location |

|

Schedule 1 (Form 473) |

|

|

Schedule 1A - for S/S and S/A loans (Form 512) |

|

|

Fannie Mae's Trial Balance |

|

|

Servicer's Trial Balance |

|

|

Lender Recap Report (LRRO12201) |

|

|

Accepted Transaction Reports -for A/A loans |

|

|

Remittance Detail Principal and Interest Report - for S/S and S/A loans |

|

|

Ending Loan Activity Rejects Report |

|

1. Header Section

Complete the header section of Schedule 1:

|

Field |

Action |

|

Month Reconciled |

|

|

Servicer Name |

|

|

Page |

|

2. Portfolio Totals per Servicer's Records

Use the Servicer’s Trial Balance to enter the totals for Fixed Installment (P&I), Loan Count, and Unpaid Principal Balance (UPB) for all loans in identified portfolio.

|

Field |

Action |

| P&I Mortgage Payment |

|

|

Loan Count |

|

|

Actual Unpaid Principal Balance |

|

3. Portfolios Totals per Fannie Mae's Records

Use the Trial Report to enter the totals for Fixed Installment (P&I), Loan Count, and Unpaid Principal Balance (Actual UPB).

- In Fannie Mae Connect, open the Trial Balance Report using Tableau.

Note: Use the Part A Summary for the Actual/Actual P&I Mortgage Payment, Loan Count, and Actual Unpaid Principal Balance fields.

- Enter the totals at the bottom of Schedule 1 in the Portfolio Balance per Fannie Mae's Records section.

Note: If using the interactive PDF these fields will auto-populate.

Note: If the totals agree, your reconciliation is complete, skip to Step 7 to sign and archive the reconciliation. If the totals do not agree, proceed to Step 4.

4. Research Differences

Compare the loan detail records from your company's trial balance to Fannie Mae's Trial Balance Report: Part A A/A to identify the discrepancy in the following fields:

-

P&I Mortgage Payment

-

Loan Count

- Actual UPB

Check any unresolved Hard Rejects listed on the Ending Loan Activity Report and note the reason for each reject.

Note: The current month report will not be an option if all Hard Rejects have been cleared.

Note: An unresolved Hard Reject indicates Fannie Mae did not update the loan to reflect the Actual UPB and last paid installment (LPI) date you reported as well as the following:

- For A/A loans, a hard reject means Fannie Mae did not apply the P&I remittance you reported.

- For S/S loans, Fannie Mae did apply scheduled P&I remittances to update the scheduled UPB.

Additional Reports that can be used for research purposes:

- Acceptance Transaction Reports

- Lender Recap Report (LRRO1201)

5. Resolve Differences

Determine whether each data discrepancy reflects an error in your records (F) for Fannie Mae’s records or (S) for Servicer's record's.

- Correct any records that are in error.

- Attach any documentation used in determining the correction to the Schedule 1. Any transactions reported in error can be corrected in the next reporting cycle.

Note: If Fannie Mae’s records are inaccurate, the action needed depends on the type of error.

Note: If the information you provided at loan delivery needs to be corrected, the LSDU Post Purchase Adjustment Request (DCC) will need to be requested. Any documentation used for this correction needs to be attached to the Schedule 1. The Data Change Rules Matrix lists correct documentation needed for each data element.

- For loans liquidated in error, contact your Fannie Mae Investor Reporting Analyst to request that the loan be reinstated.

- If a loan has been paid in full (Action Code 60) or a loan has been repurchased (Action Code 65) and you have not reported this action, report it as soon as possible using the proper Action Date.

- For any questions regarding loans reported with action codes 70, 71 or 72, contact Fannie Mae's Servicer Resources Center Assistance at 1-800-2FANNIE (800-232-6643) Option 1, Option 3 or [email protected].

Note: When Fannie Mae’s records are inaccurate, remember to attach the backup documentation used to the Schedule 1.

