My web

Missing or Inaccurate Adjustment Messages - 621-626, 632-633

![]()

These messages identify when the appraiser’s adjustment may have been in the wrong direction or when the appraiser did not make an adjustment when one may have been warranted. Click on the Adjustments tab to view additional details. For more information on Adjustment Messages click here.

For adjustments in the wrong direction for either GLA, Condition, Quality, View, or Location, the appraiser made an adjustment but it was in the wrong direction. For example, an appraiser may have adjusted in the positive direction for a comparable that has a larger GLA than the subject property, but because the comp is larger the adjustment should be in the negative direction.

Time adjustment messages are derived from the Collateral Underwriter® (CU®) market analytics. Individual market segments or property types may perform differently than the model as a whole. As with other model adjustments, it is not Fannie Mae’s expectation that the appraiser make time adjustments solely to align with the CU model nor should lenders instruct the appraiser to change adjustments to match the model. Appraisers are responsible for identifying market trends and making appropriate adjustments. The appraiser must analyze the comparable sales to determine if there have been any changes in market conditions from the time the comparable went under contract until the effective date of the appraisal. The appraiser’s analysis should reveal whether a time adjustment is warranted.

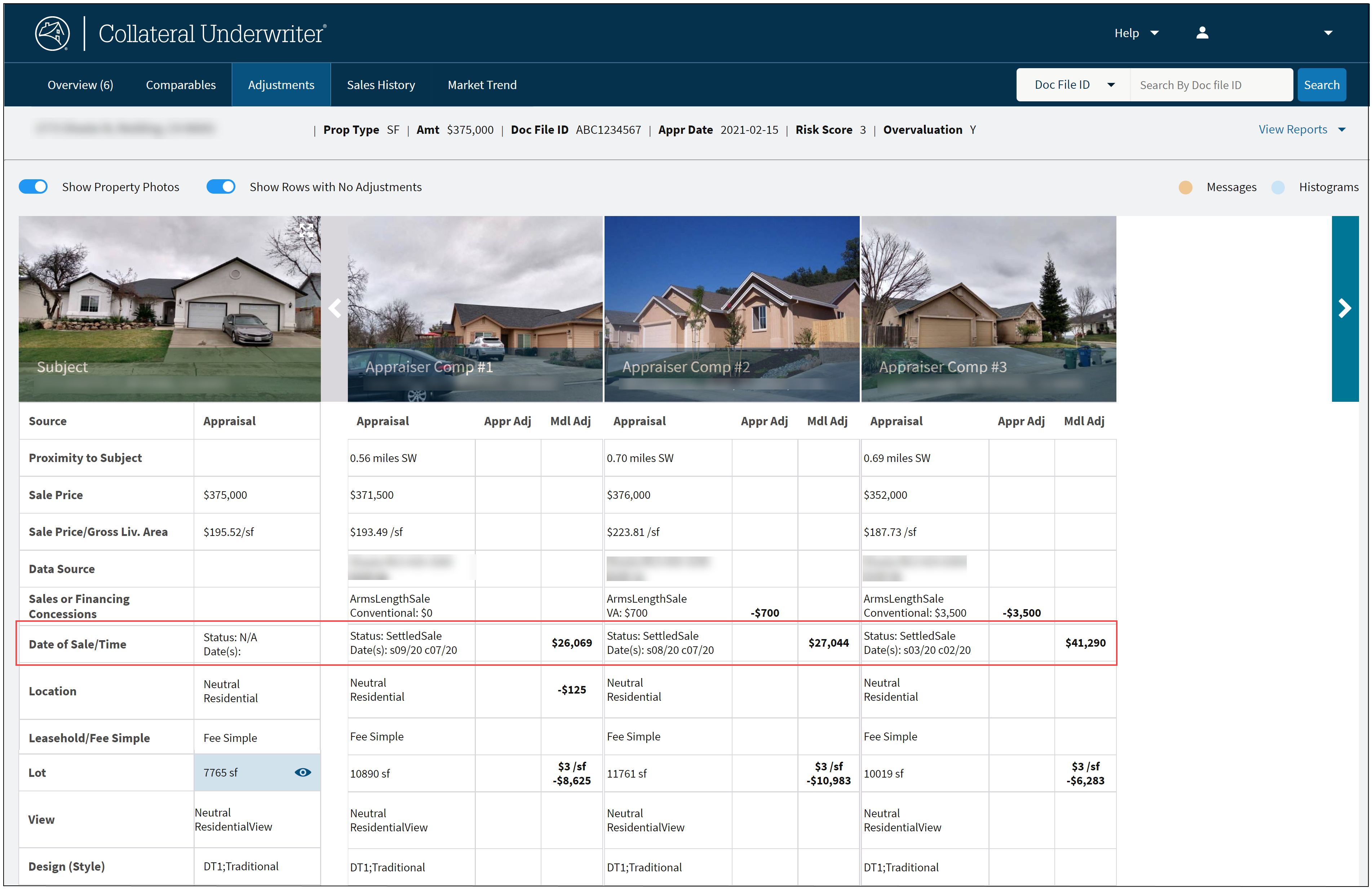

- From the Appraisal Overview page select the Adjustments tab.

- For time adjustments messages, go to the "Date of Sale" column to review the CU model adjustment amount. For adjustments in the wrong direction, locate the characteristic identified by the adjustment message and review the appraiser and

CU model adjustments. In this example, message 632 identifies that a positive time adjustment may be warranted but no adjustment has been made by the appraiser.

Things to consider

It is not Fannie Mae’s expectation that the appraiser make adjustments that align with CU, and lenders should not simply instruct the appraiser to change their adjustment to match the model.

However, lenders should determine if the appraiser’s adjustments are adequately supported and reflective of market reaction. The impact to the appraised value should also be considered in terms of both the magnitude and direction of the adjustment in question. Also, think about how the overall credibility of the appraisal is impacted.

In some cases, it may be beneficial to seek clarification and support for some adjustments that may impact the subject’s appraised value.