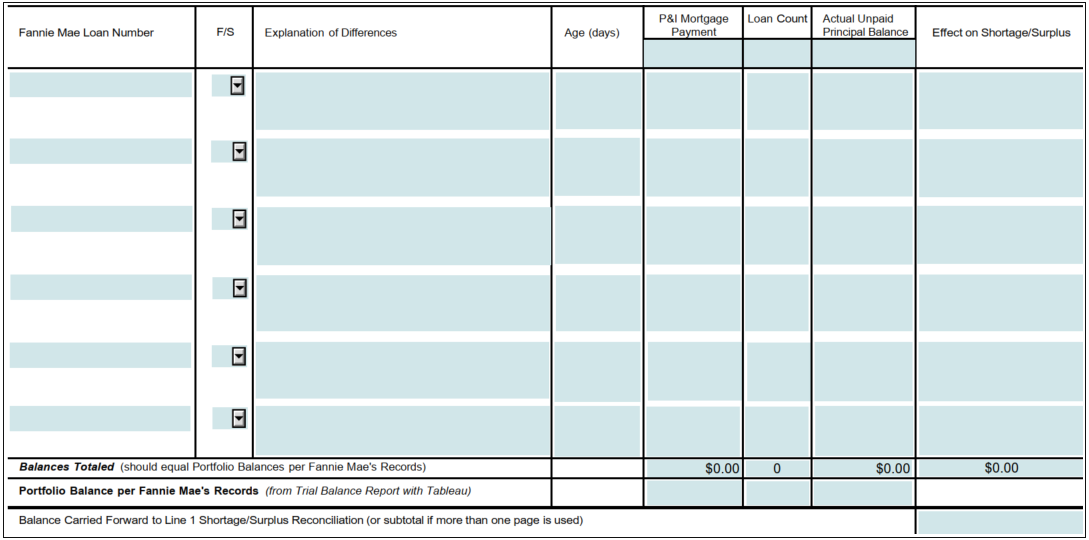

6. Reconciling Items:

Complete the following sections if the portfolio totals/balances are not equal for each of the following items:

|

Field |

Action |

|

Fannie Mae Loan Number |

|

|

F/S |

|

|

Explanation of Differences |

|

|

Age |

|

|

P&I Mortgage Payment |

|

|

Loan Count |

|

|

Actual Unpaid Principal Balance |

|

|

Effect on Shortage/Surplus |

Note: You may have to use prior reports if the reconciling items is aged and caused shortage/surplus differences in past months. |

|

Balance Totaled (should equal Portfolio Balances per Fannie Mae's Records) |

Note: These fields will auto populate if using the interactive PDF. |

| Balance Carried Forward to Line 1 Shortage/Surplus Reconciliation (or subtotal if more than one page is used) |

|

7. Footer Information

Complete the following sections of the footer:

|

Field |

Action |

|

Servicer Name |

|

|

Prepared By |

Note: If using the interactive PDF, sign the form after printing. |

|

Phone Number |

|

|

Date |

|

|

Approved By |

Note: If using the interactive PDF, sign the form after printing. |

|

Phone Number |

|

|

Date |

|

8. Common Errors

Prior to finalization, review your completed Schedule 1 to ensure that you eliminate common errors frequently identified during a Fannie Mae compliance review. Below are some of the common errors:

|

Field |

Action |

|

Portfolio Totals per Servicer's Records |

|

| Portfolio Totals per Fannie Mae's Records |

Note: A separate schedule should be created for each individual remittance type and portfolio number. |

|

F/S |

|

| Explanation of Differences |

Note: Take prompt action to resolve reconciling times including submitting documentation through LSDU Post Purchase Adjustment Requests when data is incorrect in Fannie Mae's system. |

|

Age |

|

|

P&I Mortgage Payments |

|

|

Loan Count |

|

|

Actual Unpaid Principal Balance |

Note: Shortages must be entered as negative amounts in parentheses. However, if you use the interactive PDF, enter a minus sign in front of the number. Once you click out of the field, the number appears red and in parentheses. |

| Effect on Shortage/Surplus |

Note: Shortages must be entered as negative amounts in parentheses. However, if you use the interactive PDF, enter a minus sign in front of the number. Once you click out of the field, the number appears red and in parentheses. |

What Happens Next

If using the interactive PDF or Excel® version, print the completed form for your records. Fannie Mae will settle the disposition of any unreconciled differences with each servicer on an individual case-by-case basis.

A servicer can resolve minor residual cash differences (such as those resulting from rounding) by performing a monthly cash adjustment after reviewing all the rejected transactions.

An example of a completed Schedule 1 is shown below.